PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848295

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1848295

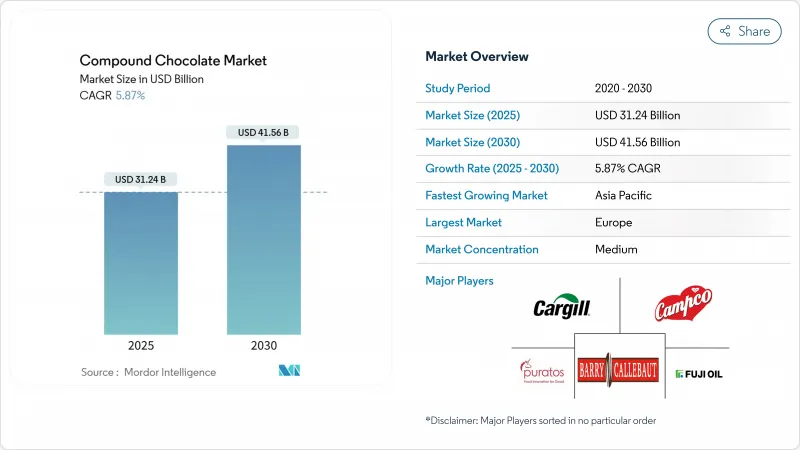

Compound Chocolate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The compound chocolate market size is anticipated to reach USD 31.24 billion by 2025 and is projected to grow at a CAGR of 5.87%, attaining USD 41.56 billion by 2030.

The rising cost of cocoa beans has significantly influenced manufacturers to adopt compound chocolate, which uses vegetable fats instead of cocoa butter, thereby mitigating cost pressures. Additionally, the extended shelf life and simplified processing of compound chocolate offer manufacturers operational advantages, such as reduced labor and energy costs during large-scale production. This cost-effectiveness, coupled with its versatility, has positioned compound chocolate as a preferred ingredient in bakery, confectionery, and ice cream applications. Food processors are further enhancing their appeal by introducing innovative flavors and inclusions, catering to the evolving preferences of consumers. Meanwhile, regulatory developments are reshaping the market dynamics. The European Union's Deforestation-Free Regulation, effective December 2025, is compelling global manufacturers to source certified fats and traceable cocoa equivalents. This move ensures compliance, maintains market access, and addresses sustainability concerns, all while managing associated costs effectively.

Global Compound Chocolate Market Trends and Insights

Cost effectiveness of compound chocolate as compared to real chocolates surges its demand

The growing adoption of compound chocolate reflects a strategic response to intensifying cost pressures across the chocolate industry, as manufacturers seek ways to protect margins without sacrificing product appeal. Compound chocolate's cost effectiveness, operational simplicity, and ability to bypass the tempering process make it an increasingly viable alternative to traditional chocolate, especially for large-scale commercial applications. In 2024, U.S. chocolate and cocoa product exports were valued at USD 2.36 billion, according to the U.S. Department of Agriculture, underscoring the persistent price pressures within the industry. The sharp and sustained rise in cocoa prices has widened the cost gap between real chocolate and compound chocolate, making the latter a more attractive option for manufacturers facing shrinking margins. Financial institutions expect elevated cocoa prices to persist in the medium term, reinforcing the urgency for structural adjustments like switching to compound chocolate, which enables manufacturers to manage input costs, safeguard profitability, and remain competitive in a volatile market landscape.

Strong demand from the bakery, confectionery, and ice cream industries boosts market growth.

The industrial applications of compound chocolate in the bakery, confectionery, and ice cream sectors are driving substantial volume growth, as manufacturers increasingly prioritize its functional benefits over cost advantages. Compound chocolate provides notable technical benefits, such as eliminating the need for tempering, offering stable melting properties, and ensuring compatibility with a wide range of ingredients. These attributes make it indispensable for large-scale production environments where efficiency and consistency are critical. The Institute of Food Technologists emphasizes the importance of applying scientific knowledge to enhance product quality and improve consumer satisfaction in the chocolate market. They note that compound chocolate formulations can be customized to meet specific industrial needs, addressing challenges such as ingredient integration and production scalability. In response to this growing demand, companies are innovating by developing specialized compound chocolate products tailored for diverse industrial applications. With production capacities reaching tens of thousands of tons annually, these companies are well-positioned to supply food manufacturers across multiple regions, supporting the evolving needs of the global food industry.

Health concerns over hydrogenated fats and additives used in some compound formulations.

Growing consumer awareness about the health risks associated with hydrogenated fats and artificial additives in compound chocolate is driving resistance in the market, particularly among health-conscious demographics. Regulatory developments further amplify these concerns. For example, the FDA enforces strict guidelines on chocolate production, specifying minimum cocoa content and restricting the use of certain additives. Similarly, the Singapore Food Agency has implemented a robust regulatory framework requiring safety assessments and permitting only specific additives, reflecting the increasing scrutiny on compound chocolate. These health-driven constraints significantly impact premium market segments, where consumers demand higher ingredient transparency and quality. Consequently, the market is experiencing a clear bifurcation: compound chocolate continues to expand its presence in value-oriented applications due to cost advantages, while its penetration in premium segments remains limited by concerns over its composition and regulatory compliance.

Other drivers and restraints analyzed in the detailed report include:

- Growth in private label and budget chocolate brands drives demand for compound chocolate.

- Innovations in flavors, textures, and inclusions broadens its consumer appeal.

- Regulatory scrutiny on artificial ingredients and labeling standards could hinder growth.

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, the milk compound chocolate segment commands a dominant 47.03% market share, largely due to its favored status in bakery and confectionery applications. Its leadership is anchored in a balanced flavor profile and versatility, making it the go-to for manufacturers, whether for enrobing or molding. This segment's robustness is further highlighted by its ingredient compatibility and consistent performance in automated settings. Cargill's technical insights reveal that vegetable fat-based compound chocolates eliminate the need for tempering, enhancing their appeal for enrobing and molding. The milk variant's widespread popularity is attributed to its universally appealing taste and the functional advantages it offers to industrial users.

The dark compound chocolate segment is on the rise, with projections indicating an 6.03% CAGR from 2025 to 2030, outpacing the overall market. This surge is largely fueled by heightened consumer awareness of dark chocolate's health benefits, notably its antioxidant properties and potential heart advantages. Additionally, the segment aligns with the growing consumer trend of "mindful indulgence," where the focus is on balancing enjoyment with nutritional value. Industry experts emphasize the significance of market trends and consumer insights in crafting new chocolate offerings, especially as health-conscious choices gain traction. Moreover, the dark compound chocolate segment is reaping rewards from flavor innovations and the addition of functional ingredients that bolster its health appeal.

The Compound Chocolate Market Report Segments the Industry Into by Type (Dark, Milk, White, and Others), Form (Chocolate Chips/Drops/Chunks, Chocolate Slabs and Blocks, Chocolate Coatings, and More), Distribution Channel (Retail, Industrial, and Foodservice), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Given in Terms of Value (USD).

Geography Analysis

In 2024, Europe commands the largest regional market share at 34.01%, capitalizing on its well-established chocolate manufacturing base and advanced retail networks. Europe's chocolate market thrives on a rich consumption tradition and is bolstered by major industry players pioneering innovations in compound chocolate. Sustainability is becoming a focal point in Europe, with initiatives like the EU's Deforestation-Free Regulation reshaping supply chains and imposing new compliance mandates on manufacturers. As European consumers increasingly prioritize sustainability in their purchasing choices, manufacturers are responding by crafting more transparent and eco-friendly compound chocolate formulations. While the market is mature, there's a vibrant push towards innovation, especially in premium and specialty segments.

Asia-Pacific is set to outpace others with a projected 7.93% CAGR from 2025 to 2030, fueled by urbanization, rising incomes, and the growth of modern retail. As lifestyles evolve and Western confectionery gains traction, new avenues for compound chocolate applications emerge. Major players are making strategic moves, establishing production units, and ramping up capacity to cater to local demands. Events like India's AAHAR fair, backed by government trade promotions, foster knowledge sharing and collaborations in food processing. Given the region's varied market dynamics, companies are customizing product development and distribution strategies to align with local tastes and regulations.

North America stands as a mature market, boasting a stronghold of leading chocolate manufacturers and a robust distribution network. The compound chocolate market here thrives on a vibrant foodservice sector and a surge in consumer interest in baking and home cooking. U.S. government data underscores the chocolate sector's significance, highlighting substantial export values for chocolate and cocoa products. With a regulatory focus on food safety and labeling clarity, North American manufacturers are held to high standards in both product development and marketing. Meanwhile, South America and the Middle East & Africa, though smaller in market share, are witnessing a surge in growth, spurred by a burgeoning middle class and modern retail developments enhancing product accessibility.

- Barry Callebaut Group

- Cargill Incorporated

- Fuji Oil Holdings Inc.

- Puratos Group

- The Central Arecanut and Cocoa Marketing and Processing Co-operative Limited (CAMPCO Chocolates)

- AAK AB

- Nestle S.A

- Clasen Quality Chocolate, Inc.

- FoodGrid Inc.

- 3F Industries LTD

- Bakels Group

- Sephra LP

- Morde

- Pure Temptation Pvt. Ltd.

- Choco Nutri

- Pellagic Food Ingredients Private Limited

- Mangharam Chocolate Solutions

- Gujarat Cooperative Milk Marketing Federation (GCMMF)

- Gandum Mas Kencana

- Polen GIda

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost effectiveness of compound chocolate as compared to real chocolates surges its demand

- 4.2.2 Strong demand from the bakery, confectionery, and ice cream industries boosts market growth.

- 4.2.3 Growth in private label and budget chocolate brands drives demand for compound chocolate.

- 4.2.4 Innovations in flavors, textures, and inclusions broadens its consumer appeal.

- 4.2.5 Increasing adoption of vegan and plant-based diets encourages non-dairy compound variants.

- 4.2.6 Longer shelf life than couverture chocolate makes it ideal for mass production and export.

- 4.3 Market Restraints

- 4.3.1 Health concerns over hydrogenated fats and additives used in some compound formulations.

- 4.3.2 Regulatory scrutiny on artificial ingredients and labeling standards could hinder growth.

- 4.3.3 Fluctuating prices of vegetable fats and cocoa substitutes can affect cost stability.

- 4.3.4 Intense competition from real chocolate products in developed markets limits expansion.

- 4.4 Regulatory Outlook

- 4.5 Technology Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Type

- 5.1.1 Dark

- 5.1.2 Milk

- 5.1.3 White

- 5.1.4 Others

- 5.2 By Form

- 5.2.1 Chips/Drops/Chunks

- 5.2.2 Slabs and Blocks

- 5.2.3 Coatings

- 5.2.4 Fillings & Spreads

- 5.2.5 Others

- 5.3 By Distribution Channel

- 5.3.1 Retail

- 5.3.1.1 Supermarkets/Hypermarkets

- 5.3.1.2 Convenience Stores

- 5.3.1.3 Online Retail Stores

- 5.3.1.4 Other Distribution Channels

- 5.3.2 Industrial

- 5.3.3 Foodservice

- 5.3.1 Retail

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Poland

- 5.4.2.8 Belgium

- 5.4.2.9 Sweden

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Indonesia

- 5.4.3.6 South Korea

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Chile

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Barry Callebaut Group

- 6.4.2 Cargill Incorporated

- 6.4.3 Fuji Oil Holdings Inc.

- 6.4.4 Puratos Group

- 6.4.5 The Central Arecanut and Cocoa Marketing and Processing Co-operative Limited (CAMPCO Chocolates)

- 6.4.6 AAK AB

- 6.4.7 Nestle S.A

- 6.4.8 Clasen Quality Chocolate, Inc.

- 6.4.9 FoodGrid Inc.

- 6.4.10 3F Industries LTD

- 6.4.11 Bakels Group

- 6.4.12 Sephra LP

- 6.4.13 Morde

- 6.4.14 Pure Temptation Pvt. Ltd.

- 6.4.15 Choco Nutri

- 6.4.16 Pellagic Food Ingredients Private Limited

- 6.4.17 Mangharam Chocolate Solutions

- 6.4.18 Gujarat Cooperative Milk Marketing Federation (GCMMF)

- 6.4.19 Gandum Mas Kencana

- 6.4.20 Polen GIda

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK