Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1686579

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1686579

India Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 95 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

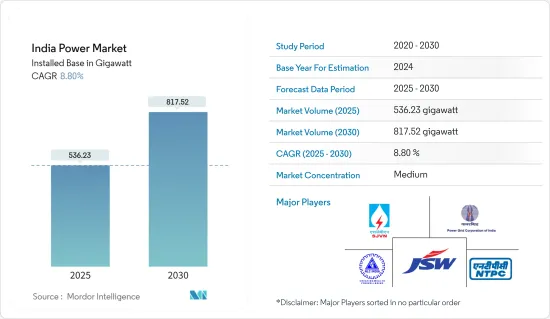

The India Power Market size in terms of installed base is expected to grow from 536.23 gigawatt in 2025 to 817.52 gigawatt by 2030, at a CAGR of 8.8% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, factors such as supportive government policies, rising electricity demand due to infrastructural activities, and rising population are expected to drive the market during the forecasted period.

- On the other hand, huge investment is required to set up and modernize power generation, transmission & distribution networks, and weak private sector investments are expected to hinder the growth of the Indian power market.

- Nevertheless, India has abundant availability of solar irradiance and receives solar energy throughout the year. This has created enormous opportunities to exploit solar energy from the sunniest sites in the country, especially Rajasthan, Gujarat, and Andhra Pradesh. The factor above, clubbed with foreign investment and extensive power projects, provides an opportunity to grow the power market in India.

India Power Market Trends

Thermal Source for Power Generation to Dominate the Market

- India has significant coal reserves, a readily available and relatively affordable fuel source for power generation. The country's large coal reserves have made it a major producer and consumer, making thermal power plants an attractive option for meeting the growing electricity demand.

- Moreover, India has a well-established infrastructure for coal-based thermal power generation. Numerous coal mines, transportation networks, and coal-fired power plants are already operating. This existing infrastructure provides a foundation for the market's dominance of thermal power generation.

- Furthermore, in September 2022, the Ministry of Energy India announced that the country is preparing to add as much as 56 GW of coal-fired generation capacity by 2030 to meet the growing electricity demand. The increase in coal-fired capacity would represent about a 25% jump above the country's current 204 GW of coal-fueled generation from 285 coal thermal power plants.

- As of November 2023, India heavily relies on thermal power sources for generating electricity, with a total installed capacity of 239.07 GW, accounting for more than 56% of the country's electricity generation capacity.

- Additionally, thermal power plants, especially those using coal, have been cost-competitive compared to alternative sources such as renewable energy. The initial capital investment for setting up thermal power plants is often lower, and the operating costs, including fuel costs, have been relatively stable compared to volatile oil and gas prices.

- Thermal power plants can provide a consistent and reliable supply of electricity, making them suitable for meeting the base load demand, which is the minimum level of power required to meet the everyday needs of consumers. The ability to provide a stable power supply has contributed to the dominance of thermal sources in the market.

- Therefore, as mentioned above, the thermal power sector will likely dominate the market during the forecasted period.

Government Policies and Support are Expected to Drive the Market

- Government policies and support are crucial drivers of the Indian power market as they provide a clear roadmap, financial incentives, regulatory frameworks, and infrastructure development necessary for the sector's growth. By promoting renewable energy, energy efficiency, grid integration, and digitalization, the government creates an enabling environment that attracts investments, fosters innovation, and facilitates the transition toward a sustainable and reliable power market in India.

- The Indian government has set ambitious renewable energy targets to increase the share of renewables in the overall energy mix. Policies such as the National Solar Mission, National Wind Energy Mission, and various state-level renewable energy policies provide incentives and support for developing renewable power projects. These initiatives aim to attract investments, streamline regulatory processes, provide financial incentives, and ensure a favorable environment for renewable energy growth.

- To catalyze a sustainable transformation in the nation, the government has established a formidable objective of achieving 500 gigawatts (GW) of installed renewable energy capacity by 2030. This target encompasses the installation of 280 GW from solar power and 140 GW from wind power sources, aiming to drive a significant green revolution across the country.

- As of 2022, the country has more than 162 GW of installed renewable energy capacity compared to 147 GW in 2021, signifying the increasing adaption of renewable energy in the country, consequently driving the power market in India.

- In March 2023, India charted a definitive path for expanding its renewable energy sector, outlining a clear roadmap for its growth. As part of this vision, the country is committed to establishing Ultra Mega Solar Parks with a combined generation capacity of 40 gigawatts by March 2024. This ambitious initiative demonstrates India's steadfast dedication to scaling up its renewable energy infrastructure and fostering a sustainable future.

- Additionally, the government offers various financial incentives and subsidies to promote renewable energy deployment and energy efficiency measures. These include capital subsidies, generation-based incentives, tax benefits, concessional financing, and viability gap funding. Such incentives make renewable projects financially attractive and encourage private sector participation in the power market.

- Therefore as per the above mentioned point, supportive government policies are expected to drive the market during the forecasted period.

India Power Industry Overview

The Indian power market is semi-consolidated. Some key players in this market (not in a particular order) include NTPC Ltd, NLC India Ltd, SJVN Ltd, JSW Group, and Power Grid Corporation India Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 52852

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 India Installed Power Generating Capacity Forecast, till 2028

- 4.3 Share of Installed Power Generation Capacity (%), by State, India, 2022

- 4.4 Electricity Generation and Consumption Forecast, in Terawatt Hours, India, till 2028

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

- 4.7 Market Dynamics

- 4.7.1 Drivers

- 4.7.1.1 Increasing Energy Demand

- 4.7.1.2 Government Support for Power Sector

- 4.7.2 Restraints

- 4.7.2.1 Financial Viability

- 4.7.1 Drivers

- 4.8 Supply Chain Analysis

- 4.9 PESTLE Analysis

5 MARKET SEGMENTATION

- 5.1 Generation

- 5.1.1 Thermal

- 5.1.2 Hydro

- 5.1.3 Renewable

- 5.1.4 Others

- 5.2 Transmission and Distribution

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Adani Group

- 6.3.2 JSW Group

- 6.3.3 NHPC Ltd

- 6.3.4 NLC India Ltd.

- 6.3.5 NTPC Ltd.

- 6.3.6 Power Grid Corporation India Ltd.

- 6.3.7 Reliance Power Limited

- 6.3.8 SJVN Ltd.

- 6.3.9 Tata Power Company Limited

- 6.3.10 Torrent Power Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Renewable Energy Growth

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.