PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844603

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844603

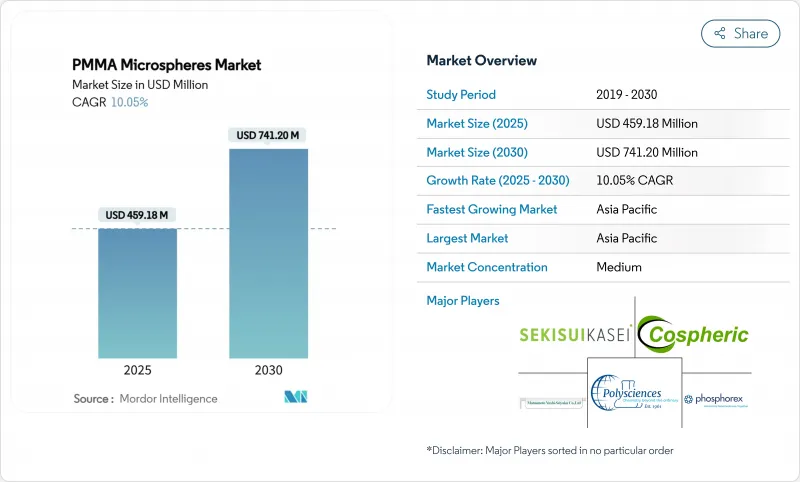

PMMA Microspheres - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The PMMA Microspheres Market size is estimated at USD 459.18 million in 2025, and is expected to reach USD 741.20 million by 2030, at a CAGR of 10.05% during the forecast period (2025-2030).

This strong trajectory reflects broadening adoption across aesthetic medicine, drug-delivery, advanced optics, and high-performance coatings. Growing demand for permanent dermal fillers, expansion of energy-efficient LED/LCD production, and the shift toward precision drug-delivery platforms are elevating volume and value growth. Producers are prioritizing monodisperse, surface-modified grades that command price premiums in life-science and electronics applications. Regulatory pressure on commodity microplastics is steering innovation toward sustainable or high-value niches rather than suppressing overall demand, while capacity optimization by large MMA suppliers is underpinning a tighter but more profitable supply environment.

Global PMMA Microspheres Market Trends and Insights

Growing Demand for PMMA Dermal Fillers in Minimally-Invasive Aesthetics

Bellafill, the only FDA-approved permanent injectable containing 20% PMMA microspheres, delivers wrinkle correction that persists for up to 15 years. A low 0.011% granuloma incidence reported across 4,725 gluteal-augmentation procedures underscores long-term safety. Microspheres in the 30-50 µm range resist phagocytosis yet foster collagen ingrowth, providing durable tissue support. Large-volume body-contouring usage is expanding the PMMA microspheres market by broadening the patient base beyond facial aesthetics. Clinics value reduced retreatment frequency, creating steady pull-through for medical-grade suppliers.

Expanding Use in Drug-Delivery & Embolization Therapies

PMMA microspheres offer lower nonspecific protein binding than polystyrene, improving biocompatibility in controlled-release systems. Surface carboxyl functionality enhances drug conjugation, while the density of 1.19 g/cc eases centrifugation handling. Continuous production of monodisperse porous particles with 50 nm pores now supports oncology drug-eluting beads. Commercial interest is rising as continuous manufacturing cuts costs and tightens batch consistency.

Regulatory Scrutiny Over Permanent Dermal-Filler Safety

Only one PMMA-based filler has FDA clearance, underscoring rigorous evidence requirements. Adverse events correlate with injection depth; submucosal placement increases nodule formation, prompting practitioner training mandates. Mandatory skin tests for bovine collagen carriers add cost. Emerging markets are tightening regulations, potentially lengthening approval timelines, and limiting broad uptake despite clinical durability advantages.

Other drivers and restraints analyzed in the detailed report include:

- Rising Utilisation in Personal-Care Formulations for Texture Enhancement

- Microfluidic Diagnostic Devices Requiring PMMA Calibration Beads

- MMA Monomer Price Volatility Impacting Production Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cosmetic Additive applications held 35.06% of PMMA microspheres market share in 2024, valued for imparting silky texture, soft-focus optics, and controlled release of actives. Premium skincare, color cosmetics, and suncare continue to specify medical-grade, low-residual MMA beads to satisfy safety audits. EU microplastic rules, however, are shifting large-volume mass-market lotions toward bio-based fillers, redirecting PMMA demand into leave-on serums and targeted anti-aging lines. Ceramic Porogen uses are accelerating at an 11.80% CAGR, as additive-manufactured alumina and zirconia components require sacrificial PMMA templates to engineer uniform pore networks critical for thermal-shock resistance. Light-diffusing agents in display films and matting additives in industrial coatings sustain mid-single-digit growth by delivering energy efficiency and low-gloss finishes, respectively. Modified Plastic Additive and Paints & Inks Additive segments absorb steady volumes where PMMA microspheres improve impact strength and rheology control.

The PMMA Microspheres Market Report is Segmented by Application (Light Diffusing Agent, Matting Agent, Cosmetic Additive, and More), End-User Industry (Lifesciences & Medical, Personal Care & Cosmetics, Electronics, and More), Particle Size (0-30 Mm, 30-100 Mm, Greater Than 100 Mm), and Geography (Asia-Pacific, North America, Europe, South America, Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led with 39.12% of PMMA microspheres market share in 2024. China's display-panel makers, Japanese fine-chemicals specialists, and South Korean consumer-electronics brands provide a robust demand backbone. Capacity consolidation, including Sumitomo Chemical's Singapore restructuring, nudges regional supply toward specialty grades yet maintains volume growth through 2030 at a 10.64% CAGR. Government incentives for semiconductor and medical-device supply chains further broaden downstream consumption.

North America benefits from stringent FDA standards, which favor domestic output of ISO-13485-compliant beads for injectable fillers and diagnostics. The Bellafill franchise anchors steady medical demand, while Wisconsin-based Nouryon has scaled specialty microsphere output for packaging and construction additives. R&D tax credits and venture capital funding in drug-delivery start-ups sustain innovation-driven consumption even as commodity volumes migrate offshore.

Europe faces the most restrictive polymer-micro-particle regulation, yet advanced-manufacturing bases in Germany and the Netherlands channel PMMA microspheres into high-margin coatings, automotive optics, and implantable medical devices. Producers are investing in bio-based or chemically recycled feedstocks that align with EU circular-economy goals, sustaining modest but profitable growth. South America and the Middle East & Africa remain emerging opportunity zones where growing healthcare infrastructure and infrastructure coatings uptake create incremental demand, though import dependence and regulatory variability temper rapid expansion.

- Bangs Laboratories, Inc.

- CD Bioparticles

- Cospheric LLC

- EPRUI Biotech Co.,Ltd.

- Goodfellow Cambridge Ltd.

- Heyo Enterprises Co., Ltd.

- Kayaku AM.

- Matsumoto Yushi-Seiyaku Co.,Ltd

- microParticles GmbH

- Phosphorex

- Polysciences

- Sekisui Kasei Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Sunjin Beauty Science

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for PMMA dermal fillers in minimally-invasive aesthetics

- 4.2.2 Expanding use in drug-delivery and embolization therapies

- 4.2.3 Adoption as light-diffusing and matting agents in LED/LCD, coatings

- 4.2.4 Rising utilisation in personal-care formulations for texture enhancement

- 4.2.5 Microfluidic diagnostic devices requiring PMMA calibration beads

- 4.3 Market Restraints

- 4.3.1 Regulatory scrutiny over permanent dermal-filler safety

- 4.3.2 MMA monomer price volatility impacting production costs

- 4.3.3 Limited global capacity for monodisperse high-precision grades

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Application

- 5.1.1 Light Diffusing Agent

- 5.1.2 Matting Agent

- 5.1.3 Cosmetic Additive

- 5.1.4 Ceramic Porogen

- 5.1.5 Modified Plastic Additive

- 5.1.6 Paints and Inks Additive

- 5.1.7 Other Applications

- 5.2 By End-user Industry

- 5.2.1 Lifesciences and Medical

- 5.2.2 Personal Care and Cosmetics

- 5.2.3 Electronics

- 5.2.4 Paints and Coatings

- 5.2.5 Plastics

- 5.2.6 Ceramics and Composites

- 5.2.7 Other End-user Industries

- 5.3 By Particle Size

- 5.3.1 0 - 30 µm

- 5.3.2 30 - 100 µm

- 5.3.3 Greater than 100 µm

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bangs Laboratories, Inc.

- 6.4.2 CD Bioparticles

- 6.4.3 Cospheric LLC

- 6.4.4 EPRUI Biotech Co.,Ltd.

- 6.4.5 Goodfellow Cambridge Ltd.

- 6.4.6 Heyo Enterprises Co., Ltd.

- 6.4.7 Kayaku AM.

- 6.4.8 Matsumoto Yushi-Seiyaku Co.,Ltd

- 6.4.9 microParticles GmbH

- 6.4.10 Phosphorex

- 6.4.11 Polysciences

- 6.4.12 Sekisui Kasei Co., Ltd.

- 6.4.13 Sumitomo Chemical Co., Ltd.

- 6.4.14 Sunjin Beauty Science

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment