PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842523

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842523

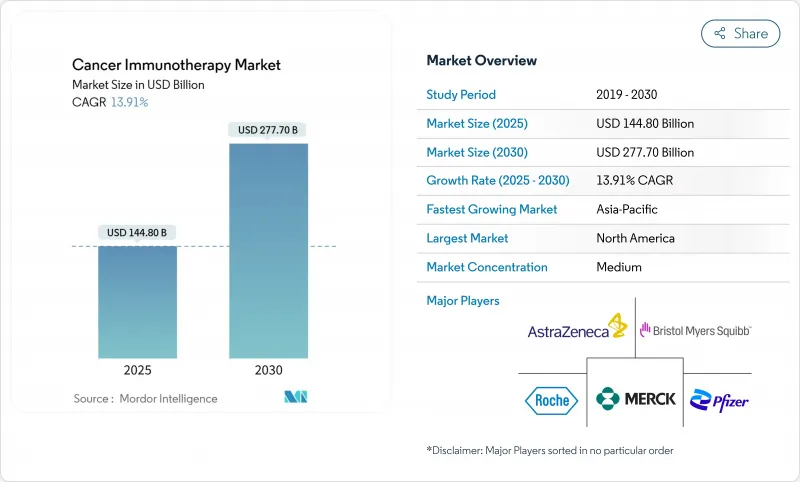

Cancer Immunotherapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The cancer immunotherapy market stood at USD 144.80 billion in 2025 and is forecast to reach USD 277.70 billion by 2030, advancing at a 13.91% CAGR.

The growth surge mirrors the therapy class' graduation from experimental use to a pillar of standard oncology care, accelerated by high-profile approvals such as the February 2024 U.S. Food and Drug Administration (FDA) clearance of lifileucel, the first tumour-infiltrating lymphocyte (TIL) therapy for advanced melanoma. Momentum is reinforced by large-scale manufacturing investments, widening payer acceptance of outcome-based contracts, and combination-therapy trial readouts that validate durable survival benefits. Supply-chain maturity around viral vectors and mRNA synthesis further lowers production risk, encouraging broader commercial roll-outs. Asia-Pacific's regulatory harmonisation and capacity build-out add a second growth engine that balances North America's established dominance, while competitive intensity heightens as cash-rich incumbents acquire specialised innovators to secure next-generation modalities.

Global Cancer Immunotherapy Market Trends and Insights

Escalating Global Incidence of Solid Tumours

Rising lifestyle-related risk factors and ageing demographics enlarge the treatable patient pool, notably in lung, colorectal, and breast cancers. Oncology societies now recommend routine biomarker screening, ensuring more patients are triaged early into immunotherapy regimens. Public-sector cancer awareness campaigns further accelerate diagnosis rates, while payer agencies expand reimbursement budgets for precision drugs that promise superior outcomes. Collectively, these forces sustain volume growth in the cancer immunotherapy market even as pricing pressures mount.

Superior Long-Term Survival Versus Chemotherapy

Five-year follow-up from CheckMate 9LA confirmed that nivolumab plus ipilimumab with chemotherapy achieved 18% overall survival in metastatic non-small cell lung cancer against 11% for chemotherapy alone, reinforcing the durability advantage that shapes modern treatment algorithms. Oncology guidelines increasingly prioritise checkpoint inhibitors in first-line settings for PD-L1-high tumours, driving protocol revisions at major cancer centres. Real-world registries corroborate trial data, boosting clinician confidence and catalysing hospital formulary expansion.

Therapy List Prices Above USD 300,000 and Reimbursement Caps

CAR-T therapies price above USD 300,000 per course, stretching payer budgets and prompting the rise of outcome-based contracts in markets such as the United States. Iovance's Amtagvi lists at USD 515,000, triggering negotiations that link payment to patient response. Tiered pricing and compulsory-licensing threats in emerging economies weigh on revenue trajectories, pressing manufacturers to streamline production for cost efficiencies.

Other drivers and restraints analyzed in the detailed report include:

- Expanding FDA/EMA Label Approvals for PD-1/PD-L1 Inhibitors

- Rapid Pipeline of CAR-T & Bispecific Antibodies

- Immune-Related Adverse Events (irAEs) Requiring Intensive Management

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Monoclonal antibodies retained 67.55% of revenue in 2024, giving them the largest cancer immunotherapy market share among modalities. Continued first-line use in lung, melanoma, and renal cancers supports sizable volumes, and the segment's cancer immunotherapy market size is projected to reach USD 174.2 billion by 2030. In contrast, oncolytic viruses are growing fastest at a 24.25% CAGR, underpinned by rising late-phase assets and manufacturing partnerships that unlock scale.

Investment patterns confirm strategic re-weighting; Pfizer's equity stake in Ignite Immunotherapy provides access to proprietary viral backbones aligned with mRNA payloads. Parallelly, Bristol Myers Squibb's alliance with BioNTech on bispecific antibodies merges antibody engineering know-how with mRNA capabilities. Convergence of modalities fosters combo regimens that enhance tumour-specific immunity and mitigate resistance.

Lung cancer contributed 25.53% of 2024 sales, representing the single largest indication within the cancer immunotherapy market. The segment's dominance persists as regulators approve adjuvant uses and high-burden geographies roll out screening programmes that drive earlier diagnosis. Hematologic malignancies exhibit the most rapid 22.15% CAGR, elevating their cancer immunotherapy market size to USD 68.6 billion by 2030.

CAR-T approvals for multiple myeloma and acute lymphoblastic leukaemia expand addressable patient pools, while bispecific antibodies extend therapy to those ineligible for cell therapy. Data from China show over 400 investigator-led CAR-T trials, reflecting academic enthusiasm and government support for indigenous innovation. Such activity positions hematology as a pivotal revenue accelerator over the forecast horizon.

The Cancer Immunotherapy Market Report is Segmented by Therapy Type (Monoclonal Antibodies, Immunomodulators, and More), Cancer Type (Prostate Cancer, Breast Cancer, Lung Cancer, and More), End Users (Hospitals and Clinics, Cancer Research Centers, and More), Route of Administration (Intravenous and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America preserved leadership with 48.72% of global revenue in 2024. The United States benefits from rapid FDA approvals, robust venture capital inflows, and payers experimenting with outcome-based reimbursement that sustains premium pricing. National Cancer Institute funding underwrites translational research across 71 designated cancer centres, maintaining a pipeline of investigator-initiated trials and novel combination studies. Canada mirrors the trend through federal investments in cell-therapy centres of excellence, accelerating domestic manufacturing capability.

Asia-Pacific delivers the fastest 18.22% CAGR through 2030. China spearheads regional momentum, hosting more than 400 CAR-T clinical programmes and building viral-vector capacity via public-private joint ventures. Regulatory reforms, such as the National Medical Products Administration's priority-review pathway, compress approval timelines to under 12 months for breakthrough therapies. Japan extends leadership in early adoption; the Pharmaceuticals and Medical Devices Agency approved nivolumab for malignant pleural mesothelioma ahead of other major markets, signalling regulatory agility. India focuses on indigenous CAR-T manufacturing, leveraging cost-efficient processes to widen access and capture export demand in emerging neighbouring nations.

Europe maintains steady expansion underpinned by EMA-level coordination. Pan-EU clinical-trial networks enable efficient patient recruitment across diverse genetic backgrounds, enriching data for precision biomarker validation. While Brexit imposes dual regulatory submissions, parallel scientific advice mitigates delays, sustaining UK participation in pivotal studies. Health Technology Assessment bodies across Germany, France, and the Nordics apply cost-effectiveness thresholds that pressure list prices, incentivising outcome-based discount frameworks. Local biomanufacturing clusters in Switzerland and Ireland scale supply for both domestic and export markets, reinforcing Europe's status as an advanced-therapy manufacturing hub.

- Amgen

- AstraZeneca

- Bristol-Myers Squibb

- Merck

- Roche

- Pfizer

- Novartis

- GlaxoSmithKline

- Eli Lilly and Company

- Abbvie

- Johnson & Johnson

- Regeneron Pharmaceuticals

- Sanofi

- BeiGene

- Seagen

- BioNTech

- Moderna

- Iovance Biotherapeutics

- OSE Immunotherapeutics SA

- Innovent Biologics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Incidence of Solid Tumors

- 4.2.2 Superior Long-Term Survival Vs. Chemotherapy & Targeted Small-Molecule Agents

- 4.2.3 Expanding FDA/EMA Label Approvals For PD-1/PD-L1 Inhibitors

- 4.2.4 Rapid Pipeline of CAR-T & Bispecific Antibodies Entering Late-Phase Trials

- 4.2.5 AI-Optimised Neoantigen Prediction Shortening Personalised Vaccine Lead-Times

- 4.2.6 Hospital Adoption of In-House TIL Manufacturing Driven By Point-Of-Care Bioreactors

- 4.3 Market Restraints

- 4.3.1 Therapy List-Prices >USD 300k And Reimbursement Caps

- 4.3.2 Immune-Related Adverse Events Requiring Intensive Management

- 4.3.3 Emerging Biosimilar PD-1s Pressuring Global Price Corridors

- 4.3.4 Viral-Vector Supply Bottlenecks For Autologous Cell Therapies

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Therapy Type

- 5.1.1 Monoclonal Antibodies

- 5.1.2 Cancer Vaccines

- 5.1.3 Immunomodulators (Cytokines, Adjuvants)

- 5.1.4 Cell-based Therapies

- 5.1.5 Oncolytic Virus Therapies

- 5.1.6 Combination Regimens

- 5.2 By Cancer Type

- 5.2.1 Lung Cancer

- 5.2.2 Breast Cancer

- 5.2.3 Melanoma & Skin Cancers

- 5.2.4 Prostate Cancer

- 5.2.5 Hematologic Malignancies (Leukemia, Lymphoma, Myeloma)

- 5.2.6 Others (CRC, Gastric, Renal, etc.)

- 5.3 By End User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Academic & Cancer Research Centers

- 5.3.3 Ambulatory & Specialty Infusion Centres

- 5.4 By Route of Administration

- 5.4.1 Intravenous

- 5.4.2 Sub-cutaneous / Intratumoral

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Amgen Inc.

- 6.3.2 AstraZeneca PLC

- 6.3.3 Bristol-Myers Squibb Co.

- 6.3.4 Merck & Co., Inc.

- 6.3.5 F. Hoffmann-La Roche Ltd

- 6.3.6 Pfizer Inc.

- 6.3.7 Novartis AG

- 6.3.8 GSK plc

- 6.3.9 Eli Lilly and Company

- 6.3.10 AbbVie Inc.

- 6.3.11 Johnson & Johnson (Janssen)

- 6.3.12 Regeneron Pharmaceuticals

- 6.3.13 Sanofi

- 6.3.14 BeiGene Ltd

- 6.3.15 Seagen Inc.

- 6.3.16 BioNTech SE

- 6.3.17 Moderna, Inc.

- 6.3.18 Iovance Biotherapeutics

- 6.3.19 OSE Immunotherapeutics SA

- 6.3.20 Innovent Biologics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment