PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846298

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846298

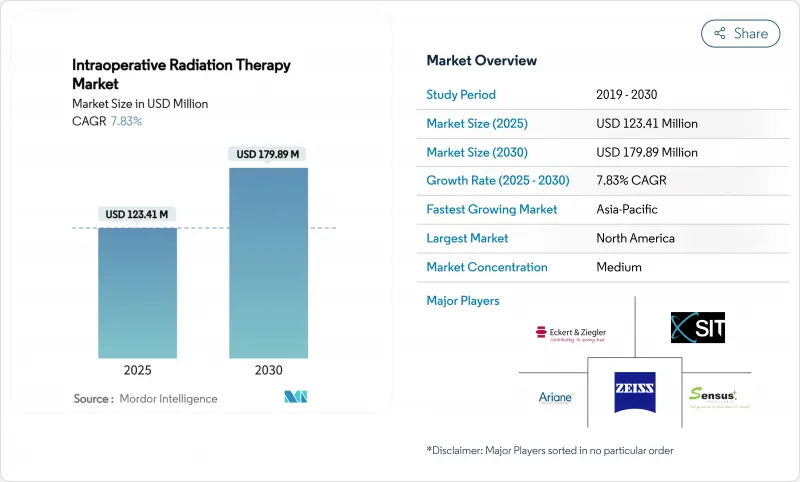

Intraoperative Radiation Therapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The intraoperative radiation therapy market size stood at USD 123.41 million in 2025 and is forecast to reach USD 179.89 million by 2030, advancing at a 7.83% CAGR.

The growth reflects hospital demand for single-session radiation options that free linear-accelerator capacity, shorten care pathways and align with bundled-payment incentives. Miniaturised mobile electron accelerators now slot into standard operating rooms, eliminating costly bunker retro-fits and expanding addressable sites of service. Early evidence of equivalent local-control rates in breast cancer, combined with improving image-guided accuracy for neurosurgical and gastro-intestinal procedures, sustains clinical confidence. Vendor consolidation around full-stack oncology platforms, coupled with service-oriented revenue models, enhances implementation support and reduces ownership risk for mid-size providers.

Global Intraoperative Radiation Therapy Market Trends and Insights

Growing Global Prevalence of Cancer

Cancer incidence is projected to hit 24 million new cases by 2030, overwhelming capacity at many external-beam facilities . Emerging economies such as India illustrate the gap: 521 radiotherapy centers serve more than 1.3 million annual cases, leading to treatment delays. IORT compresses multi-week regimens into a single procedure, freeing slots for complex fractionated cases and improving throughput. Health ministries in high-density nations increasingly view portable electron units as stop-gap infrastructure that multiplies surgical suites' utility. The trend also aligns with demographic ageing in OECD economies, where comorbidity burdens make prolonged courses impractical.

Advancements in Cancer-Therapy Technologies

Integration of surgical robotics with radiation delivery now enables margin-controlled dosing within minutes; Varian's HyperSight imaging cuts acquisition time by 50% and enhances lesion visualization . FLASH protocols delivering >40 Gy/s show promise for limiting normal-tissue toxicity, with trial treatment times of 4-9 minutes . Artificial-intelligence models achieve 84% accuracy in predicting positive margins during breast-conserving surgery, reducing re-excision risk. Miniaturised accelerators, lighter shielding, and battery operation broaden adoption in low-resource settings. Together, these advances reduce specialized training needs and shrink total procedural duration, attracting multidisciplinary teams.

Shortage of Trained Multidisciplinary IORT Teams

Radiation therapist vacancy rates reached 10.7% in 2022, and medical dosimetrist deficits are projected to persist through 2035. IORT demands real-time collaboration among surgeons, physicists, and therapists, a combination scarce outside tertiary centers. Accreditation bodies eliminated on-the-job pathways in 2017, forcing candidates into scarce baccalaureate programs that seldom offer hands-on intraoperative exposure. Smaller hospitals struggle to justify dedicated teams amid low case volumes, creating regional access gaps. Workforce bottlenecks, therefore, temper expansion despite equipment availability.

Other drivers and restraints analyzed in the detailed report include:

- Advantages of IORT Over Prolonged External-Beam Courses

- Outpatient Bundled-Payment Models

- Clinical Preference for Conventional Fractionated Radiotherapy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electron approaches retained 59.91% share of the intraoperative radiation therapy market in 2024 on the back of decades-long breast-cancer validation and streamlined mobile-accelerator workflows. The modality sustains a reliable supply chain for applicators and quality-assurance tools that hospitals already stock. Intraoperative brachytherapy, however, is expected to post an 8.34% CAGR through 2030 as high-definition afterloaders and real-time dosimetry software improve conformity in irregular cavities. Photon-based and alpha-particle seed systems represent a nascent 3% niche, with FDA investigational exemptions driving early uptake in recurrent glioblastoma. Clinical teams now match method to tumor geography, fuelling diversified purchasing patterns.

Electron advocates point to deeper penetration abilities that suit larger breast or pelvic fields, whereas brachytherapy proponents highlight dosimetric sparing near cranial nerves. Alpha DaRT's radium-224 seeds showed favorable safety in pilot cohorts, adding competitive pressure. Vendors co-marketing hybrid suites-where electron and brachytherapy carts share imaging infrastructure-further blur categorical lines. As surgical oncology subspecialises, decision criteria center on procedure time, shielding costs and credentialing familiarity rather than intrinsic physical dosimetry.

Capital sales delivered 67.21% of 2024 revenue, underpinned by repeat replacement cycles for accelerators and real-time imaging consoles. Hospitals in mature markets refresh fleets every 7-8 years to comply with evolving AI-integrated planning software, sustaining double-digit unit price growth. Yet service lines are on an 8.45% CAGR trajectory, reflecting provider appetite for turnkey packages that bundle physics support, remote QA and staff certification. The intraoperative radiation therapy industry has shifted toward outcome-based service contracts, where vendors assume uptime guarantees and share clinical-quality metrics.

System-level integration platforms like Varian ARIA CORE overlay data from pathology, imaging and dosimetry, reducing siloed workflows. Subscription models for software-as-a-service and predictive maintenance analytics now contribute 22% of recurring sales, smoothing vendor revenue volatility. Accessory categories-sterile carts, shielded drapes, docking stations-offer high-margin consumables that lock customers into proprietary ecosystems. While unit installations drive visibility, service competence increasingly determines tender awards, especially in resource-constrained regions where staffing depth is limited.

The Intraoperative Radiation Therapy Report is Segmented by Method (Electron IORT, Intraoperative Brachytherapy, Other Methods), Products and Services (Products and Services), Application (Breast Cancer, Brain Tumor, and More), End User (Hospitals, Specialty Clinics, Others), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America preserved 42.45% intraoperative radiation therapy market share in 2024 as clear HCPCS codes and bundled-payment pilots de-risk capital investment. U.S. integrated delivery networks leverage economies of scale to negotiate multiyear service contracts, while Canadian provinces include IORT in provincial cancer agency roadmaps. Provider networks in suburban settings report utilisation rates exceeding 85% because mobile units rotate among campuses overnight, extending return on assets. Eleven states now reimburse single-dose breast boosts at parity with hypofractionated external-beam regimens, accelerating penetration.

Europe maintains steady adoption on the back of cross-border device certification, though heterogenous DRG payments create variability. German and Italian breast-surgeon societies publish consensus guidelines that frame IORT as standard of care for selected patients, underpinning reimbursement. UK National Health Service pilot studies document net savings of GBP 2,300 (USD 2,930) per case after currency conversion at 2024 average rates, largely from reduced transport services. Scandinavian countries show high per-capita utilisation due to dispersed populations and winter travel challenges. However, smaller Central-Eastern markets face capital budget caps that delay fleet renewal.

Asia-Pacific is projected to log an 8.88% CAGR to 2030, powered by China's national isotope roadmap and Japan's ageing demography. Government-subsidised procurement schemes fund province-level radiotherapy hubs where intraoperative suites serve satellite hospitals via weekly block scheduling. Taiwan hosts eight proton centers, creating regional expertise that cross-pollinates intraoperative adoption. India's Tata Memorial chain operates mobile electron units in rural outreach programs, cutting average patient travel distance by 53% compared with city-based linacs. Despite strong momentum, workforce shortages persist: the Philippines counts only 113 radiation oncologists for 110 million citizens, underscoring training imperatives.

South America and the Middle East & Africa remain emerging opportunities. Chile's public-private partnerships finance hybrid ORs, while Saudi Arabia earmarks oncology modernization funds in Vision 2030. Currency volatility and import tariffs hamper smaller economies, yet used-equipment markets and vendor-financed leases lower entry barriers. Clinical societies across the Gulf states translate European guidelines to local practice, smoothing regulatory pathways. Over the forecast, unmet need combined with demographic shifts positions both regions as long-term volume engines if workforce pipelines materialize.

- Siemens Healthineers (Varian Medical Systems)

- Elekta

- Carl Zeiss

- IntraOp Medical Corporation

- iCAD Inc.

- Ariane Medical Systems

- Eckert & Ziegler

- GMV Innovating Solutions

- Sensus Healthcare

- Sordina IORT Technologies

- IsoRay

- Accuray

- Ion Beam Applications S.A. (IBA)

- Brain Lab

- Zap Surgical Systems Inc.

- medPhoton GmbH

- Surgiceye GmbH

- ViewRay Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing global prevalence of cancer

- 4.2.2 Advancements in cancer-therapy technologies

- 4.2.3 Advantages of IORT over prolonged external-beam courses

- 4.2.4 Outpatient-bundled payment models incentivising single-dose IORT

- 4.2.5 Miniaturisation of mobile electron accelerators for low-resource ORs

- 4.2.6 AI-guided intra-op imaging improving margin assessment & uptake

- 4.3 Market Restraints

- 4.3.1 Shortage of trained multidisciplinary IORT teams

- 4.3.2 Clinical preference for conventional fractionated radiotherapy

- 4.3.3 Limited long-term outcome data beyond breast indications

- 4.3.4 High shielding / OR-retro-fit capex for mobile CT-compatible units

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Method

- 5.1.1 Electron IORT

- 5.1.2 Intraoperative Brachytherapy

- 5.1.3 Other Methods

- 5.2 By Products and Services

- 5.2.1 Products

- 5.2.1.1 Systems and Accelerators

- 5.2.1.2 Applicators & Afterloaders

- 5.2.1.3 Treatment Planning Systems

- 5.2.1.4 Accessories

- 5.2.2 Services

- 5.2.1 Products

- 5.3 By Application

- 5.3.1 Breast Cancer

- 5.3.2 Brain Tumor

- 5.3.3 Gastro-intestinal Cancer

- 5.3.4 Head and Neck Cancer

- 5.3.5 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Specilaty Clinics

- 5.4.3 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Siemens Healthineers (Varian Medical Systems)

- 6.3.2 Elekta AB

- 6.3.3 Carl Zeiss Meditec AG

- 6.3.4 IntraOp Medical Corporation

- 6.3.5 iCAD Inc.

- 6.3.6 Ariane Medical Systems Ltd

- 6.3.7 Eckert & Ziegler

- 6.3.8 GMV Innovating Solutions

- 6.3.9 Sensus Healthcare Inc.

- 6.3.10 Sordina IORT Technologies

- 6.3.11 Isoray Inc.

- 6.3.12 Accuray Incorporated

- 6.3.13 Ion Beam Applications S.A. (IBA)

- 6.3.14 Brainlab AG

- 6.3.15 Zap Surgical Systems Inc.

- 6.3.16 medPhoton GmbH

- 6.3.17 Surgiceye GmbH

- 6.3.18 ViewRay Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment