PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836645

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836645

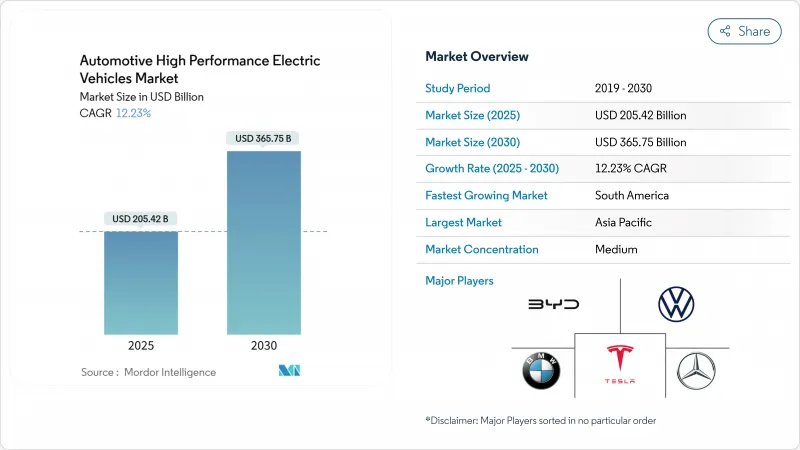

Automotive High Performance Electric Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Automotive High Performance Electric Vehicles Market size is estimated at USD 205.42 billion in 2025, and is expected to reach USD 365.75 billion by 2030, at a CAGR of 12.23% during the forecast period (2025-2030).

Continued cost declines in battery packs, rapid 800 V platform diffusion, and a new wave of tri- and quad-motor models position the automotive high performance EVs market for sustained double-digit expansion. Consumer interest in vehicles that deliver both near-silent operation and super-car-level acceleration is reinforcing premium pricing power, while governments use zero-emission mandates and purchase subsidies to pull forward demand.

Global Automotive High Performance Electric Vehicles Market Trends and Insights

Battery Cost Decline & 800 V Adoption

NMC and NCA cell prices continued falling below USD 90 kWh in 2025 as Tesla's 4680 line hit volume production and Chinese suppliers commercialized 6C-charge packs, shrinking pack-level cost structures by double digits. Eight-hundred-volt architectures pioneered by the Porsche Taycan now permeate premium segments, slicing DC fast-charge sessions by 40% and allowing lighter cabling that offsets added motor mass. Silicon-carbide MOSFET inverters from Infineon and Wolfspeed drop switching losses for tri- and quad-motor layouts, supporting 10-minute full charges without thermal derate. The combined effect propels the automotive high performance EVs market toward broader affordability while sustaining ultra-high power outputs.

Government Incentives & Emission Norms

The U.S. Inflation Reduction Act grants up to USD 7,500 per vehicle, complemented by state rebates that trim effective transaction prices by as much as USD 15,000. The European Union's Fit-for-55 package legally binds a 55% fleet-average CO2 cut by 2030, compelling OEMs to lean into high performance EV volume to counterbalance residual ICE output. China's dual-credit regime pushed BYD deliveries to 4.27 million units in 2024, more than doubling its EV tally in two years.

Thermal-management Limits

Current lithium-ion packs lose capacity rapidly above 60 °C, and extreme duty cycles in multi-motor setups can push cells to these thresholds in minutes. Liquid-cooling plates, phase-change composites, and refrigerant-based chillers add cost, weight, and service complexity. In the Persian Gulf, summer ambient temperatures already trim real-world range by up to 20% during spirited driving. OEMs are exploring structural cooling and immersion methods, yet short-term capex remains a hurdle for the automotive high performance EVs market.

Other drivers and restraints analyzed in the detailed report include:

- Ultra-fast Charging Corridors

- SiC Inverters for Track Duty

- Rare-earth Price Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery Electric Vehicles secured 71.27% of 2024 revenue, underscoring buyer preference for pure-electric thrust and simplified drivetrains. BEVs exploit instant torque and finer power modulation, exemplified by the Xiaomi SU7 Ultra's Nurburgring benchmark lap. The segment also benefits from lighter maintenance demand and OTA-driven performance tuning. Meanwhile, Plug-in Hybrid Electric Vehicles are expanding at a 13.26% CAGR, appealing to enthusiasts in regions where 350 kW public chargers remain scarce.

Europe's stricter CO2 fleet averages make PHEVs attractive for compliance, and premium marques integrate track-oriented electric boost modes that deliver sustained lap performance. Tax regimes in Germany and the U.K. favor PHEVs for company fleets, propelling adoption among executive buyers.

Passenger cars commanded 84.74% of 2024 revenue of the automotive high performance EVs market size, propelled by sports sedans and luxury SUVs that now out-accelerate legacy supercars. Battery floor mounting drops centers of gravity, and torque vectoring enhances handling, enabling Mercedes-AMG, BMW M, and Audi Sport to offer sub-3-second 0-60 mph times with four-door practicality. Customer willingness to pay for software-unlock extras further fortifies margins.

Commercial vehicles, led by performance-oriented pickups and delivery vans, record a 12.75% CAGR through 2030. Fleet managers appreciate torque for towing and payload while benefiting from lower fuel and service bills. Rivian's R1T and Ford's F-150 Lightning prove that workhorse fleets can extract premium value from propulsion systems designed for extremes. As duty-cycle data feeds predictive maintenance, residuals improve, inviting institutional capital into the automotive high performance EVs market.

The Automotive High Performance EVs Market Report is Segmented by Drive Type (Battery Electric and Plug-In Hybrid Electric), Vehicle Type (Passenger Cars and Commercial Vehicles), Motor Type (Permanent-Magnet Synchronous, Induction, and More), Battery Chemistry (Lithium-Ion (NMC/NCA) and More), Powertrain Architecture (Single-Motor RWD and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated with 46.85% 2024 revenue share, anchored by China where electric vehicles are slated to reach 60% of total light-duty sales in 2025. Japan remains hybrid-skewed, yet South Korea and Australia witness double-digit growth under expanded purchase rebates and 350 kW highway charger deployments. Integrated supply chains allow battery, inverter, and chip suppliers to co-locate, compressing lead times and securing a structural price edge for the automotive high performance EVs market in the region.

Europe rebounded with around 30% BEV sales growth in Q1 2025 after a 2024 plateau, supported by joint public-private funding that targets one million public charge points by 2030. Germany and the U.K. posted a decent respective gains, benefiting from residual-value guarantees and Formula E technology spillovers. Mexico's planned mini-EV hub for 2030 integrates NAFTA content rules and low labor costs, creating a contiguous supply belt that reinforces regional competitiveness. Such build-local trends align with national security narratives, shielding the automotive high performance EVs market from distant supply disruptions.

South America delivered the fastest 13.17% CAGR outlook as Latin American EV registrations doubled units in 2024. Uruguay tops regional per-capita adoption; Brazil cut import tariffs to accelerate domestic assembly programs, and Paraguay eyes battery-grade lithium business anchored on hydropower. Yet charging coverage remains patchy outside capital corridors, prompting fleets to prioritize depot-based operations. As renewable generation expands, the automotive high performance EVs market should find fertile ground in clean-energy branding for premium imports.

- Tesla

- BYD Auto

- Volkswagen Group

- BMW Group

- Mercedes-Benz Group

- General Motors

- Ford Motor Company

- Stellantis NV

- Hyundai Motor Group

- Toyota Motor Corporation

- Nissan Motor Co.

- Lucid Group

- Rivian Automotive

- Rimac Automobili

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Battery cost decline & 800 V adoption

- 4.2.2 Government incentives & emission norms

- 4.2.3 Ultra-fast charging corridors

- 4.2.4 SiC inverters for track duty

- 4.2.5 EV-only racing halo

- 4.2.6 OTA performance-upgrade revenue

- 4.3 Market Restraints

- 4.3.1 Thermal-management limits

- 4.3.2 Rare-earth price risk

- 4.3.3 Insurance-premium spike

- 4.3.4 Grid bottlenecks for MW chargers

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment & Funding Trends

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Drive Type

- 5.1.1 Battery Electric (BEV)

- 5.1.2 Plug-in Hybrid Electric (PHEV)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 By Motor Type

- 5.3.1 Permanent-Magnet Synchronous

- 5.3.2 Induction

- 5.3.3 Switched Reluctance

- 5.3.4 Axial Flux

- 5.4 By Battery Chemistry

- 5.4.1 Lithium-ion (NMC/NCA)

- 5.4.2 Lithium Iron Phosphate (LFP)

- 5.4.3 Solid-state & Semi-solid

- 5.5 By Powertrain Architecture

- 5.5.1 Single-Motor RWD

- 5.5.2 Dual-Motor AWD

- 5.5.3 Tri-/Quad-Motor AWD

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Tesla

- 6.4.2 BYD Auto

- 6.4.3 Volkswagen Group

- 6.4.4 BMW Group

- 6.4.5 Mercedes-Benz Group

- 6.4.6 General Motors

- 6.4.7 Ford Motor Company

- 6.4.8 Stellantis NV

- 6.4.9 Hyundai Motor Group

- 6.4.10 Toyota Motor Corporation

- 6.4.11 Nissan Motor Co.

- 6.4.12 Lucid Group

- 6.4.13 Rivian Automotive

- 6.4.14 Rimac Automobili

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment