PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445764

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445764

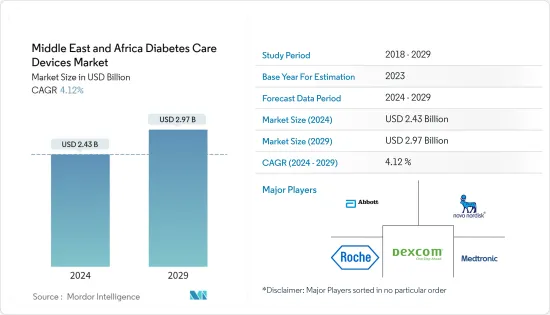

Middle East and Africa Diabetes Care Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Middle East and Africa Diabetes Care Devices Market size is estimated at USD 2.43 billion in 2024, and is expected to reach USD 2.97 billion by 2029, growing at a CAGR of 4.12% during the forecast period (2024-2029).

The market is estimated to reach a value of more than USD 2.7 billion by 2027.

The COVID-19 pandemic positively impacted the Middle East and Africa diabetes care devices market growth. Patients with diabetes, infected with COVID-19 may experience elevated blood glucose, abnormal glucose variability, and diabetic complications. The prevalence of diabetes in people with COVID-19 caused a significant increase in severity and mortality of COVID-19 in people with either type 1 (T1DM) or type 2 diabetes mellitus (T2DM), especially in association with poor glycemic control. While new-onset hyperglycemia and new-onset diabetes (both T1DM and T2DM) have been increasingly recognized in the context of COVID-19 and have been associated with worse outcomes. To avoid aggravation, a patient's blood glucose should be monitored regularly, which has underlined the importance of self-monitoring blood glucose devices. Pandemic emergency has created a rise in remote care from both patients and providers and removed many long-standing regulatory barriers.

73 million adults (20-79) are living with diabetes in the IDF MENA Region in 2021. This figure is estimated to increase to 95 million by 2030. 48 million adults in the IDF MENA Region are living with Impaired Glucose Tolerance, which places them at increased risk of developing type 2 diabetes. Diabetes is responsible for 796,000 deaths in the IDF MENA Region in 2021. USD 33 billion was spent on healthcare for people with diabetes in 2021.

The Middle East and Africanregion had witnessed an alarming increase in the prevalence of diabetes, in recent years, the rate of diabetes is at an all-time high, mainly due to lifestyle changes. Diabetes is associated with many health complications. Patients with diabetes require many corrections throughout the day to maintain nominal blood glucose levels, such as administering additional insulin or ingesting additional carbohydrates by monitoring their blood glucose levels. Diabetes poses an emerging healthcare burden across the region.

Owing to the aforementioned factors the studied market is anticipated to witness growth over the analysis period.

Middle East And Africa Diabetes Care Devices Market Trends

Continuous glucose monitoring segment is expected to witness highest growth rate over the forecast period

The continuous glucose monitoring segment is expected to register a CAGR of 16.8% over the forecast period.

Continuous glucose monitoring devices are automated glucose monitoring systems that consist of a small device that can be worn on the body and held on by an adhesive patch. The sensor part of the device has a cannula that is inserted into the top layer of skin and uses samples of interstitial fluid to check glucose levels. Sensors are connected to a transmitter that can send data wirelessly to a dedicated mobile receiving device or smartphone. The use of CGMs by people with diabetes and their caregivers and communities is beneficial for managing their blood glucose and insulin levels and maintaining their health outcomes. CGM makes it significantly easier to manage blood glucose levels by decreasing interruptions, allowing for better sleep, and improving the mental health of patients or caregivers by reducing the overall mental load of managing diabetes.

Continuous glucose monitoring sensors use glucose oxidase to detect blood sugar levels. Glucose oxidase converts glucose to hydrogen peroxidase, which reacts with the platinum inside the sensor, producing an electrical signal to be communicated to the transmitter. Continuous glucose monitoring has become a popular alternative to the portable finger-prick glucometers available on the market for the convenience of diabetic patients. Sensors are the most important part of continuous glucose monitoring devices. A large variety of promising glucose-sensing technologies, from traditional electrochemical-based glucose sensors to novel optical and other electrical glucose sensors, have been developed, which has had a positive impact on market growth. Technological advancements to improve the accuracy of the sensors are expected to drive segment growth during the forecast period.

Governments in the Middle East have identified the threat of diabetes and started to respond with various policies, initiatives, and programs. Six out of 15 countries in this region still do not have a national operational action policy for diabetes. Many countries still do not have a national strategy to reduce overweight, obesity, and physical inactivity, which are important risk factors for diabetes. Most counties have fully implemented national diabetes treatment guidelines. However, constant measures are being taken to minimize diabetic complications; therefore, owing to the aforesaid factors, the growth of the studied market is anticipated in the Middle East and African region.

Saudi Arabia is expected to witness highest CAGR in the Middle East and Africa Diabetes Care Devices Market over the forecast period

Saudi Arabia is expected to register the highest CAGR of about 5.08% in the Middle East and Africa Diabetes Care Devices Market over the forecast period.

More than one in ten people in Saudi Arabia were living with diabetes, and the prevalence of the disease was expected to almost double by 2045, according to the 2021 report of the International Diabetes Federation. The report mentioned that 4.27 million people in Saudi Arabia have diabetes. The rise in the number of people with type-2 diabetes is driven by a complex interplay of socio-economic, demographic, environmental, and genetic factors. Key contributors include urbanization, an aging population, decreasing levels of physical activity, and increased levels of overweight and obesity.

The Saudi government announced in July 2022 that Saudi Arabia saw growing demand for quality healthcare services spurred by changes, including an increasing and aging population and a growing prevalence of lifestyle diseases such as diabetes and obesity. The government and private sector are both involved in working on healthcare entities, certifications, and regulations. The government is taking steps to have 100 percent of Saudi citizens covered by insurance and is working towards ensuring affordability, access, and quality digital healthcare and primary care with cost-effectiveness.

Therefore, owing to the aforesaid factors, the growth of the studied market is anticipated in the Middle East and Africa region.

Middle East And Africa Diabetes Care Devices Industry Overview

The Middle East and African diabetes care device market is moderately fragmented, with few significant and generic players. There have been constant innovations driven by manufacturers to compete in the market. The major players, such as Abbott and Medtronic, have undergone many mergers, acquisitions, and partnerships to establish market dominance while also adhering to organic growth strategies, which is evident from their R&D spending.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Monitoring Devices

- 5.1.1 Self-monitoring Blood Glucose Devices

- 5.1.1.1 Glucometer Devices

- 5.1.1.2 Blood Glucose Test Strips

- 5.1.1.3 Lancets

- 5.1.2 Continuous Glucose Monitoring Devices

- 5.1.2.1 Sensors

- 5.1.2.2 Durables (Receivers and Transmitters)

- 5.1.1 Self-monitoring Blood Glucose Devices

- 5.2 Management Devices

- 5.2.1 Insulin Pumps

- 5.2.1.1 Insulin Pump Monitor

- 5.2.1.2 Insulin Pump Reservoir

- 5.2.1.3 Insulin Infusion Sets

- 5.2.2 Insulin Syringes

- 5.2.3 Insulin Disposable Pens

- 5.2.4 Insulin Cartridges in Reusable Pens

- 5.2.5 Jet Injectors

- 5.2.1 Insulin Pumps

- 5.3 Geography

- 5.3.1 Saudi Arabia

- 5.3.2 Iran

- 5.3.3 Egypt

- 5.3.4 Oman

- 5.3.5 South Africa

- 5.3.6 Rest of Middle East and Africa

6 MARKET INDICATORS

- 6.1 Type-1 Diabetes Population

- 6.2 Type-2 Diabetes Population

7 COMPETITIVE LANDSCAPE

- 7.1 COMPANY PROFILES

- 7.1.1 Dexcom Inc.

- 7.1.2 Insulet Corporation

- 7.1.3 Medtronic PLC

- 7.1.4 Roche Diabetes Care

- 7.1.5 Novo Nordisk A/S

- 7.1.6 Ascensia Diabetes Care

- 7.1.7 Agamatrix Inc.

- 7.1.8 Bionime Corporation

- 7.1.9 Lifescan

- 7.1.10 Abbott Diabetes Care

- 7.1.11 Eli Lilly

- 7.1.12 Sanofi

- 7.1.13 Rossmax

- 7.2 COMPANY SHARE ANALYSIS

- 7.2.1 Self-monitoring Blood Glucose Devices

- 7.2.1.1 Abbott Diabetes Care

- 7.2.1.2 Roche Diabetes Care

- 7.2.1.3 LifeScan

- 7.2.1.4 Other Self-monitoring Blood Glucose Devices

- 7.2.2 Continuous Glucose Monitoring Devices

- 7.2.2.1 Dexcom Inc.

- 7.2.2.2 Medtronic PLC

- 7.2.2.3 Abbott Diabetes Care

- 7.2.2.4 Other Continuous Glucose Monitoring Devices

- 7.2.3 Insulin Devices

- 7.2.3.1 Insulet Corporation

- 7.2.3.2 Novo Nordisk A/S

- 7.2.3.3 Other Insulin Devices

- 7.2.1 Self-monitoring Blood Glucose Devices

8 MARKET OPPORTUNITIES AND FUTURE TRENDS