PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851505

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851505

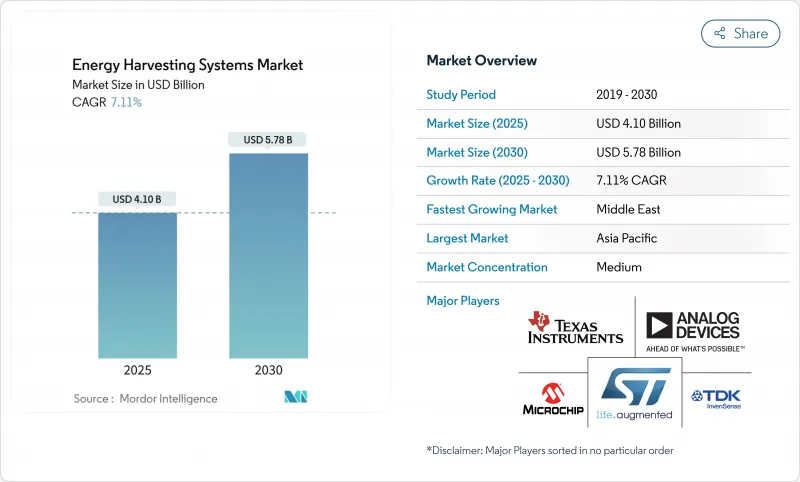

Energy Harvesting Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The energy harvesting systems market size is USD 4.10 billion in 2025 and is forecast to climb to USD 5.78 billion by 2030, advancing at a 7.11% CAGR.

Rising demand for battery-free Internet-of-Things (IoT) devices and the spread of ultra-low-power electronics across industrial and consumer environments underpin this growth. Momentum stems from rapid miniaturization in power-management integrated circuits that now squeeze sophisticated regulation functions into sub-millimeter footprints, while policy pressure to cut disposable battery waste reinforces the value proposition for energy harvesting solutions. Developers also benefit from ecosystem partnerships that speed time-to-market for turnkey modules and reference designs, further lifting adoption in smart buildings, factories, and wearables. Together, these forces strengthen the energy harvesting systems market outlook during the current decade.

Global Energy Harvesting Systems Market Trends and Insights

Proliferation of Battery-less IoT Sensor Nodes in Smart Buildings

The European Union Ecodesign Regulation 2024/1781 obliges commercial properties to use energy-efficient control systems, which pushes building managers toward battery-free wireless sensors Demonstrations in Paris and Oviedo logged 36.8 kW average power savings after integrating solar and RF-powered sensors that communicate occupancy and environmental data. RF harvesters convert 10-50% of ambient energy and more than 70% in tuned indoor zones, keeping sensors operational for the entire building life cycle. Facility owners increasingly weigh total cost of ownership and find that three battery replacement cycles eclipse initial sensor hardware costs, accelerating migration to harvesting solutions. As procurement teams pivot budgets from maintenance to analytics-ready hardware, the energy harvesting systems market gains sustained demand from the commercial real-estate sector.

Mandates for Sustainable Low-Power Automation in APAC Factories

Industrial groups across China, Japan, and South Korea install harvesters to satisfy corporate carbon pledges and cut unscheduled downtime tied to battery swaps. Telefonica Tech rolled out ATEX-certified thermoelectric generators that power vibration nodes in oil and gas refineries where battery access is tightly restricted. Researchers at the Korea Institute of Science and Technology combined thermoelectric and piezoelectric effects in a hybrid harvester that boosts power output by more than 50% for heavy-machinery monitoring. Dense manufacturing ecosystems allow quick feedback loops between pilot deployments and component suppliers, further trimming bill-of-materials cost. As regulatory audits emphasize energy baselines in production plants, executives increasingly standardize harvesting platforms across multiple factory sites, reinforcing regional momentum.

Low Energy Density of Ambient RF in Rural Installations

Field trials show that 70% of growers abandon wireless sensor pilots because nodes exhaust batteries faster than expected, a gap magnified where RF density dips below harvestable levels. Agritech integrators now blend small solar tiles with vibration strips on irrigation pumps to hedge against cloudy seasons and weak RF signals. Even so, hybrid designs raise costs and complicate maintenance schedules, delaying wide deployment in cost-sensitive farms. Until rural connectivity infrastructure expands, this restraint caps immediate upside for the energy harvesting systems market in agriculture and environmental monitoring.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Miniaturization of Ultra-Low-Power MCUs Enabling Sub-µW Thresholds

- Growing Deployment of Wireless Condition-Monitoring in Rail & Aviation OEMs

- Absence of Universal Power-Management Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Light-based photovoltaic harvesters controlled 42% of the energy harvesting systems market share in 2024. Superior maturity, low cost per watt, and predictable diurnal energy profiles keep photovoltaics in pole position for building and outdoor installations. RF harvesting, however, posts an 11% CAGR to 2030 as dense 5G deployments raise ambient electromagnetic levels that can be scavenged for sensor power. Vibration and electromagnetic harvesters serve machinery where rotational energy is plentiful, while thermal Seebeck devices find niches in automotive exhaust and industrial furnaces. Hybrid architectures that blend multiple modalities deliver continuity during light or motion lulls, appealing to mission-critical use cases. The energy harvesting systems market gains resilience as integrators pair intelligent maximum-power-point tracking with adaptive storage to optimize yield across variable sources.

Hybrid proof points abound. Ambient Photonics records triple the power output in 200 lux compared with legacy cells, unlocking indoor remote controls and keyboards. Meanwhile, the Korea Institute of Science and Technology reports a 50% power bump by merging thermoelectric and piezoelectric channels in a cantilever platform. These advances compress payback periods and extend uptime guarantees, encouraging original-equipment manufacturers to specify multi-source designs in request-for-proposal documents. As RF harvesting efficiency rises and component prices drop, the energy harvesting systems market will witness converged modules that auto-select the most productive source every few milliseconds to sustain load demands.

Power-management ICs captured 38% of the energy harvesting systems market size in 2024 by value because every harvester topology requires accurate voltage regulation and storage orchestration. Energy-harvesting transducers exhibit a 9.5% CAGR to 2030 as designers diversify beyond single-source architectures and need specialized conversion layers. Thin-film batteries and supercapacitors buffer intermittent energy streams, while ultra-low-power microcontrollers perform the analytics that justify sensor deployments. STMicroelectronics' SPV1050 achieves up to 99% conversion efficiency for photovoltaic and thermoelectric inputs, highlighting how sophisticated regulation extends node lifetimes. Asahi Kasei's AP4413 series integrates cell-balancing and trickle-charge control in a 1.43 mm2 die, bringing harvesting solutions to cost-sensitive consumer gadgets.

Industry roadmaps converge on system-on-chip packages that embed harvesting front ends, buck-boost converters, and microcontrollers within a single laminate. This consolidation removes board-level interconnect losses and simplifies certification, expanding addressable use cases from industrial automation to smart toys. Over the forecast window, falling ASPs for integration-ready PMICs will spur volume shipments, further fortifying the energy harvesting systems market.

Energy Harvesting Systems Market is Segmented by Technology (Light Energy Harvesting, Vibration Energy Harvesting, and More), Component (Energy-Harvesting Transducers, Power-Management ICs, and More), Power Range (Less Than 10 MW, 10-100 MW, and More), Application (Consumer Electronics, Building and Home Automation, Industrial IoT and Automation, and More), Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia held 35% of 2024 global revenue, benefiting from China's immense IoT roll-outs and Japan's leadership in piezoelectric materials through firms such as TDK Corporation tdk.com. Government-backed smart-city programs from Seoul to Shenzhen subsidize sensor infrastructure, while contract manufacturers in Taiwan and Malaysia offer cost-efficient assembly paths that shorten product cycles. South Korea's semiconductor ecosystem extends bespoke PMIC fabrication, and Singapore's logistics parks test large-scale ambient IoT arrays that showcase real-world harvester robustness.

The Middle East records the fastest trajectory at a 9.2% CAGR to 2030. Saudi Arabia's Vision 2030 positions renewable energy at the center of megacity planning, and indoor navigation beacons at the Al-Haram mosque now trial piezo tile flooring that converts pilgrim footsteps into grid power doi.org. Gulf Cooperation Council utilities integrate photovoltaic harvesters into smart-meter housings to avoid truck rolls for battery service. Israel and the United Arab Emirates anchor regional R&D clusters that pair nano-material labs with venture funds, accelerating commercialization timelines for high-efficiency harvesters.

North America and Europe show mature yet solid demand tied to regulatory frameworks that emphasize lifecycle sustainability. The United States Department of Energy proposes stricter standby limits for chargers, nudging appliance makers toward ambient power paths. Germany and the United Kingdom equip factories with vibration harvesters for rotating machinery, citing net present value gains over three to five years. Across these economies, engineering teams now quantify carbon abatement when selecting sensor platforms, a trend that channels steady orders into the energy harvesting systems market even where initial capital outlay is higher.

