PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850153

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850153

Fluid Biopsy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

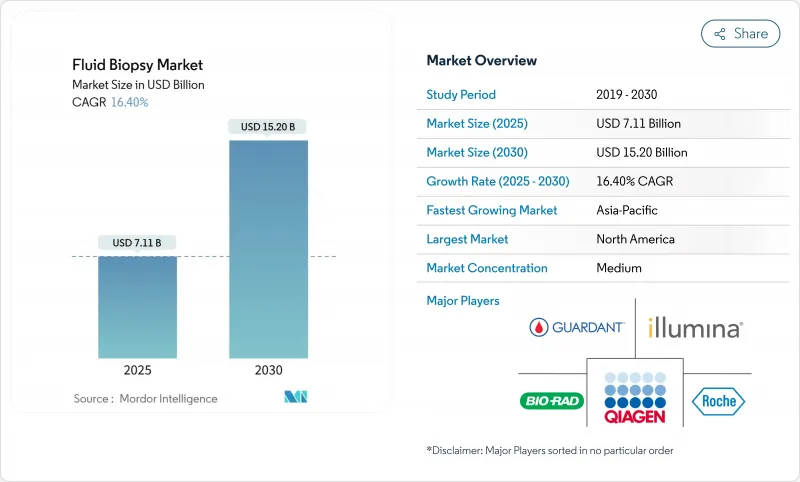

The fluid biopsy market size stands at USD 7.11 billion in 2025 and is forecast to advance to USD 15.20 billion by 2030, reflecting a 16.40% CAGR.

Rapid AI-guided signal-enrichment techniques, broader Medicare coverage, and multiple FDA breakthrough device designations position fluid biopsies as a routine component of precision oncology workflows. Machine-learning fragmentomics improves detection of circulating tumor DNA (ctDNA) in early-stage cancers, mitigating the low-yield barrier that once limited screening programs. Investment momentum remains strong: single funding rounds now exceed USD 105 million for platform developers that combine next-generation sequencing (NGS) with decentralized automation to shorten turnaround times. Competitive intensity is rising as emerging players deliver software-centric tools that challenge incumbents on sensitivity, price, and scalability. Asia-Pacific's regulatory agility and large at-risk population create outsized growth potential, while North America retains leadership through reimbursement certainty and research depth.

Global Fluid Biopsy Market Trends and Insights

Rising Preference for Non-Invasive Oncology Diagnostics

Patient demand for safer procedures has re-shaped cancer work-ups. Medicare's 2025 coverage of Guardant Health's Shield assay validates liquid biopsy utility for routine screening and extends access to Veterans Affairs beneficiaries. Elderly cohorts gain most because tissue biopsy complications rise sharply with comorbidities. Real-time blood-based monitoring allows oncologists to modify therapy sooner than imaging-based schedules, giving fluid biopsy market solutions a complementary role rather than a replacement one. Outpatient clinics adopt the tests quickly because sample collection requires only phlebotomy skills. The trend reinforces decentralized testing demand and underpins recurring reagent revenue.

AI-Driven Fragmentomics Boosting Early-Stage Detection Accuracy

Machine-learning models now interpret fragment length, end motif, and methylation patterns from cell-free DNA to identify early tumors with 92% sensitivity at 90% specificity in non-small cell lung cancer trials. Weill Cornell Medicine's MRD-EDGE protocol detects residual disease months before radiographic relapse, facilitating pre-emptive therapy switches. Johns Hopkins' ARTEMIS-DELFI platform provides real-time pancreatic cancer response metrics, addressing a malignancy that historically evaded surveillance. These advances make AI the core infrastructure for future fluid biopsy market platforms. Continuous algorithm training with global data sets will likely widen performance gaps between AI-native and conventional assays.

High Test Cost & Reimbursement Hurdles

Comprehensive liquid biopsy panels still average USD 2,800 per use, challenging adoption in systems with constrained oncology budgets. Health-economic models indicate prices must drop by two-thirds for second-line colorectal screening to reach cost-effectiveness thresholds. Payer review cycles remain lengthy, demanding robust clinical-utility evidence rather than analytical-validity data. Emerging markets face additional currency fluctuation risks that complicate budgeting for imported reagents. Until scalable manufacturing achieves double-digit cost reductions, uptake outside premium tertiary centers may remain modest.

Other drivers and restraints analyzed in the detailed report include:

- Sequencing-Cost Decline & NGS Workflow Automation

- Reimbursement Expansion for Minimal Residual-Disease Blood Tests

- Low ctDNA Yield in Early-Stage Tumors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, lung applications generated 33.55% of overall revenues, consolidating leadership through multiple FDA-cleared companion diagnostics that guide EGFR, ALK, and MET inhibitor therapy selections. The fluid biopsy market benefits from well-mapped mutation profiles and the clinical necessity of repeat testing at progression, which boosts reagent pull-through. Pancreatic programs, although starting smaller, post an impressive 18.25% forecast CAGR on the strength of AI-enabled response monitoring platforms that deliver actionable insight within days. Broad payer support for therapy-selection panels encourages hospitals to integrate liquid biopsy into baseline staging protocols.

Real-world data show breast and colorectal oncology teams now add blood-based surveillance between imaging cycles, cutting average radiology utilization by 15%. Prostate cancer indications gain traction after BRCA-positive metastatic castration-resistant approvals expanded testing beyond genomic labs to urology clinics. Ovarian and gastric trials progress steadily as multi-omics assays uncover epigenetic signatures absent in mutation-centric panels. Adoption diversity across tumor types helps cushion revenue cycles against single-indication reimbursement headwinds and keeps the fluid biopsy market on a stable expansion path.

ctDNA supplied 45.53% of the 2024 biomarker revenue, reflecting a decade of cumulative clinical validation and regulatory clearance. However, vesicle-based assays are scaling at a 19.15% CAGR because lipid membranes protect analytes from degradation, yielding higher analytical sensitivity in Stage I diagnoses. Combined protein and RNA cargo analysis inside exosomes supplies orthogonal data that improve false-positive discrimination. Multi-analyte tests pairing ctDNA with vesicle metrics push positive predictive values into imaging-equivalent ranges without procedural risks.

Circulating tumor cells hold niche relevance for phenotyping metastatic progression, while microRNA signatures supplement histology-agnostic programs. Integrative AI pipelines now fuse fragmentomics, methylation, and vesicle-cargo data, enabling tissue-of-origin predictions with sub-10-millimeter tumor burden. Investors prioritizing early-detection claims channel capital into vesicle startups, anticipating premium reimbursement for screening code sets once sensitivity hurdles are cleared. The biomarker race diversifies revenue streams, reducing single-analyte dependence and fostering innovation across the fluid biopsy industry.

The Fluid Biopsy Market Report is Segmented by Indication (Lung Cancer, Breast Cancer, and More), Biomarker Type (Circulating Tumor Cells, and More), Product & Service (Kits & Reagents, and More), Technology (Next-Generation Sequencing (NGS), and More), End User (Reference Laboratories and More), Sample Type (Blood, Urine, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 38.72% of global fluid biopsy market revenue in 2024, supported by FDA breakthrough pathways, generous Medicare coverage, and a dense ecosystem of academic-industry collaborations. United States oncology networks absorb the majority of test volumes, while cross-border patients to Canada and Mexico augment regional demand. Ongoing policy efforts to harmonize sample-handling standards aim to reduce inter-lab variability and protect reimbursement levels tied to quality measures.

Asia-Pacific records the fastest 19.52% CAGR through 2030 as China, Japan, and India expand molecular oncology budgets. China's 2024 approval of a methylation-based liver cancer assay underscores regulatory willingness to catalyze domestic innovation. Japan's recent companion diagnostic endorsements for targeted therapies reflect sophisticated regulator-industry dialogue that accelerates product cycles. Government-linked manufacturing incentives lower localized reagent costs, further stimulating uptake.

Europe occupies a mature but still expanding position. Harmonized in-vitro diagnostic regulation, coupled with growing evidence packages, prompts national payers to reimburse MRD monitoring beyond pilot programs. Germany, France, and the United Kingdom anchor market demand through comprehensive cancer centers that value integrated genomic reports. Southern Europe and Scandinavia follow via pan-European procurement schemes that cut acquisition costs. Middle East, Africa, and South America remain nascent but demonstrate increasing trial participation, foreshadowing longer-term commercial opportunities once reimbursement pathways formalize.

- Guardant Health

- Roche

- Illumina

- Grail

- Bio-Rad Laboratories

- Qiagen N V

- Foundation Medicine

- Natera

- Thermo Fisher Scientific

- Exact Sciences

- NeoGenomics Laboratories

- Inivata

- Lucence Diagnostics

- Predicine Inc.

- LungLife AI

- Exosome Diagnostics

- Biocept

- Angle plc

- Adaptive Biotechnologies

- Singlera Genomics

- Oncocyte Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Preference For Non-Invasive Oncology Diagnostics

- 4.2.2 Rapid Increase In Global Cancer Incidence

- 4.2.3 Sequencing-Cost Decline & NGS Workflow Automation

- 4.2.4 Reimbursement Expansion For Minimal Residual-Disease (MRD) Blood Tests

- 4.2.5 AI-Driven Fragmentomics Boosting Early-Stage Detection Accuracy

- 4.2.6 Venture Capital Inflow To Decentralized Fluid-Biopsy Platforms

- 4.3 Market Restraints

- 4.3.1 High Test Cost & Reimbursement Hurdles

- 4.3.2 Emerging Optical-Biopsy & Imaging Substitutes

- 4.3.3 Pre-Analytical Sample-Handling Variability

- 4.3.4 Low ctDNA Yield In Early-Stage Tumors

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Indication

- 5.1.1 Lung Cancer

- 5.1.2 Breast Cancer

- 5.1.3 Colorectal Cancer

- 5.1.4 Prostate Cancer

- 5.1.5 Pancreatic Cancer

- 5.1.6 Other Indications

- 5.2 By Biomarker Type

- 5.2.1 Circulating Tumour Cells (CTCs)

- 5.2.2 Circulating Tumour DNA (ctDNA)

- 5.2.3 Cell-free DNA (cfDNA)

- 5.2.4 Extracellular Vesicles / Exosomes

- 5.2.5 Other Biomarkers (miRNA, TEPs, proteins)

- 5.3 By Product & Service

- 5.3.1 Kits & Reagents

- 5.3.2 Instruments & Platforms

- 5.3.3 Software & Bioinformatics

- 5.3.4 Testing Services

- 5.4 By Technology

- 5.4.1 Next-Generation Sequencing (NGS)

- 5.4.2 Digital PCR / ddPCR

- 5.4.3 Real-Time PCR

- 5.4.4 Microarray & qPCR

- 5.4.5 Other (Nanopore, Lab-on-Chip, etc.)

- 5.5 By End User

- 5.5.1 Reference Laboratories

- 5.5.2 Hospital & Physician Labs

- 5.5.3 Academic & Research Centers

- 5.5.4 CROs & Biopharma

- 5.6 By Sample Type

- 5.6.1 Blood (Plasma/Serum)

- 5.6.2 Urine

- 5.6.3 Saliva / Sputum

- 5.6.4 Cerebrospinal Fluid

- 5.6.5 Other Body Fluids

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Guardant Health

- 6.3.2 Roche Diagnostics

- 6.3.3 Illumina Inc.

- 6.3.4 Grail Inc.

- 6.3.5 Bio-Rad Laboratories

- 6.3.6 Qiagen N V

- 6.3.7 Foundation Medicine

- 6.3.8 Natera Inc.

- 6.3.9 Thermo Fisher Scientific

- 6.3.10 Exact Sciences

- 6.3.11 NeoGenomics Laboratories

- 6.3.12 Inivata Ltd

- 6.3.13 Lucence Diagnostics

- 6.3.14 Predicine Inc.

- 6.3.15 LungLife AI Inc.

- 6.3.16 Exosome Diagnostics

- 6.3.17 Biocept Inc.

- 6.3.18 Angle plc

- 6.3.19 Adaptive Biotechnologies

- 6.3.20 Singlera Genomics

- 6.3.21 Oncocyte Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment