PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846210

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846210

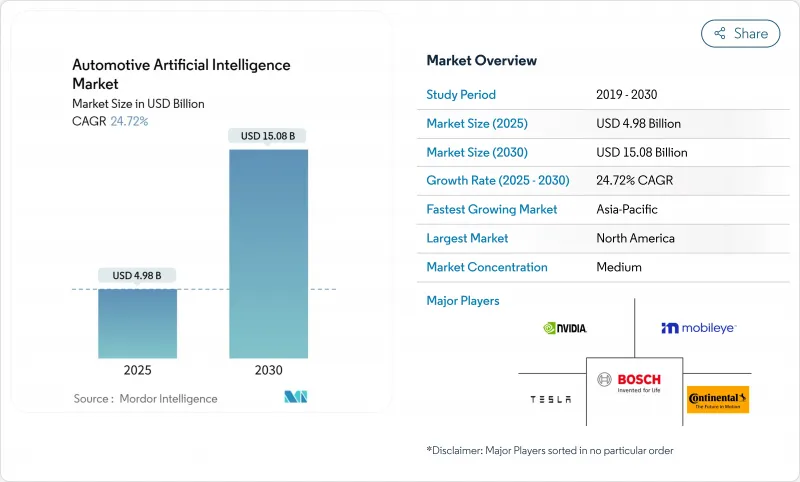

Automotive Artificial Intelligence - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Automotive AI market is valued at USD 4.98 billion in 2025 and is forecast to reach USD 15.08 billion by 2030, advancing at a 24.72% CAGR during the forecast period (2025-2030).

Rapid software-defined vehicle adoption, mandatory Level-2 ADAS regulations in the EU and the United States, and falling costs of automotive-grade AI compute are shifting competitive advantage from mechanical engineering to algorithm performance. Automakers are scaling over-the-air (OTA) update platforms that turn every delivered vehicle into a revenue-generating edge node, while chiplet-based system-on-chips (SoCs) make high TOPS performance affordable for mid-range models. Fleet-learning frameworks pioneered by Tesla and replicated by leading Chinese OEMs raise perception accuracy at a pace no closed-loop validation can match. Against this backdrop, strategic partnerships between carmakers, Tier-1s, hyperscalers, and AI start-ups are replacing vertical integration, creating a modular innovation ecosystem that encourages specialist differentiation.

Global Automotive Artificial Intelligence Market Trends and Insights

Regulatory Mandates For Level-2+ ADAS Safety Features

The EU General Safety Regulation II, which came into force in July 2024, obliges every new car sold in Europe to include automatic emergency braking, emergency lane-keeping, and intelligent speed assistance. Comparable requirements are gaining traction in the United States and Japan, nudging global automakers to design once and certify everywhere. Compliance needs have therefore transformed what used to be premium add-ons into baseline design elements, stimulating larger order volumes for perception stacks from Tier-1 suppliers. The United Nations ECE Regulation 171 on Driver Control Assistance Systems reinforces this shift by detailing virtual-testing rules for AI functions. As a result, OEMs that once differentiated through mechanical refinement now compete on software maturity timelines, and market entry barriers for newcomers fall when a clear rulebook replaces fragmented local requirements.

Rapid Decline In AI Compute And TOPS For Automotive SoCs

NVIDIA's Thor processor promises 2,000 TOPS, and Tesla's forthcoming AI5 chip targets 2,500 TOPS-ten times today's in-car performance while cutting cost per TOPS by roughly 40% every year since 2022. Cost deflation comes from shared data-center volumes, advanced foundry nodes, and chiplet partitioning that substitutes reticle-size monoliths with modular tiles. Imec's Automotive Chiplet Programme unites Bosch, BMW, and other pioneers around interoperable die-to-die protocols that compress development cycles and enable platform reuse across vehicle lines. As silicon ceases to be scarce, differentiation migrates to software, forcing traditional semiconductor suppliers to embed toolchains, middleware, and reference stacks that help automakers deploy at scale.

Fragmented Functional-Safety Regulations Across Jurisdictions

ISO 26262, ISO/IEC 5469:2024, and forthcoming ISO/TS 5083:2025 each define safety processes for different slices of the autonomy stack, leaving OEMs to reconcile overlaps and contradictions. Europe's GSR II departs from emerging US federal guidelines and China's GB/T standards, forcing global platforms to maintain separate compliance evidence for each region. Smaller suppliers struggle with the overhead of multi-track validation, often delaying launches or narrowing geographic scope. Industry consortia advocate a "safety case exchange" where audit artefacts could be ported between homologation authorities, but consensus remains distant. Until unification arrives, the patchwork saps the Automotive AI market growth by raising non-recurring engineering costs.

Other drivers and restraints analyzed in the detailed report include:

- Explosion of Over-the-Air SW Updates Enabling AI Feature Monetisation

- Fleet-Learning Architectures Accelerating Perception Model Accuracy

- High Validation Cost Of AI Models For Edge-Case Scenarios

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software generated 65.23% of the automotive artificial intelligence market revenue in 2024 as vehicle value creation migrated from iron and steel to lines of code. Automakers now ship neural-network upgrades that add features years after purchase, turning every connected car into a living, billed service node. Hardware segment grows at a CAGR of 14.23% during the forecast period, yet its margin compresses when chiplet ecosystems commoditise TOPS. The Automotive AI market, therefore, rewards companies able to bundle code, toolchains, and life-cycle support rather than those selling silicon alone.

Edge-resident language models like Cerence CaLLM Edge illustrate how software can boost perceived intelligence without network fees, meeting privacy guidelines in Europe and China. Regulatory mandates that require continuous improvement of braking or lane-keeping further lock in software revenues, because compliance updates must reach every in-use unit, not just fresh builds. As a result, the Automotive AI market sees Tier-1s investing billions in DevOps talent and OTA cybersecurity, cementing software as the primary moat.

Machine learning owns 41.56% of the automotive artificial intelligence market share in 2024 because its transparent decision trees satisfy ISO 26262 audit needs. Still, deep learning's 16.25% CAGR indicates manufacturers' migration toward multi-sensor fusion that classic algorithms cannot parse. Computer vision, natural language processing, and context awareness tie into cockpit user experience, widening the Automotive AI market beyond safety alone.

Tesla's planned AI5 chip demonstrates that only deep convolutional models can manage 4D radar, LiDAR, and HD-camera fusion at freeway speed. Chinese suppliers follow by embedding transformer networks inside parking-assist modules, making once-exotic AI a showroom differentiator. Consequently, supply-chain partners race to supply annotated data, scalable training infrastructure, and verification tools that handle opaque neural latent spaces.

The Automotive Artificial Intelligence Market is Segmented by Offering (Hardware and Software), Technology (Machine Learning, Deep Learning, and More), Process (Data Mining, Image Recognition, and More), Application (Autonomous Driving, and More), Vehicle Type (Passenger Cars, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 36.25% of the automotive artificial intelligence market in 2024 revenue, anchored by Tesla's data advantage, Texas's permissive testing statutes, and a domestic AI-compute cluster around NVIDIA's Silicon Valley headquarters. In the meantime, General Motors, Ford, and Waymo are scaling driverless operations from Phoenix to Austin, validating monetisation and spotlighting gaps in fleet-wide remote assistance regulation.

Asia-Pacific records a 23.43% CAGR, the fastest worldwide. China combines export-oriented EV leadership with a comparatively unified regulatory sandbox, letting Chery pledge AI rollout across 30 models and Huawei target 500,000 autonomous-capable vehicles by 2025. Japan's Toyota, Nissan, and Honda have formed a semiconductor consortium to address domestic AI shortages. In contrast, South Korea's Hyundai invests KRW 7 trillion in self-driving logistics corridors linking factory zones with ports. Local battery and lidar suppliers reduce the bill of materials for regional OEMs, boosting the Automotive AI market adoption in mid-segment vehicles.

Europe maintains strict data-privacy rules yet mandates AI safety functions under GSR II, creating a compliance-driven baseline for every volume platform. BMW's 2025 integration of DeepSeek AI in China underscores its localisation strategy, while Volkswagen rolls out Cerence Chat Pro OTA to millions of European vehicles. GDPR constraints amplify demand for edge inference, spurring suppliers to design privacy-preserving model-update pipelines. Although the market trails Asia in absolute growth, high per-vehicle content keeps Europe profitable for specialist vendors focusing on driver-monitoring and cyber-secure OTA stacks.

- Tesla Inc.

- Waymo LLC (Alphabet)

- NVIDIA Corporation

- Intel Corporation / Mobileye

- Horizon Robotics Inc.

- Aptiv PLC

- Continental AG

- Robert Bosch GmbH

- Qualcomm Incorporated

- Huawei Technologies Co.

- Microsoft Corporation

- Amazon Web Services Inc.

- Mercedes-Benz Group AG

- ZF Friedrichshafen AG

- BMW AG

- Toyota Motor Corporation

- Uber Technologies Inc.

- Hyundai Motor Company

- Hyundai Mobis Co. Ltd.

- Magna International Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory Mandates for Level-2+ ADAS Safety Features

- 4.2.2 Rapid Decline in AI-compute and TOPS for Automotive SoCs

- 4.2.3 Explosion of Over-the-air (OTA) SW Updates Enabling AI Feature Monetization

- 4.2.4 Fleet-learning Architectures Accelerating Perception Model Accuracy

- 4.2.5 On-device Multimodal Foundation Models Reducing Cloud Dependency

- 4.2.6 Emerging Chiplet-Based ECUs Lowering BOM for Mass-market Vehicles

- 4.3 Market Restraints

- 4.3.1 Fragmented Functional-Safety Regulations Across Jurisdictions

- 4.3.2 High Validation Cost of AI Models for Edge-case Scenarios

- 4.3.3 Persistent Scarcity of Automotive-grade AI Talent in Tier-1s

- 4.3.4 Supply-chain Exposure to Advanced-node Foundry Capacity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.2 Software

- 5.2 By Technology

- 5.2.1 Machine Learning

- 5.2.2 Deep Learning

- 5.2.3 Computer Vision

- 5.2.4 Natural Language Processing

- 5.2.5 Context Awareness

- 5.3 By Process

- 5.3.1 Data Mining

- 5.3.2 Image Recognition

- 5.3.3 Signal Recognition

- 5.4 By Application

- 5.4.1 Autonomous Driving

- 5.4.2 Advanced Driver-Assistance Systems (ADAS)

- 5.4.3 Human-Machine Interface

- 5.4.4 Predictive Maintenance & Diagnostics

- 5.5 By Vehicle Type

- 5.5.1 Passenger Cars

- 5.5.2 Light Commercial Vehicles

- 5.5.3 Heavy Commercial Vehicles

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Indonesia

- 5.6.4.6 Philippines

- 5.6.4.7 Vietnam

- 5.6.4.8 Australia

- 5.6.4.9 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Nigeria

- 5.6.5.6 Egypt

- 5.6.5.7 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Tesla Inc.

- 6.4.2 Waymo LLC (Alphabet)

- 6.4.3 NVIDIA Corporation

- 6.4.4 Intel Corporation / Mobileye

- 6.4.5 Horizon Robotics Inc.

- 6.4.6 Aptiv PLC

- 6.4.7 Continental AG

- 6.4.8 Robert Bosch GmbH

- 6.4.9 Qualcomm Incorporated

- 6.4.10 Huawei Technologies Co.

- 6.4.11 Microsoft Corporation

- 6.4.12 Amazon Web Services Inc.

- 6.4.13 Mercedes-Benz Group AG

- 6.4.14 ZF Friedrichshafen AG

- 6.4.15 BMW AG

- 6.4.16 Toyota Motor Corporation

- 6.4.17 Uber Technologies Inc.

- 6.4.18 Hyundai Motor Company

- 6.4.19 Hyundai Mobis Co. Ltd.

- 6.4.20 Magna International Inc.

7 Market Opportunities & Future Outlook