- Microchip Technology Inc.

- STMicroelectronics N.V.

- Texas Instruments Incorporated

- Analog Devices Inc.

- Renesas Electronics Corporation

- NXP Semiconductors N.V.

- onsemi (ON Semiconductor Corp.)

- TDK Corporation (InvenSense)

- Powercast Corporation

- Cymbet Corporation

- EnOcean GmbH

- e-peas S.A.

- ABB Ltd.

- Advanced Linear Devices Inc.

- Cap-XX Limited

- Fujitsu Components America Inc.

- G24 Power Ltd.

- Drayson Technologies Ltd.

- Piezo.com (Mide Technology)

- LORD MicroStrain (Parker Hannifin)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Battery-less IoT Sensor Nodes in Smart Buildings (Europe and North America)

- 4.2.2 Mandates for Sustainable Low-Power Automation in APAC Factories

- 4.2.3 Rapid Miniaturization of Ultra-Low-Power MCUs Enabling Sub-W Thresholds

- 4.2.4 Growing Deployment of Wireless Condition-Monitoring in Rail and Aviation OEMs

- 4.2.5 Integration of Photovoltaic Harvesters into Wearables and Medical Patches

- 4.3 Market Restraints

- 4.3.1 Low Energy Density of Ambient RF in Rural Installations

- 4.3.2 Absence of Universal Power-Management Standards

- 4.3.3 Competing LPWAN Batteries Reducing Need for On-Board Harvesters

- 4.3.4 High Up-front Design-Integration Costs for Transportation Retrofits

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Light (Solar/Photovoltaic) Energy Harvesting

- 5.1.2 Vibration (Piezoelectric and Electromagnetic) Energy Harvesting

- 5.1.3 Thermal (Seebeck / Thermoelectric) Energy Harvesting

- 5.1.4 RF (Radio-Frequency) Energy Harvesting

- 5.1.5 Hybrid / Multi-Source Energy Harvesting

- 5.2 By Component

- 5.2.1 Energy-Harvesting Transducers

- 5.2.2 Power-Management ICs

- 5.2.3 Energy-Storage Units (Thin-Film Batteries, Supercapacitors)

- 5.2.4 Ultra-Low-Power Sensors and MCUs

- 5.3 By Power Range

- 5.3.1 Less than 10 micro W

- 5.3.2 10-100 micro W

- 5.3.3 100 micro W-1 mW

- 5.3.4 1-10 mW

- 5.3.5 Greater than 10 mW

- 5.4 By Application

- 5.4.1 Consumer Electronics

- 5.4.2 Building and Home Automation

- 5.4.3 Industrial IoT and Automation

- 5.4.4 Transportation

- 5.4.4.1 Automotive

- 5.4.4.2 Rail

- 5.4.4.3 Aviation

- 5.4.5 Healthcare and Wearables

- 5.4.6 Defense and Security

- 5.4.7 Agriculture and Environmental Monitoring

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Nordics (Sweden, Norway, Denmark, Finland)

- 5.5.2.7 Benelux (Belgium, Netherlands, Luxembourg)

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN (Singapore, Malaysia, Thailand, Indonesia, Philippines, Vietnam)

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Israel

- 5.5.5.4 Turkey

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Microchip Technology Inc.

- 6.4.2 STMicroelectronics N.V.

- 6.4.3 Texas Instruments Incorporated

- 6.4.4 Analog Devices Inc.

- 6.4.5 Renesas Electronics Corporation

- 6.4.6 NXP Semiconductors N.V.

- 6.4.7 onsemi (ON Semiconductor Corp.)

- 6.4.8 TDK Corporation (InvenSense)

- 6.4.9 Powercast Corporation

- 6.4.10 Cymbet Corporation

- 6.4.11 EnOcean GmbH

- 6.4.12 e-peas S.A.

- 6.4.13 ABB Ltd.

- 6.4.14 Advanced Linear Devices Inc.

- 6.4.15 Cap-XX Limited

- 6.4.16 Fujitsu Components America Inc.

- 6.4.17 G24 Power Ltd.

- 6.4.18 Drayson Technologies Ltd.

- 6.4.19 Piezo.com (Mide Technology)

- 6.4.20 LORD MicroStrain (Parker Hannifin)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment