PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083249

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083249

Egg Separator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

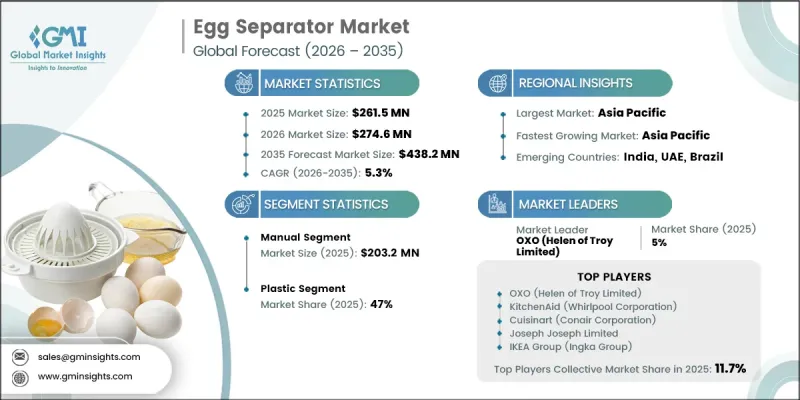

The Global Egg Separator Market was valued at USD 261.5 million in 2025 and is estimated to grow at a CAGR of 5.3% to reach USD 438.2 million by 2035.

Egg separators are specialized kitchen tools designed to efficiently divide egg yolks from egg whites, serving as an essential utility in baking, confectionery preparation, culinary applications, and food processing workflows. The market is expanding due to a combination of rising egg consumption globally, increasing adoption of modern kitchen gadgets, premiumization of household cooking tools, and the rapid expansion of online retail ecosystems. The global egg separator industry is also undergoing structural changes across product innovation, material preferences, usage patterns, and distribution networks. Although still categorized as a basic kitchen accessory, the market is being reshaped by shifting consumer expectations toward convenience, durability, and design efficiency. Growth is strongly supported by increasing urbanization, expanding middle-class populations, and evolving home cooking habits. The Asia Pacific region leads both in market size and growth momentum, supported by high egg production and consumption levels, rapid urban expansion, and strong demand for kitchen utility products across East Asian households. At the same time, digital retail channels are transforming purchasing behavior, with online platforms increasingly replacing traditional retail outlets. Direct-to-consumer digital storefronts are expanding faster than third-party marketplaces as brands strengthen their owned sales channels. In contrast, offline retail channels are facing pressure due to reduced mall traffic and shifting consumer buying preferences in developed markets.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $261.5 Million |

| Forecast Value | $438.2 Million |

| CAGR | 5.3% |

The manual egg separator segment accounted for USD 203.2 million in 2025. This segment continues to lead the market due to its low cost, ease of use, and widespread adoption across households and small-scale food service operations. Manual separators remain popular because they do not require electricity, involve minimal maintenance, and offer practical functionality for everyday cooking and baking needs.

The plastic-based segment held 47% share in 2025. Plastic remains the most widely used material in egg separator manufacturing due to its affordability and mass production efficiency. However, the segment is increasingly challenged by growing demand for more durable alternatives such as stainless steel and silicone, along with tightening regulatory actions targeting plastic usage in multiple regions. Rising environmental awareness is also influencing consumer preferences, encouraging a gradual shift toward reusable, long-lasting kitchen tools that offer better sustainability performance and extended product lifecycles.

U.S. Egg Separator Market held 89.9% share, generating USD 62.4 million in 2025. The market is experiencing signs of maturity as household penetration levels for entry-level products approach saturation, particularly in the lower price range. This has shifted competitive focus toward premium product upgrades and material transitions from plastic to higher-end alternatives, alongside growing reliance on online distribution channels. Broader consumption trends in egg-based food preparation continue to support steady long-term demand for kitchen separation tools.

