PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444681

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1444681

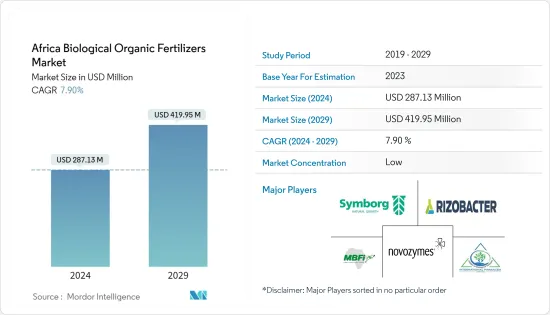

Africa Biological Organic Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Africa Biological Organic Fertilizers Market size is estimated at USD 287.13 million in 2024, and is expected to reach USD 419.95 million by 2029, growing at a CAGR of 7.90% during the forecast period (2024-2029).

Key Highlights

- Organic agriculture promotes food systems that increase food security and improve living conditions but currently, only 0.2 percent of agricultural land in Africa is dedicated to organic farming. This was due to limited knowledge of how organic products are produced, processed, and marketed. However, the war in Ukraine has caused a significant disruption in global supply chains, particularly for energy, food, and fertilizers. The effect of the conflict on global fertilizer prices has been especially pronounced in Africa. This brief looks at the immediate effects of the Ukraine war on local fertilizer prices and its likely impact on food production.

- Even before the outbreak of war in Ukraine, fertilizers prices across Africa were higher compared to other regions of the world. Due to this reason, farmers are shifting to organic fertilizers, and the area of organic farmland in Africa has doubled in the last decade to 2.1 million hectares. According to FiBL, the most prominent organic centers are in North and East Africa. In Kenya, nuts and coconuts dominate organic output. In Tunisia, it is olives. Ethiopia and Tanzania are big coffee growers, while Uganda is home to the most organic producers in Africa, the crop of choice is cacao.

- According to data from the Research Institute of Organic Agriculture (FiBL), in a continent where natural agricultural and subsistence farming are widely practiced. Farmers who avoid synthetic fertilizers and pesticides but are unable to get organic certificates to say high costs, corruption, and little government support stymie their plans to export abroad.

- The focus on organic cultivation and the need for sustainable farming practices are the major reasons for Africa's increasing consumption of organic fertilizers. Various government subsidies and initiatives in developing countries for sustainable organic farming are expected to maintain continuous growth in the market. More awareness among the farmers is needed to maintain the growth of the market. The developing and untapped markets in Africa would provide substantial growth opportunities.

Africa Organic Fertilizers Market Trends

Popularity for the Organic Farming Drives the Market

- Africa has the highest population with the largest arable land. For instance, the Sub-Saharan African region has 13% of the world's population and approximately 20% of the global agricultural land. However, the region is facing severe food insecurity primarily due to inadequate food production. The lack of access to mechanization in farming and limited use of fertilizers due to less farmer buying power are driving the demand for alternative cost-effective fertilizers, such as organic fertilizers, in the region.

- Organic farming in Africa has been increasing at a significant rate. According to FiBL, the area under organic permanent crops are 374,118 thousand hectares in 2021. There are more than 3.8 million hectares of certified organic agricultural land in Africa, constituting about 2.8% of the world's organic agricultural land. The most important organic permanent crops grown in Africa are nuts (mainly cashew nuts), which were grown on an area of over 291,000 hectares, followed by olives, coffee, and cocoa, each with an area above 200,000 hectares in 2020.

- The countries with the largest permanent crop areas were Tunisia (mainly olives), which reported an area of nearly 269,000 hectares, followed by Sierra Leone, Ethiopia (mainly coffee), Congo (cocoa and coffee), and Kenya (mainly nuts), with the latter reaching an area of nearly 113,000 hectares. As organic cultivation only uses biological organic fertilizers, increasing organic farming will boost the African market.

South Africa Dominates the Market

- South Africa is the top country among all the African countries in terms of the revenue generated from the biofertilizer segment. Factors like environmental concerns, increasing awareness among the farmers, and degrading soil quality, are the major market drivers in the region.

- According to Food and Agriculture Organization (FAO), the consumption of fertilizers in South Africa increased from 70.4 Kg per hectare in 2018 to 72.8 Kg per hectare in 2020. Over the years, more chemical fertilizers consumption than recommended levels has led to soil acidification. Thus, more organic fertilizers are needed to correct the PH value of the soil. In addition, the country's organic land has been increasing.

- For instance, the organic land in 2020 was 40,954 thousand hectares and has increased to 97,359 thousand hectares by 2021. Updated Production needs to be increased on low fertile soil with a high amount of organic fertilizers. This enhances the nutrient availability of crop plants (by processes like fixing atmosphere N or dissolving P present in the soil), thus, imparting better health to crops and soil, thereby enhancing crop yields, which, in turn, may drive the organic fertilizer market during the forecast period.

- Regional and global players manufacturing biofertilizers in South Africa are also one of the major factors boosting the market in South Africa.

Africa Organic Fertilizers Industry Overview

The African organic fertilizer market needs to be more cohesive, with number of local and international players. The major players in the African organic fertilizers market are Rizobacter Argentina SA, Novozymes AS, Symborg, International Panaacea Limited, and MBFI. Collaborations with government organizations and expansion in the market, along with product innovation, are some of the strategies adopted by the companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Microorganisms

- 5.1.2 Organic Residues

- 5.2 Application type

- 5.2.1 Grains and Cereals

- 5.2.2 Pulses and Oilseeds

- 5.2.3 Fruits and Vegetables

- 5.2.4 Commercial crops

- 5.2.5 Other Crop Types

- 5.3 Geography

- 5.3.1 South Africa

- 5.3.2 Ethiopia

- 5.3.3 Egypt

- 5.3.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Rizobacter Argentina SA

- 6.3.2 Novozymes AS

- 6.3.3 Company C

- 6.3.4 International Panaacea Limited

- 6.3.5 MBFI

- 6.3.6 T Stanes & Company Limited

- 6.3.7 Camson Bio Technologies Limited

- 6.3.8 Biomax

- 6.3.9 Agri Life

- 6.3.10 Bio Protan

7 MARKET OPPORTUNITIES AND FUTURE TRENDS