PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844657

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844657

Europe Wheat Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

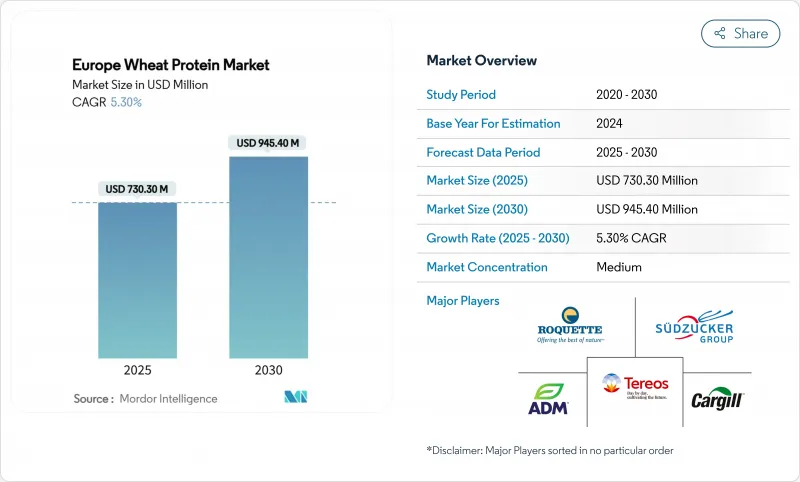

The Europe wheat protein market size is projected to grow substantially, increasing from USD 730.3 million in 2025 to USD 945.4 million by 2030, at a compound annual growth rate of 5.30%. In terms of market volume, the market is expected to grow from 184 thousand metric tons in 2025 to 237.70 thousand metric tons by 2030, at a CAGR of 5.25% during the forecast period (2025-2030).

This growth is driven by the rising popularity of plant-based diets, a growing preference for clean-label and sustainable food options, and supportive government policies aimed at fostering sustainable food systems. Germany, France, and the United Kingdom dominate the market due to their advanced food-processing capabilities and strong retail distribution networks. To meet the evolving consumer demand, manufacturers are enhancing their production processes by adopting advanced extraction and fractionation technologies. These innovations are expanding the use of wheat protein across various applications, including bakery products, meat substitutes, sports nutrition, and personal care items. Such developments are enabling manufacturers to align with consumer preferences while contributing to the region's sustainability objectives.

Europe Wheat Protein Market Trends and Insights

Growing usage of wheat protein in vegan and plant-based products

In Europe, manufacturers are increasingly adopting wheat protein for vegan and plant-based products, driving market growth. Leveraging wheat's versatility, they are creating meat substitutes that appeal to both vegans and flexitarians, with innovations like PLNT's wheat protein-based lamb strips and chicken-style sausages. Germany is supporting this shift with initiatives such as the EUR 38 million allocation by the Bundestag in November 2023 to promote sustainable protein sources, including plant-based foods and cultivated meat, while aiding farmers in their transition. Technological advancements by companies like Buhler and Andritz are scaling wheat protein production through methods like extrusion and fermentation, reducing costs and improving accessibility across food segments such as ready-to-eat meals, snacks, and bakery products. Rising consumer demand for sustainable, health-conscious options and Germany's focus on reducing greenhouse gas emissions further bolster the adoption of wheat protein, which offers nutritional and functional benefits with a lower environmental footprint compared to animal-based proteins.

Rising demand for clean-label ingredients

The clean label movement in Europe is transforming wheat protein formulations as consumers demand minimally processed and transparently sourced ingredients. Technological advancements, such as enzymatic hydrolysis, are enhancing the solubility and functionality of plant proteins like wheat protein without chemical additives, making them suitable for a wider range of food applications. Research published in the Proceedings of the National Academy of Sciences highlights the effectiveness of enzymatic hydrolysis in addressing the low solubility of certain plant proteins. Initiatives by Wageningen University and Research further support clean label solutions by promoting simplified ingredient lists and familiar components to boost consumer acceptance and trust. Additionally, EIT Food and Foundation Earth introduced environmental food scoring standards in August 2024, aiming to educate consumers about the ecological impact of their food choices while reinforcing sustainability and ethical sourcing practices in the food industry.

Surge in gluten intolerance and celiac disease cases

As celiac disease increasingly impacts Europe's populace, traditional wheat protein products grapple with challenges. Data from Ministero della Salute reveals that in 2023, 0.45% of Italians were affected by celiac disease. Regions like Aosta Valley, the Autonomous Province of Trento, and Tuscany reported higher prevalence rates . However, this rising health concern simultaneously carves out niche opportunities for specialized wheat protein variants. Responding to these health issues, the EU has rolled out stringent gluten labeling regulations. In contrast to the US's more lenient and often voluntary standards, the EU enforces strict compliance. Underlining this commitment, the European Commission's Regulation (EU) No 828/2014 mandates that products labeled "gluten-free" must not exceed 20 parts per million (ppm) of gluten. This regulation seeks to bolster clarity and safety for gluten-sensitive consumers. Reflecting these shifts, the market is seeing innovations such as gluten-free wheat flours that mimic traditional wheat products. These advancements not only tackle concerns about taste and nutrition but also specifically target those with gluten sensitivities. Consequently, while conventional wheat protein remains a staple for the mainstream, the market is evolving: specialized and modified wheat proteins are emerging to cater to consumers with dietary restrictions.

Other drivers and restraints analyzed in the detailed report include:

- Increasing use in bakery and confectionery application

- Fitness trends increase demand for wheat protein in supplements

- Rising use of substitute protein sources

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, wheat protein isolates command a dominant 43.67% share of the European market, owing to their high protein content and functional advantages in premium applications. According to the American Society of Baking, wheat protein isolate (WPI), boasting a minimum of 90% protein content, undergoes a wet-processing method. This process separates starch from wheat flour while retaining the desired protein properties. As a result, this high-protein ingredient finds its way into a myriad of products, from keto and low-calorie baked goods to baby food. Its ability to bolster dough strength and elasticity proves vital for high-speed baking. While the EU has yet to establish specific regulations for WPI composition, barring baby foods, this ambiguity fosters an innovative landscape, albeit with fundamental safety standards in place.

Hydrolyzed wheat protein is on the rise, projected to grow at a CAGR of 7.47% from 2025 to 2030. Its appeal lies in its superior digestibility and bioavailability, making it a sought-after ingredient in specialized nutrition and cosmetics. The European Food Safety Authority (EFSA) is on the frontlines, scrutinizing novel foods and ingredients, including protein hydrolysates, to ensure they align with safety standards before hitting the market. This segment's growth is bolstered by cutting-edge research in protein extraction and modification, amplifying the functional attributes and application scope of hydrolyzed wheat proteins in food, cosmetics, and pharmaceuticals.

In 2024, dry wheat protein dominates the market with an 83.33% share, due to its longer shelf life and logistical benefits in Europe's varied food manufacturing scene. For the 2023/2024 marketing year, the European Union's cereals market, a key supplier for wheat protein production, reported a soft wheat output of 125.5 million tonnes, as noted by the European Commission . This steady supply chain bolsters the leading position of dry wheat protein. Its handling and storage are less specialized than its liquid counterpart, making it the go-to choice for manufacturers across diverse application segments.

Liquid wheat protein is on a growth trajectory, boasting a CAGR of 5.97% from 2025 to 2030. Food and beverage manufacturers are gravitating towards these solutions, aiming to streamline production and ensure product consistency. The European Parliamentary Research Service underscores the role of alternative protein sources, including plant proteins, in bolstering food security and mitigating environmental impacts within the EU. This emphasis on sustainable protein is fueling innovations in liquid wheat protein formulations, especially in applications where swift incorporation and even distribution are paramount for quality and efficiency.

The Europe Wheat Protein Market Report Segments the Industry by Product Type (Isolate, Concentrate, and Hydrolyzed), Form (Dry and Liquid), Nature (Organic and Conventional), Application (Food and Beverage, Animal Feed, and Cosmetics and Personal Care), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- The Archer-Daniels-Midland Company

- Cargill, Incorporated

- Roquette Freres

- Tereos SCA

- MGP Ingredients, Inc.

- Crespel & Deiters Group

- First Dutch (Royal Ingredients Group)

- Sedamyl S.P.A.

- Sudzucker AG

- Kroner-Starke GmbH

- Bryan W Nash & Sons Ltd.

- Permolex Ltd.

- Kerry Group plc

- AGRANA Beteiligungs-AG

- Lantmannen Group

- Manildra Group

- Nexira SAS

- EURODUNA International GmbH

- The Jackering Group

- Meelunie B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing usage of wheat protein in vegan and plant-based products

- 4.2.2 Rising demand for clean-label ingredients

- 4.2.3 Increasing use in bakery and confectionery application

- 4.2.4 Fitness trends increase demand for wheat protein in supplements

- 4.2.5 Disruptions in animal protein supply boost wheat protein demand.

- 4.2.6 Research enhances wheat protein extraction and functionality

- 4.3 Market Restraints

- 4.3.1 Surge in gluten intolerance and celiac disease cases

- 4.3.2 Rising use of substitute protein sources

- 4.3.3 Fluctuation in raw material prices

- 4.3.4 Trade tariffs affecting wheat imports and exports

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Isolate

- 5.1.2 Concentrate

- 5.1.3 Hydrolyzed

- 5.2 By Form

- 5.2.1 Dry

- 5.2.2 Liquid

- 5.3 By Nature

- 5.3.1 Organic

- 5.3.2 Conventional

- 5.4 By Application

- 5.4.1 Food and Beverage

- 5.4.1.1 Bakery and Confectionery

- 5.4.1.2 Snacks and Cereals

- 5.4.1.3 Meat/Poultry/Seafood and Meat Alternatives

- 5.4.1.4 RTE/RTC Food Products

- 5.4.1.5 Other Application

- 5.4.2 Animal Feed

- 5.4.3 Cosmetics and Personal Care

- 5.4.1 Food and Beverage

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Russia

- 5.5.7 Netherlands

- 5.5.8 Poland

- 5.5.9 Nordics (Sweden, Denmark, Finland, Norway)

- 5.5.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 The Archer-Daniels-Midland Company

- 6.4.2 Cargill, Incorporated

- 6.4.3 Roquette Freres

- 6.4.4 Tereos SCA

- 6.4.5 MGP Ingredients, Inc.

- 6.4.6 Crespel & Deiters Group

- 6.4.7 First Dutch (Royal Ingredients Group)

- 6.4.8 Sedamyl S.P.A.

- 6.4.9 Sudzucker AG

- 6.4.10 Kroner-Starke GmbH

- 6.4.11 Bryan W Nash & Sons Ltd.

- 6.4.12 Permolex Ltd.

- 6.4.13 Kerry Group plc

- 6.4.14 AGRANA Beteiligungs-AG

- 6.4.15 Lantmannen Group

- 6.4.16 Manildra Group

- 6.4.17 Nexira SAS

- 6.4.18 EURODUNA International GmbH

- 6.4.19 The Jackering Group

- 6.4.20 Meelunie B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK