PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689883

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1689883

Substation Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

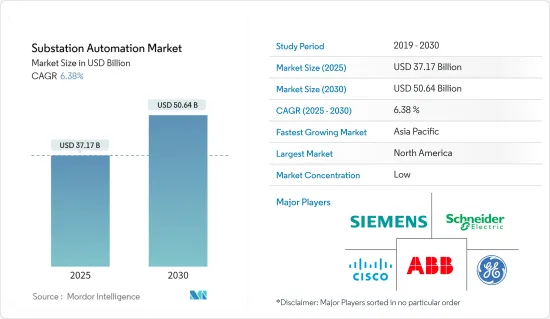

The Substation Automation Market size is estimated at USD 37.17 billion in 2025, and is expected to reach USD 50.64 billion by 2030, at a CAGR of 6.38% during the forecast period (2025-2030).

Key Highlights

- A substation automation system is usually referred to as a collection of hardware and software components integrated to control or monitor an electrical system, both locally and remotely. Substation automation systems are also used to automate tedious, repetitive, and error-prone activities to increase the overall productivity and efficiency of the comprehensive system.

- Substation automation provides protection, control, automation, monitoring, and communication capabilities as a part of a comprehensive substation control and monitoring solution. A substation layout should be clean so that the user can eliminate entire writing racks and cabinets or make them much smaller depending on how the user handles their I/Os to the IEDs (intelligent electronic devices). High-speed microprocessor-based remote terminal units or smart electronic devices are used for substation automation and protection.

- A smart grid is an electricity network that employs digital and other advanced technologies to monitor and manage electricity transport from all generation sources to meet the electricity needs of end users. To operate every system component as efficiently as possible, smart grids coordinate the needs and capabilities of all generators, grid operators, end users, and electricity market stakeholders. This maximizes system reliability, resilience, flexibility, and stability while minimizing costs and environmental impacts.

- The surge in demand for electricity is supported by factors such as the increasing propensity of consumers to low-carbon alternatives to traditional products, such as heat pumps and electric vehicles. Furthermore, companies operating in heavily polluting industries, including steel, plastics and polymers, and transportation, are also looking for electrification to enhance sustainability.

- Although the demand for substation automation is growing, cost continues to remain among the major challenging factors for the market's growth. For instance, installing a full-scale automation system in a substation requires significant initial investment considering the large number of components being used, including SCADA, sensors, RTUs, IEDs, HMIs, servers, etc.

- In September 2023, Moxa introduced the new MGate5119 Series IEC 61850 gateway, simplifying system integrations and enhancing communication security for power substations. This substation gateway provides DNP3/IEC 101/IEC 104/Modbus-to-IEC 61850 protocol conversions, easy-to-use functions to simplify configuration and troubleshooting, security-hardened features based on the IEC 62443 and NERC CIP standards, and a protocol encryption function to enhance communication security. With these features, the MGate5119 Series IEC 61850 gateway is perfect for substation retrofit projects.

Substation Automation Market Trends

The Industrial Sector is Expected to Witness Significant Growth

- Substation automation systems are commonly utilized in industries where energy availability is of utmost importance, including oil and gas, transportation, mining, steel, and others. Employing substation automation systems can benefit companies by preventing power outages, minimizing maintenance expenses, enhancing plant productivity, promoting worker safety, and more.

- Due to the increasing demand from various industries such as utility, steel, mining, and others, suppliers of substation automation equipment are expected to benefit significantly in the future. In the metal and mining industry, it is utilized to monitor and regulate power distribution systems. The oil and gas industry also gains advantages from substation automation as it allows for remote monitoring and control of electrical infrastructure.

- In addition, transportation industries rely on this service to manage power systems in their facilities effectively. Furthermore, other sectors use this application for efficient power management and control.

- The emergence of industry 4.0 trends has significantly enhanced the demand for automation and robotics solutions for different industrial applications, creating a favorable ecosystem for the market's growth by influencing the electricity demand. For instance, according to the World Robotics Report 2023 by the International Federation of Robotics, the annual installation of industrial robots is anticipated to witness growth globally. However, demand across the Asia-Pacific region is expected to remain the highest, growing from 385 thousand units in 2021 to 539 thousand by 2026.

- Artificial intelligence is poised to transform the industrial substation automation market significantly. AI drives significant growth and innovation through predictive maintenance, improved decision-making, and optimized integration of renewable energy sources. A survey released by IBM in 2024 revealed that 74% of surveyed industrial companies have either already implemented or are considering AI integration in their operations. With industrial users and renewable energy providers increasingly embracing AI solutions, the substation automation market is poised for significant growth, solidifying AI's role in shaping the future power grid.

Asia-Pacific is Expected to Witness the Fastest Growth

- Asia-Pacific will experience robust growth in the future, primarily driven by the rising need for rural electrification and the adoption of renewable energy sources, contributing to the enhanced safety and efficiency of stations. Moreover, the presence of companies dedicated to promoting top-quality electronic products will further bolster the progress.

- The growth of smart grids in the market is driven by factors such as the rising demand for efficient electricity transmission, the need for reduced operations and management costs for utilities, and the objective of lower power costs for consumers. Moreover, the growth of smart grids in substation automation is fueled by the increasing integration of large-scale renewable energy systems and enhanced security measures.

- To cater to the diverse electricity requirements of end users, a smart grid is an electricity network that utilizes digital and other advanced technologies to effectively monitor and regulate the transportation of electricity from different sources of generation. Smart grids aim to optimize the functioning of every element within the system by coordinating the needs and capabilities of generators, grid operators, end users, and stakeholders in the electricity market. This approach enhances the system's reliability, resilience, flexibility, and stability while reducing costs and environmental impacts.

- China is recognized as the largest market globally for power transmission and distribution (T&D) and is also on track to become a significant adopter of smart grid technology. This aligns with its commitment to reducing carbon emissions and promoting sustainable development. China aspires to become a global leader in electrical power equipment by 2025, as stated in its national strategy outlined in the Technology Roadmap (2017) of the Made in China 2025 program. The program strongly emphasizes innovation and technology, with substantial funding allocated toward supporting its development.

- Moreover, India has taken the lead in mobilizing global action for long-term development. To combat climate change, the country has taken significant steps to reduce its national carbon footprint and reliance on fossil fuels. As a result, it is only natural that the country accelerates its efforts toward smart metering and the digitalization of its grid networks. India has set a goal of achieving net zero emissions by 2070 and obtaining 50% of its energy needs from renewable sources by 2050, raising the possibility of the national electricity grid being developed to handle demand-side flexibility and integration variability.

Substation Automation Industry Overview

The substation automation market is fragmented and appears to be highly competitive. Market leaders are investing in research and development to innovate their products continuously and are increasingly seeking market expansion through various strategic mergers and acquisitions, innovation, and a cost-effective product portfolio. Some of the key players in the market include ABB Limited, Siemens AG, Schneider Electric SE, General Electric Co., Cisco Systems Inc., and Eaton Corporation.

November 2023: Eaton announced the opening of its new Global Innovation Center near Montreal in Brossard, Quebec, worth USD 3 billion. It focuses its efforts on accelerating R&D in Distributed Energy Resources Technology to promote the development of technologies that enable electricity grids to generate power from renewable energy sources. The company continuously invests in high-growth, high-margin businesses to meet the customers' changing needs and strengthen its product portfolio.

June 2023: GE Grid Solutions secured a contract with Larsen & Toubro to supply three 380 kV T155 gas-insulated switchgear (GIS) substations for the largest utility-scale green hydrogen plant in Saudi Arabia. By the end of 2026, NEOM Green Hydrogen Company intends to produce carbon-free hydrogen using wind and solar energy at its plant, with a production capacity of up to 600 tons per day.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Need to Upgrade the Existing Networks

- 5.1.2 Innovations in Substation Automation Components/Technologies

- 5.2 Market Restraint

- 5.2.1 High Cost of Installation and Cyber Security Concerns

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Transmission

- 6.1.2 Distribution

- 6.2 By Module

- 6.2.1 Intelligent Electronic Devices (IED)

- 6.2.2 Remote Terminal Unit (RTU)

- 6.2.3 Bay Control Unit (BCU)

- 6.2.4 Supervisory Control and Data Acquisition (SCADA)

- 6.3 By Communication

- 6.3.1 Wired

- 6.3.2 Wireless

- 6.4 By Stage

- 6.4.1 Retrofit

- 6.4.2 New

- 6.5 By End User

- 6.5.1 Utility

- 6.5.2 Industry

- 6.6 By Geography

- 6.6.1 North America

- 6.6.2 Europe

- 6.6.3 Asia

- 6.6.4 Australia and New Zealand

- 6.6.5 Latin America

- 6.6.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Limited

- 7.1.2 Siemens AG

- 7.1.3 Schneider Electric SE

- 7.1.4 General Electric Co.

- 7.1.5 Cisco Systems Inc.

- 7.1.6 Eaton Corporation

- 7.1.7 NovaTech LLC

- 7.1.8 Belden Inc.

- 7.1.9 ARTECHE

- 7.1.10 Honeywell International

- 7.1.11 Schweitzer Engineering Laboratories

- 7.1.12 Hitachi Energy Ltd

- 7.1.13 Ingeteam

- 7.1.14 Ashida Electronics Pvt. Ltd

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS