PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644852

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1644852

Europe Mobile Payments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

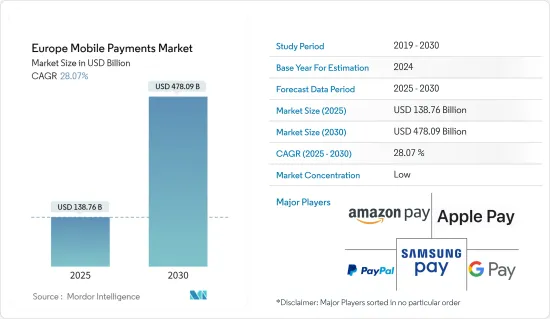

The Europe Mobile Payments Market size is estimated at USD 138.76 billion in 2025, and is expected to reach USD 478.09 billion by 2030, at a CAGR of 28.07% during the forecast period (2025-2030).

The Europe mobile payments market is undergoing a remarkable transformation, propelled by increased digitalization across industries. Mobile wallets and contactless payments are fundamentally changing how consumers and businesses conduct financial transactions. As digital ecosystems expand, mobile payment solutions have become integral to the payment landscape in Europe. The convenience, speed, and advanced security features that mobile payments offer are major drivers of their growing adoption. Furthermore, the push towards cashless economies by both governments and businesses accelerates the transition from traditional payment methods to digital ones.

Rising Mobile Payment Integration Across Sectors

Key Highlights

- Mobile payments have made significant inroads into various industries, including retail, e-commerce, transportation, and peer-to-peer (P2P) payments. Contactless payment methods, powered by Near-Field Communication (NFC), have facilitated secure and swift transactions, minimizing the friction traditionally associated with cash or card payments. The growing penetration of smartphones and the expansion of mobile banking platforms have been key in driving the mobile payment industry forward. Moreover, major industry leaders such as Google Pay, Apple Pay, and PayPal have capitalized on loyalty programs and real-time payment features to bolster consumer adoption.

- However, the market faces challenges such as security concerns and a lack of awareness regarding the use of mobile payment tools, which remain barriers to full-scale market penetration. Nevertheless, the advantages of mobile payments-particularly instant payments and seamless peer-to-peer transfers-are anticipated to sustain growth across the region.

Widespread Digitalization Accelerates Mobile Payment Adoption

Key Highlights

- Digital Shift Fuels Market Expansion: The digital transformation in Europe is redefining the payment landscape. As both businesses and consumers transition to digital platforms, mobile payments have become a central component of this shift. Key sectors like retail, transportation, and online shopping are integrating mobile payment solutions to offer better convenience and user experiences. Mobile banking has also allowed seamless integration between bank accounts and mobile wallets, facilitating faster and more secure transactions.

- Leading Countries in Mobile Payment Adoption: The UK, Germany, and France are at the forefront of mobile payment adoption, driven by governmental initiatives encouraging cashless economies. With the proliferation of smartphones and mobile apps, accessibility to mobile payments is steadily increasing. Additionally, 5G technology is boosting mobile payment capabilities, enabling faster transaction speeds and further cementing mobile payments as the preferred method of transaction in Europe.

- E-commerce Embraces Mobile Payments: E-commerce platforms have increasingly integrated mobile wallets, encouraging consumers to use them during checkout. The accessibility of mobile payment options is further enhanced by user-friendly interfaces and secure authentication methods. This trend underscores the growing reliance on mobile payments for everyday transactions, positioning mobile payment solutions as a vital component of Europe's digital economy.

Rewards and Instant Payments Drive Market Growth

Key Highlights

- Incentives Boost Mobile Payment Adoption: Reward strategies and loyalty programs have been crucial in driving the adoption of mobile payments. Companies like PayPal, Apple Pay, and Samsung Pay offer users rewards such as cashback and discounts, which incentivize continued use of their platforms. This approach not only helps retain customers but also encourages repeat transactions, further embedding mobile payments into the consumer lifestyle.

- Real-Time Payments Increase Popularity: The growing availability of real-time payment systems across Europe is another major factor behind the market's rapid growth. Instant payments allow consumers to complete transactions in seconds, aligning with modern preferences for fast and efficient services. These systems are also playing a significant role in peer-to-peer payments, further broadening the use cases for mobile payments. As financial institutions collaborate with mobile payment providers to integrate these systems, both consumers and merchants are benefitting from the enhanced speed and convenience of transactions.

- Countries such as Germany and France, where digital banking is well-established, have embraced real-time payment features in mobile apps. The ongoing development of initiatives like the European Payment Initiative (EPI) illustrates the region's commitment to promoting faster, more secure digital payments.

