PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444013

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444013

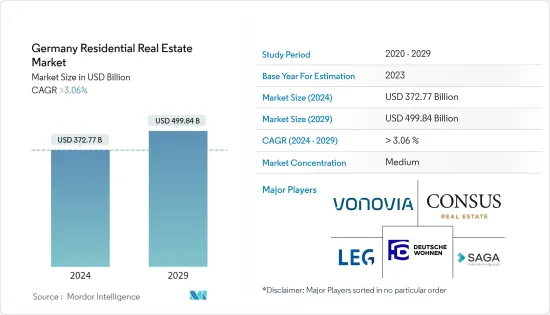

Germany Residential Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Germany Residential Real Estate Market size is estimated at USD 372.77 billion in 2024, and is expected to reach USD 499.84 billion by 2029, growing at a CAGR of greater than 3.06% during the forecast period (2024-2029).

Despite the market's expansion in the previous decade, it halted in 2022. Purchase costs slightly increased throughout the year. Prices decreased starting in July 2022 despite the low amount of supply, among other reasons being the increase in the ECB's primary interest rate and subsequently rising interest rates, even though the first half had seen an increase. Due to the high levels of uncertainty, private persons, investors, and property developers grew more cautious and offered proportional concessions on purchase prices.

Key Highlights

- The previous ten years were marked by continuously growing rental and purchase prices, with top yields for residential real estate hovering at 2.3 percent until mid-2022. However, starting in the summer, geopolitical factors gradually slowed the market: the Ukraine War significantly impacted the economy, the European Central Bank (ECB) gradually increased theprimaryn interest rate, and inflation hit historic highs of nearly 10%. High energy costs, energy supply constraints, constantly growing building expenses, and future uncertainty were among the factors that restrained progress. Investment deals were few, and building activity also drastically decreased. Thus, the federal government's objective of building the 400,000 additional dwellings needed each year slipped into the future.

- German rental markets are regulated in areas with competitive housing markets. The state government must approve the conversion of rental apartments into owner-occupied apartments. The "rent brake," which has been in place, limits rent increases by landlords to 10% over the local market level. The green transition is one trend that will also affect the German real estate market in the future. The government is actively encouraging energy-efficient homes since the building sector accounts for roughly 16% of all greenhouse gas emissions in Germany. Five billion euros more will be made available under the "Immediate Action Program 2022" to promote the construction of new, energy-efficient structures, including social housing, and the renovation of existing ones. Political support, however, might also present a problem.

Germany Residential Real Estate Market Trends

Strong Demand and Rising Construction Activities to Drive the Market

Germany has approved the construction of 24,500 houses until March 2023. According to the Federal Statistical Office (Destatis), this represents a decline of 10,300 construction permits, or 29.6%, from March 2022. Since May 2022, the number of new residential permits issued has been lower than in the same month the previous year, with the year-on-year fall reaching 10% since October 2022 and exceeding 20% since January 2023. In March 2007, The last time there was a greater year-on-year loss than in March 2023 was in March 2007 (-46.5% on March 2006).

From January to March 2023, 68,700 residential building licenses were issued, a decrease of 25.7% from the same period the previous year (January to March 2022: 92,500 building permits). The high costs of construction materials and poor financing circumstances are anticipated to remain the primary factors in the fall of building projects. The outcomes include building permits for new houses and new dwellings in existing buildings.

In recent years, the migration crisis and strong economic growth have added to the already strong demand in the country. Consequently, foreseeable structural changes, such as demographic effects, are also perceived as important drivers of demand. Most recently, the supply side was the main obstacle to further growth. However, the political uncertainty regarding new government constellations and the high investment pressure of many market participants have tempted some portfolio holders to bring products to the market in the second half of the year.

The status of the public finasignificantly impactsct on civil engineering, and infrastructure investment is crucial. Due to decreasing business investment in commercial, retail, and office buildings, the non-residential segment's performance has remained modest. Over the past twelve months, most German construction companies have reported stable or marginally better results. Given the benign demand environment, the prognosis for profit margins is stable now, and price wars are being avoided. However, persistent material shortages and unstable input prices continue to be problems. Without contract escalation clauses, builders find it challenging to pass price hikes on to clients. Future profit margins may suffer as a result.

Rising House Prices in Germany Affecting Demand in the Market

Germany's Federal Statistics Office (StBA) stated on Friday that housing expenses in the country fell by the most in a single quarter in 16 years in the fourth quarter of 2022. Rising inflation and bank interest rate hikes to curb it were mentioned as reasons for the unexpected turnaround. The news was backed by data indicating that housing prices in urban and rural regions declined by 3.6% on average. A similar decline occurred in the first quarter of 2007 when they fell 3.8%. Until the drop in Q4 2022, German home prices had risen since 2010. The StBA stated that the price decrease may be attributed to a similar reduction in demand due to increasing finance costs and continued inflation. Prices for single-family houses and city duplexes declined 5.9% in Q4 2021. Apartment prices fell by an average of 1%. House prices in rural regions declined by 5.5%.

Prices for homes (2.9%) and apartments (1.6%) declined in Germany's seven most populated cities: Berlin, Hamburg, Munich, Cologne, Frankfurt, Stuttgart, and Dusseldorf. In densely populated rural areas, the price of single and two-family dwellings rose by 12% in the third quarter of 2021 compared to last year. The cost of condominiums in these areas increased by 12.3%. In less densely populated rural areas, prices for single and two-family homes rose by 15.5%, while condominiums rose by 11.2%.

Experts have identified several reasons why house prices continue to rise so rapidly. Over the past decade, low interest rates, increasing demand, a lack of investment opportunities, and a strong economy have contributed to Germany's rising house prices. Construction costs have also increased significantly, with prices rising for building materials such as wood, concrete, and steel. The construction industry is facing labor shortages.

Germany Residential Real Estate Industry Overview

The German residential real estate market is fragmented and has become increasingly competitive. The increasing spending on infrastructure, new government initiatives to drive investments, and new project announcements are expected to bring an overall development in the real estate sector, which may further enhance the interest of more investors. Some of the major players in Germany include Vonovia SE, Deutsche Wohnen SE, SAGA Hamburg, LEG Immobilien SE, and Consus Real Estate.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strong Demand and Rising Construction Activities to Drive the Market

- 4.2.2 Rising House Prices in Germany Affecting Demand in the Market

- 4.3 Market Restraints

- 4.3.1 Weak economic environment

- 4.4 Market Opportunities

- 4.4.1 Recovery in Demand and Supply Demand Due to Government Initiatives

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Government Initiatives and Regulations for the Residential Real Estate Sector

- 4.7 Residential Real Estate Buying Trends - Socio-economic and Demographic Insights

- 4.8 Insights into Size of Real Estate Lending and Loan to Value Trends

- 4.9 Insights into Interest Rate Regime for General Economy and Real Estate Lending

- 4.10 Insights into Rental Yields in the Residential Real Estate Segment

- 4.11 Insights into Capital Market Penetration and REIT Presence in Residential Real Estate

- 4.12 Insights into Affordable Housing Support Provided by Government and Public-private Partnerships

- 4.13 Insights into Real Estate Tech and Startups Active in the Real Estate Segment (Broking, Social Media, Facility Management, and Property Management)

- 4.14 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Villas and Landed Houses

- 5.1.2 Condominiums and Apartments

- 5.2 By Key Cities

- 5.2.1 Berlin

- 5.2.2 Hamburg

- 5.2.3 Cologne

- 5.2.4 Munich

- 5.2.5 Rest of Germany

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Vonovia SE

- 6.2.2 Deutsche Wohnen SE

- 6.2.3 SAGA Siedlungs-Aktiengesellschaft Hamburg

- 6.2.4 LEG Immobilien SE

- 6.2.5 Consus Real Estate

- 6.2.6 Degewo

- 6.2.7 Vivawest

- 6.2.8 Residia Care Holding GmbH & Co.

- 6.2.9 Wohnungsbaugenossenschaft Musikwinkel eG (WBG)

- 6.2.10 ABG Frankfurt Holding*

7 FUTURE OF THE MARKET

8 APPENDIX