Major companies operating in the global egg separator market include OXO, KitchenAid, Joseph Joseph, Cuisinart, IKEA Group, Kuhn Rikon, Chef'n Corporation, Norpro, Good Cook (Bradshaw Home), Prepworks by Progressive International, Trudeau Corporation, Tovolo, MSC International (Joie), RSVP International, Fox Run Brands, Hutzler Manufacturing Company, Westmark GmbH, Chef Craft, Pampered Chef, Wilton Brands, and Lakeland. Companies in the egg separator market are focusing on product innovation, premium material upgrades, and ergonomic design improvements to strengthen market positioning. Manufacturers are increasingly shifting from basic plastic designs toward stainless steel and silicone-based products to meet rising sustainability expectations and durability demands. Expansion of e-commerce channels, particularly direct-to-consumer platforms, is enabling brands to improve visibility and customer engagement while reducing dependence on traditional retail networks. Firms are also investing in branding, packaging innovation, and kitchenware ecosystem integration to enhance product differentiation. Strategic collaborations with online retailers and culinary influencers are supporting stronger product promotion.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Business trends

- 2.3 Type trends

- 2.4 Material trends

- 2.5 Price range trends

- 2.6 Capacity trends

- 2.7 End use trends

- 2.8 Distribution channel trends

- 2.9 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem and value chain analysis

- 3.1.1 Raw material & component suppliers

- 3.1.2 Manufacturers & assemblers

- 3.1.3 Distributors & wholesalers

- 3.1.4 Retailers & end-users

- 3.1.5 Profit margin analysis across value chain

- 3.2 Industry impact forces

- 3.2.1 Market Driver

- 3.2.2 Market challenges/pitfalls

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Industry ecosystem analysis

- 3.5 Regulatory framework

- 3.5.1 Food contact material safety standards (FDA, EU Regulation 10/2011)

- 3.5.2 BPA & chemical restriction regulations by region

- 3.5.3 Product safety & labeling compliance (CPSC, CE marking)

- 3.5.4 Sustainability & recyclability regulations impacting kitchenware

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis (driven by primary research)

- 3.6.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.7 Technology and innovation landscape

- 3.7.1 Emerging filter media technologies

- 3.7.2 Smart & condition-monitoring enabled filters

- 3.7.3 High-pressure & high-efficiency filtration innovations

- 3.8 Porter's Analysis

- 3.9 PESTEL Analysis

- 3.10 Trade data analysis (driven by primary research)

- 3.10.1 Import & export volume & value trends (HS code 8210)

- 3.10.2 Key trade corridors & tariff impact on kitchen tool flows

- 3.11 Impact of AI and generative AI on the market

- 3.11.1 AI-driven disruption of product design & consumer personalization

- 3.11.2 GenAI use cases & adoption roadmap by segment (DTC brands, retailers)

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Distribution infrastructure & channel penetration landscape (driven by primary research)

- 3.12.1 Channel coverage by region & format (modern vs. traditional trade) (driven by primary research)

- 3.12.2 Last-mile infrastructure gaps & emerging channel shifts (Q-commerce, social commerce) (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 APAC

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 ($ Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Electric

Chapter 6 Market Estimates and Forecast, By Material, 2022 - 2035 ($ Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Stainless Steel

- 6.4 Silicone

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Price Range, 2022 - 2035 ($ Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low (< $10)

- 7.3 Medium ($10-$30)

- 7.4 High (> $30)

Chapter 8 Market Estimates and Forecast, By Capacity, 2022 - 2035 ($ Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Single Egg

- 8.3 Multi-Egg

Chapter 9 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.3.1 Professional Bakeries

- 9.3.2 Restaurants & Catering

- 9.3.3 Institutional (Hotels, Culinary Schools, Hospital Kitchens)

- 9.3.4 Others (Food Processing Units, Meal-Kit Manufacturers)

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce Platforms

- 10.2.2 Brand/Company Websites (D2C)

- 10.3 Offline

- 10.3.1 Specialty Kitchen Stores

- 10.3.2 Mega Retail / Hypermarkets

- 10.3.3 Others (Department Stores, Home Improvement Stores)

Chapter 11 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Top Global Players

- 12.1.1 KitchenAid

- 12.1.2 Cuisinart

- 12.1.3 OXO

- 12.1.4 Joseph Joseph

- 12.1.5 IKEA Group

- 12.1.6 Kuhn Rikon

- 12.1.7 Chef'n Corporation

- 12.2 Regional Players

- 12.2.1 Good Cook (Bradshaw Home)

- 12.2.2 Norpro

- 12.2.3 Prepworks by Progressive International

- 12.2.4 Trudeau Corporation

- 12.2.5 Tovolo

- 12.2.6 MSC International (Joie)

- 12.2.7 RSVP International

- 12.3 Niche & Specialist Players

- 12.3.1 Fox Run Brands

- 12.3.2 Hutzler Manufacturing Company

- 12.3.3 Westmark GmbH

- 12.3.4 Chef Craft

- 12.3.5 Pampered Chef

- 12.3.6 Wilton Brands

- 12.3.7 Lakeland