Europe Mobile Payments Market Trends

E-commerce to Drive the Mobile Payments Market

- E-commerce Drives Mobile Payments Market: The rapid growth of e-commerce is a critical driver for the mobile payments market in Europe. Mobile payment methods, which offer speed and convenience, are increasingly preferred by consumers. By 2024, m-commerce revenue in Europe is forecasted to reach USD134.37 billion. The widespread use of digital wallets such as Apple Pay, Google Pay, and PayPal is particularly prominent in countries like Germany, where 44% of all domestic transactions are now completed through digital wallets.

- Increasing Adoption of Mobile Wallets: As smartphone penetration continues to rise, mobile wallets are becoming the go-to payment method for many Europeans, replacing traditional options. In Germany, PayPal dominates digital payments with 83% of the market share, while mobile devices account for 20% of in-store transactions. The broader shift toward a cashless society, which has been accelerated by the COVID-19 pandemic, is also fueling the demand for peer-to-peer payment apps like Venmo and Revolut.

- Security Innovations Strengthen Market Trust: The success of mobile payments hinges on consumer trust, which is being bolstered by advancements in security technologies such as encryption, biometric authentication, and tokenization. These measures ensure that mobile transactions are secure, contributing to the growing confidence in mobile payment platforms. Additionally, real-time payment systems offer immediate transfers, enhancing the user experience and solidifying the reliability of mobile payments as a mainstream financial tool.

- Expansion Supported by Digital Growth: The mobile payments market in Europe is one of the fastest-growing globally, with the UK, France, and Germany leading the charge. In 2022, the UK experienced a 50% increase in contactless payments, showcasing the region's enthusiastic embrace of mobile solutions. As consumers shift away from cash, the market is set to continue expanding, supported by regulatory initiatives and innovations in payment technologies.

United Kingdom Expected to Hold Major Market Share

- UK Leads in Mobile Payment Adoption: The United Kingdom is expected to maintain its position as a leader in Europe's mobile payments market due to its advanced digital infrastructure and high rate of mobile wallet usage. Widespread use of contactless payments and NFC technology has fueled market growth, with companies like Revolut and Monzo continually innovating to enhance user experiences.

- Regulatory Support Drives Growth: The UK government's supportive regulatory environment has been instrumental in promoting digital payments. Initiatives such as open banking and frameworks supporting cashless transactions have accelerated the adoption of real-time and NFC payments, resulting in a fast and secure mobile payment ecosystem.

- Contactless Payments Dominate UK Transactions: Contactless payments have become the norm in the UK, with 50% of transactions now being made via contactless methods as of 2022. The increasing use of mobile wallets in sectors such as retail, hospitality, and public transportation has improved the consumer experience and reduced dependence on physical currency, driving market growth further.

- Forecasted Growth in UK Mobile Payments Market: The UK's mobile payments market is forecasted to continue growing steadily, with projections suggesting that cash payments will account for only 6% of total transactions by 2031. This shift highlights the country's strong momentum towards a cashless society, cementing its role as a key player in mobile payment innovations across Europe.

Europe Mobile Payments Industry Overview

Fragmented Market with Diverse Players: The mobile payments market in Europe is highly fragmented, with a mix of global and regional players competing for market share. While global giants like Google Pay, Apple Pay, and PayPal dominate the landscape, smaller regional platforms are also finding their niche. This diversity in payment preferences and regulatory environments across Europe ensures that both large conglomerates and specialized firms have opportunities to succeed.

Global Leaders Drive Market Innovation: Major players such as Google Pay, Apple Pay, and PayPal are leveraging their brand recognition and extensive ecosystems to dominate the European mobile payments market. Their strong presence is reinforced by advanced security features and seamless cross-platform integration, allowing them to maintain a competitive edge. However, there is also room for innovation from smaller competitors like Klarna and niche players such as Fitbit Pay and Garmin Pay, which cater to specific user needs.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHT

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of the Digitalization in Europe

- 5.1.2 Pay-backs and Reward Strategies to Boost Market Growth

- 5.1.3 Instant payments are becoming increasingly widespread

- 5.2 Market Challenges / Restrain

- 5.2.1 Lack of Knowledge to Operate the Tool

- 5.2.2 Security Concerns and Inconvenience of Using Cash to Impact Mobile-based Transaction

6 MARKET SEGMENTATION

- 6.1 Payment Mode

- 6.1.1 Proximity Payment

- 6.1.2 Remote Payment

- 6.2 By Country

- 6.2.1 United Kingdom

- 6.2.2 Germany

- 6.2.3 France

- 6.2.4 Italy

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Google Pay

- 7.1.2 Apple Pay

- 7.1.3 Amazon Pay

- 7.1.4 Paypal

- 7.1.5 Samsung Pay

- 7.1.6 Klarna

- 7.1.7 Fitbit Pay

- 7.1.8 Garmin Pay

- 7.1.9 Bit Pay

- 7.1.10 Bluecode

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET