PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850311

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850311

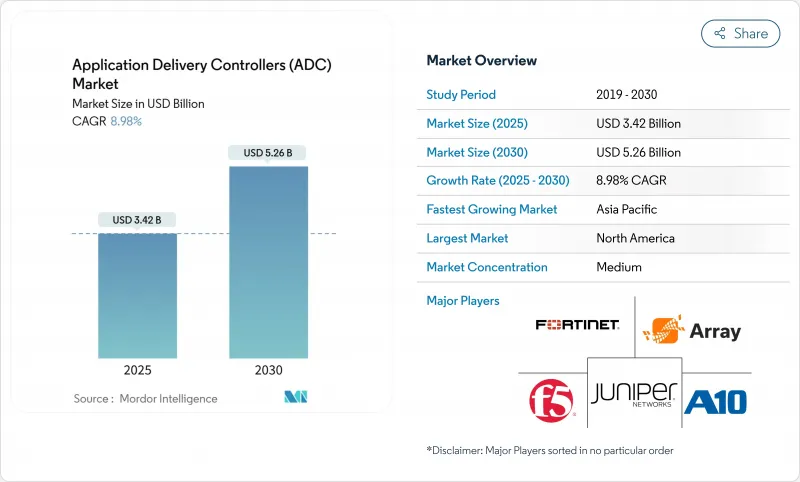

Application Delivery Controllers (ADC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The application delivery controllers market size stands at USD 3.42 billion in 2025 and is set to reach USD 5.26 billion by 2030, expanding at an 8.98% CAGR.

Rapid migration to cloud-native architectures, rising east-west data-center traffic, and persistent multi-cloud strategies keep demand high for intelligent, security-aware traffic-management platforms. Vendors now bundle advanced Layer-7 security, API protection, and AI-assisted analytics into single offerings, allowing enterprises to improve user experience while containing risk. Hardware appliances still dominate performance-critical workloads, yet virtual and cloud-managed form factors are scaling faster as organizations prioritize agility and consumption-based economics. Regionally, North America leverages mature IT estates and regulatory tailwinds to hold leadership, while Asia-Pacific's 5G build-outs and digital initiatives create the steepest growth curve.

Global Application Delivery Controllers (ADC) Market Trends and Insights

Shift Toward Cloud-Native And Microservices Architecture

More than half of enterprise workloads already run as containerized or serverless components, forcing the application delivery controllers market to pivot toward lightweight, API-centric form factors that sit inside Kubernetes clusters and service meshes. These micro-gateways inject granular traffic steering, mutual-TLS termination, and automated scaling hooks that match the ephemeral nature of modern applications . Vendors are embedding schema-aware API firewalls and distributed rate-limiters to close security gaps opened by east-west service calls. As CIOs push for platform engineering, declarative "ADC-as-code" integrates seamlessly with GitOps pipelines, reducing hand-offs between Dev and NetOps.

Exponential East-West Data-Center Traffic Growth

Virtual server density has multiplied internal flows, outpacing traditional north-south patterns and elevating latency-sensitive micro-transactions. Distributed ADC instances now sit closer to workload pods, providing pervasive telemetry and inline decryption without introducing bottlenecks . Financial exchanges, telcos, and gaming providers deploy thousands of lightweight proxies that collectively enforce Layer-7 policies yet adapt to bursty resource pools.

Complex Layer-7 Policy Configuration Burdens IT Ops

Enterprise teams confront hundreds of heterogeneous applications, each demanding bespoke routing, rewrite, or WAF logic. Maintaining accuracy across multi-cloud estates strains scarce DevSecOps talent and can stall broader ADC roll-outs. Vendors answer with intent-based templates, AI-assisted rule creation, and visual dependency maps, yet skill gaps persist.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates for Secure Digital Banking

- Growing 5G Roll-outs Driving Edge ADC Adoption

- Cost Inflation of Advanced ADC Licensing Models

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware appliances represented 59% of the application delivery controllers market in 2024, supported by specialized SSL offload chips and deterministic throughput. Yet the virtual segment is scaling at 14.6% CAGR as DevOps teams embed ADC images directly into CI/CD pipelines, reducing rack footprint and accelerating rollout windows. The application delivery controllers market size for virtual solutions is forecast to surge alongside container adoption, challenging hardware's grip on mission-critical tiers.

Mature vendors hedge by releasing container-native proxies that inherit their policy engines while shedding appliance overhead. Cost transparency plus cloud marketplace billing appeal to agile teams, driving incremental share gains for software even inside traditional enterprises. As TLS 1.3 and QUIC adoption climb, code-level agility will further tilt decisions toward software form factors, though hardware will persist for ultra-high TPS gateways in finance and telecom cores.

On-premise instances still command 64% of the application delivery controllers market size in 2024, favored by sectors bound to data-sovereignty mandates. Integrated threat analytics modules and pay-as-you-grow capacity licensing now refresh legacy estates without forklift replacements .

Conversely, the cloud-managed model rises at 15.2% CAGR as platform teams offload patching, scaling, and telemetry to vendor-operated control planes. Multi-region rollouts complete in hours, and unified API policy enforcement eliminates site-level drift, making it the preferred path for digital-native firms. The application delivery controllers market continues to blend these modes through hybrid dashboards that configure hardware, virtual, and SaaS endpoints from a single console.

Application Delivery Controllers (ADC) Market is Segmented by Type (Hardware-Based ADC, Virtual/Software ADC), Deployment (On-Premise, Cloud-Managed/Hosted), Component (Solutions (Control, Acceleration, Security), Services (Integration, Managed, Training)), Enterprise Size (Large Enterprises, Smes), End-User Vertical (IT and Telecom, BFSI, and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 34% of the application delivery controllers market in 2024, buoyed by hyperscaler ecosystems and stringent data-privacy regulations that elevate integrated security requirements. Consolidation plays, such as F5's reported displacement of hundreds of Citrix NetScaler estates, demonstrate churn within mature accounts.

Asia-Pacific delivers the steepest 12.8% CAGR as 5G rollouts and Industry 4.0 agendas spur demand for low-latency, multi-tenant ADC fabrics across factories and smart cities. Government cloud programs in China and India embed ADC functionality inside sovereign clouds, driving local vendor partnerships.

Europe balances on-prem and cloud adoption, reinforced by DORA compliance deadlines influencing bank and fintech upgrades. Regulators' focus on data residency fuels demand for policy-driven location fencing.

Middle East and Africa tap ADCs to underpin USD 3.7 trillion in megaproject construction, IoT-enabled utilities, and nationwide digital-government portals. Hybrid models satisfy both performance needs and limited regional data-center footprints.

South America's financial-services modernization and retail e-commerce spur incremental uptake, with cloud-based ADCs preferred to circumvent capital constraints amid economic volatility.

- F5 Networks Inc.

- NetScaler (Citrix Systems)

- Fortinet Inc.

- A10 Networks Inc.

- Array Networks Inc.

- Radware Ltd.

- Akamai Technologies Inc.

- Cisco Systems Inc.

- Barracuda Networks Inc.

- HAProxy Technologies LLC

- Kemp Technologies (Progress Software)

- Loadbalancer.org Inc.

- Cloudflare Inc.

- Dell Technologies Inc.

- Amazon Web Services (ALB / NLB)

- Microsoft Azure (Application Gateway)

- Alibaba Cloud (Global Server Load Balancer)

- Piolink Inc.

- Sangfor Technologies Inc.

- NGINX Inc. (F5)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Toward Cloud-Native and Microservices Architecture

- 4.2.2 Exponential East-West Data-Center Traffic Growth

- 4.2.3 Regulatory Mandates for Secure Digital Banking in North America and EU

- 4.2.4 Growing 5G Roll-outs Driving Edge ADC Adoption in Asia

- 4.2.5 Rising Multi-Cloud and Hybrid IT Strategies among Global 2000

- 4.3 Market Restraints

- 4.3.1 Complex Layer-7 Policy Configuration Burdens IT Ops

- 4.3.2 Cost Inflation of Advanced ADC Licensing Models

- 4.3.3 Commoditization of Basic Load-Balancing Features

- 4.3.4 Shortage of Skilled NetOps and DevSecOps Talent

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of Macroeconomic Factors Impact on the Industry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Hardware-Based ADC

- 5.1.2 Virtual/Software ADC

- 5.2 By Deployment

- 5.2.1 On-premise

- 5.2.2 Cloud-Managed/Hosted

- 5.3 By Component

- 5.3.1 Solutions (Control, Acceleration, Security)

- 5.3.2 Services (Integration, Managed, Training)

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By End-user Vertical

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Retail and E-commerce

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Government and Public Sector

- 5.5.6 Manufacturing and Industrial 4.0

- 5.5.7 Media and Entertainment

- 5.5.8 Energy and Utilities

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Peru

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 F5 Networks Inc.

- 6.3.2 NetScaler (Citrix Systems)

- 6.3.3 Fortinet Inc.

- 6.3.4 A10 Networks Inc.

- 6.3.5 Array Networks Inc.

- 6.3.6 Radware Ltd.

- 6.3.7 Akamai Technologies Inc.

- 6.3.8 Cisco Systems Inc.

- 6.3.9 Barracuda Networks Inc.

- 6.3.10 HAProxy Technologies LLC

- 6.3.11 Kemp Technologies (Progress Software)

- 6.3.12 Loadbalancer.org Inc.

- 6.3.13 Cloudflare Inc.

- 6.3.14 Dell Technologies Inc.

- 6.3.15 Amazon Web Services (ALB / NLB)

- 6.3.16 Microsoft Azure (Application Gateway)

- 6.3.17 Alibaba Cloud (Global Server Load Balancer)

- 6.3.18 Piolink Inc.

- 6.3.19 Sangfor Technologies Inc.

- 6.3.20 NGINX Inc. (F5)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment