PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083366

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083366

Frozen Food Processing Machinery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

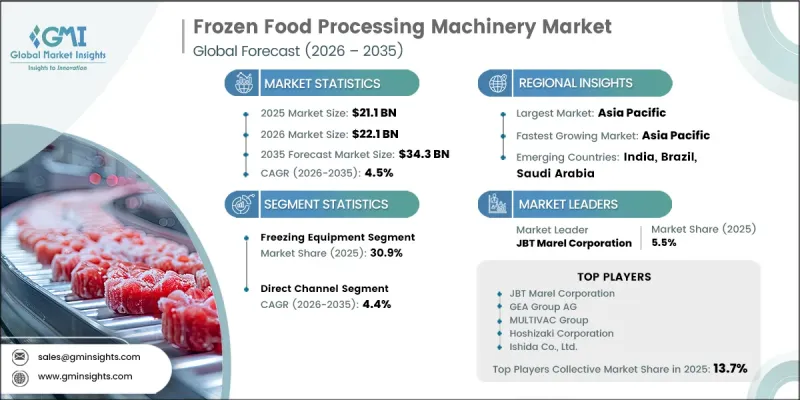

The Global Frozen Food Processing Machinery Market was valued at USD 21.1 billion in 2025 and is estimated to grow at a CAGR of 4.5% to reach USD 34.3 billion by 2035.

Growth in the frozen food processing machinery market is supported by the continued rise in frozen and convenience food consumption worldwide, driven by changing lifestyles, urban expansion, increasing disposable incomes, and ongoing investments in cold-chain infrastructure. Food manufacturers are expanding production capacities to meet growing consumer demand, resulting in greater investments in advanced processing equipment. In addition, evolving food safety regulations and environmental requirements are encouraging processing facilities to modernize their machinery and adopt energy-efficient technologies. The industry is also witnessing a gradual transition toward refrigeration systems with lower environmental impact, alongside increasing deployment of automation technologies designed to improve operational efficiency, reduce labor dependency, and ensure consistent product quality. Expanding organized retail networks and rising demand for ready-to-cook and ready-to-eat food products continue to create favorable conditions for equipment manufacturers. Furthermore, investments in production modernization and processing optimization are strengthening long-term demand for advanced frozen food processing machinery across both developed and emerging markets, supporting sustained industry expansion through 2035.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.1 Billion |

| Forecast Value | $34.3 Billion |

| CAGR | 4.5% |

The freezing equipment segment accounted for 30.9% share in 2025 and is projected to grow at a CAGR of 5.9% through 2035. The segment's leading position is primarily attributed to the high capital investment requirements and technological sophistication associated with freezing systems compared to other processing equipment categories. Continuous advancements in freezing technologies, coupled with increasing demand for efficient food preservation solutions, are supporting segment growth. Manufacturers are increasingly investing in advanced freezing systems that enhance product quality, improve operational efficiency, and optimize production throughput, further strengthening the segment's market leadership.

The direct sales channel represented 61.5% share in 2025 and is expected to grow at a CAGR of 4.4% during 2026-2035. The dominance of this channel is linked to the technical complexity and substantial investment associated with food processing machinery. Direct engagement between manufacturers and end users allows for customized equipment specifications, installation support, commissioning services, and long-term maintenance programs. The direct sales model also facilitates extended customer relationships and generates recurring revenue through spare parts supply, system upgrades, calibration services, and ongoing technical support, making it the preferred distribution approach across the industry.

North America Frozen Food Processing Machinery Market captured 27.8% share in 2025 and is anticipated to grow at a CAGR of 4.1% through 2035. The region continues to maintain a strong market position due to its established food processing sector, continuous investments in production capacity upgrades, and increasing focus on automation and operational efficiency. Demand for advanced processing machinery remains supported by replacement cycles, modernization initiatives, and compliance with evolving food safety regulations. The region's robust frozen food manufacturing infrastructure and commitment to technological advancement continue to create substantial opportunities for machinery suppliers and equipment manufacturers.

Major companies operating in the global frozen food processing machinery market include Air Products and Chemicals, Inc., GEA Group AG, Alfa Laval AB, Buhler Group, and AMF Tech. Companies operating in the frozen food processing machinery market are focusing on several strategic initiatives to strengthen their market position and expand their customer base. A major priority is investment in automation technologies that improve productivity, reduce labor requirements, and enhance operational efficiency. Manufacturers are also developing energy-efficient equipment and environmentally sustainable refrigeration systems to align with evolving regulatory requirements and customer sustainability goals. Strategic partnerships, acquisitions, and collaborations are being pursued to expand technological capabilities and geographic reach. In addition, companies are increasing investments in research and development to introduce innovative processing solutions with improved performance and lower operating costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 By Machinery type

- 2.2.3 By Freezing Technology

- 2.2.4 By Mode of operation

- 2.2.5 By Application

- 2.2.6 By End use

- 2.2.7 By Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global demand for frozen & convenience food products

- 3.2.1.2 Rapid cold chain infrastructure expansion in emerging markets

- 3.2.1.3 Automation adoption to address labor shortages in food processing

- 3.2.1.4 Stricter food safety regulations driving equipment upgradation

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Supply chain disruptions for critical components (compressors, refrigerants)

- 3.2.2.2 Skilled workforce gaps for operating & maintaining advanced automation

- 3.2.3 Opportunities

- 3.2.3.1 IQF & cryogenic equipment demand from premium seafood & protein exporters

- 3.2.3.2 Retrofitting & modernization of legacy food processing plants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory framework

- 3.4.1 Standards & compliance requirements

- 3.4.2 Regional regulatory frameworks

- 3.4.3 Certification standards

- 3.5 Major market trends and disruptions

- 3.6 Technology/innovation landscape

- 3.6.1 Current trends

- 3.6.2 Emerging trends

- 3.7 Pricing Analysis (driven by primary research)

- 3.7.1 Historical price trend analysis (driven by primary research)

- 3.7.2 Pricing strategy by player type (premium / value / cost- plus) (driven by primary research)

- 3.8 Future market trends

- 3.9 Trade data analysis (driven by paid database) (HS Code- 8438)

- 3.9.1 Import/export volume & value trends (driven by primary research)

- 3.9.2 Key trade corridors & tariff impact (driven by primary research)

- 3.10 Impact of AI & Generative AI on the Market

- 3.10.1 AI- driven disruption of existing business models

- 3.10.2 GenAI use cases & adoption roadmap by segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

- 3.13 Capacity & Production Landscape (Driven by Primary Research)

- 3.13.1 Installed Capacity by Region & Key Equipment Producer (Driven by Primary Research)

- 3.13.2 Capacity Utilization Rates & Expansion Pipelines (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Middle East and Africa

- 4.2.1.5 Latin America

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Machinery Type, 2022 - 2035 (USD Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Preparation equipment

- 5.2.1 Cutters

- 5.2.2 Slicers

- 5.2.3 Grinders

- 5.2.4 Blenders & mixers

- 5.2.5 Blanchers

- 5.2.6 Extruders & homogenizers

- 5.2.7 Others (peelers, portioning machines, etc.)

- 5.3 Freezing equipment

- 5.3.1 Blast freezers

- 5.3.2 Spiral freezers

- 5.3.3 Plate freezers

- 5.3.4 Individual quick freezing (IQF) equipment

- 5.3.5 Cryogenic Freezers (LN2 & CO2 Systems)

- 5.3.6 Others (tunnel freezers, fluidized bed freezers, etc.)

- 5.4 Packaging equipment

- 5.4.1 Wrapping machines

- 5.4.2 Bagging machines

- 5.4.3 Cartoning machines

- 5.4.4 Tray loaders & sealers

- 5.4.5 Others (vacuum packaging machines, shrink wrappers, etc.)

- 5.5 Refrigeration & cooling systems

- 5.5.1 Blast chillers

- 5.5.2 Industrial refrigeration units (low-GWP refrigerant systems)

- 5.5.3 Holding room refrigeration

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Freezing Technology, 2022 - 2035 (USD Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Mechanical freezing

- 6.3 Cryogenic freezing

Chapter 7 Market Estimates & Forecast, By Mode of Operation, 2022 - 2035 (USD Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Semi-Automatic

- 7.3 Automatic

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 (USD Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Fruits & vegetables

- 8.3 Dairy products

- 8.4 Meat, poultry, & seafood

- 8.5 Ready-to-eat (RTE) meals

- 8.6 Bakery products

- 8.7 Snacks

- 8.8 Others (soups, sauces, etc)

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 (USD Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Food processing companies

- 9.3 Restaurants and foodservice

- 9.4 Retail & supermarkets

- 9.5 Others (distribution centers, etc)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 (USD Billion, Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Companies

- 12.1.1 Air Products and Chemicals, Inc.

- 12.1.1.1 Business Overview

- 12.1.1.2 Financial Data

- 12.1.1.3 Product Landscape

- 12.1.1.4 Strategic Outlook

- 12.1.1.5 SWOT Analysis

- 12.1.2 Alfa Laval AB

- 12.1.3 Buhler Group

- 12.1.4 GEA Group AG

- 12.1.5 Ishida Co., Ltd.

- 12.1.6 JBT Marel Corporation

- 12.1.7 Linde plc

- 12.1.8 MULTIVAC Group

- 12.1.9 Tetra Pak International S.A.

- 12.1.10 The Middleby Corporation

- 12.1.1 Air Products and Chemicals, Inc.

- 12.2 Regional Companies

- 12.2.1 Hoshizaki Corporation

- 12.2.2 Intralox

- 12.2.3 Nantong Sinrofreeze Equipment Co., Ltd.

- 12.2.4 NTSquare

- 12.2.5 OctoFrost Group

- 12.2.6 SPX FLOW, Inc.

- 12.2.7 Starfrost (UK) Ltd.

- 12.3 Emerging Companies

- 12.3.1 AMF Tech

- 12.3.2 Nantong Icesource Coldchain Technology Co., Ltd.

- 12.3.3 Nantong Worldbase Refrigeration Equipment Co., Ltd.

- 12.3.4 Yurnfreeze