PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851797

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851797

Smart Toys - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

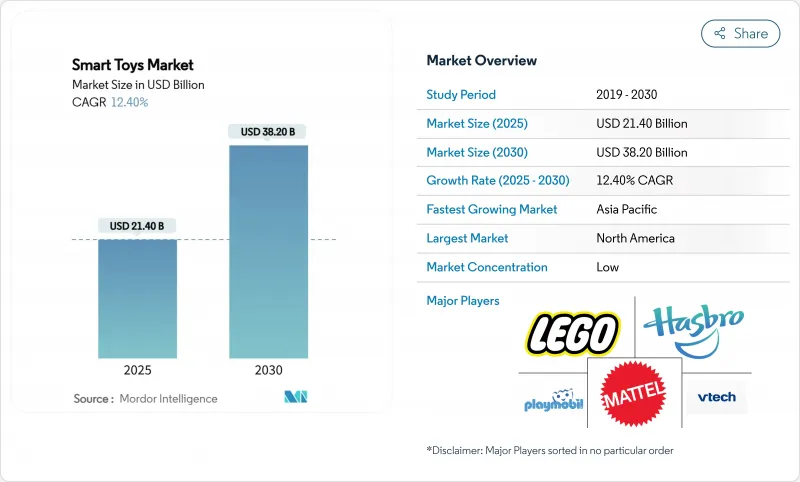

The Smart Toys Market size is estimated at USD 21.40 billion in 2025, and is expected to reach USD 38.20 billion by 2030, at a CAGR of 12.40% during the forecast period (2025-2030).

This growth is underpinned by rapid advances in kid-safe large language models, rising parental demand for screen-free learning, and regulatory clarity that protects children's data without curbing innovation. Premium connected experiences powered by edge AI and 5G are expanding average selling prices, while subscription-based content updates lengthen product life cycles and smooth revenue streams. Strategic technology partnerships between incumbent toy makers and cloud or AI vendors are compressing innovation timelines, and retailer private-label initiatives are reshaping supply-chain bargaining power. Geographically, North America retains leadership on the back of high disposable income and established ed-tech adoption, yet Asia-Pacific is accelerating fastest as governments embed hands-on robotics within STEM curricula.

Global Smart Toys Market Trends and Insights

Rapid rollout of kid-safe AI/LLM speech engines

Child-appropriate language models now enable conversational play that adapts in real time, shifting toys from pre-set scripts to genuinely interactive companions. Edge-based architectures such as the DAVID Smart-Toy platform process speech locally, guarding privacy while delivering rich dialogue. Commercial products like Curio Interactive's Grok, priced at USD 99, couple Wi-Fi connectivity with safe generative AI for children aged three and up. Shanghai-based FoloToy's Alilo Honey Bunny extends the approach with multi-language support, underscoring how natural language interaction has become a core differentiator in the premium tier

Parental shift toward screen-free interactive ed-tech

Cross-sectional studies conducted in Guangzhou and Shenzhen show that multi-sensory educational toys significantly improve engagement indices and cognitive outcomes over tablet-only alternatives. Parallel Japanese surveys reveal rising acceptance of emotional AI in early learning, indicating broad cultural readiness for physical-digital hybrids. Robotics vendor WhalesBot has already partnered with 11,000 schools across 31 countries and runs contests drawing 100,000 participants annually, validating institutional appetite for tangible coding platforms

Rising compliance costs under global children-data laws

The EU's draft Toy Safety Regulation introduces digital product passports and mental-health safeguards for connected toys, with a 30-month grace period but sweeping documentation demands. In the U.S., the Consumer Product Safety Commission is adding button-cell battery durability tests under Reese's Law, escalating certification outlays for smaller brands. These dual obligations raise engineering expenses and lengthen release cycles, favoring incumbents with dedicated regulatory teams.

Other drivers and restraints analyzed in the detailed report include:

- Retailer private-label smart-toy lines expand shelf space

- Mainstream STEM curricula mandate hands-on robotics kits

- Battery-safety recalls erode consumer trust

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smartphone-connected toys captured 45% of the smart toys market share in 2024, underlining how households leverage existing mobile hardware for control, display, and audio. Console-connected products are poised to post a 22.4% CAGR between 2025-2030, reflecting synergies with AAA gaming ecosystems and dedicated graphics pipelines.

The smartphone cohort benefits from zero incremental screens and ubiquitous mobile data, letting firms focus on sensory actuators and AI features instead of processors. TCL's modular AI companion robot "Ai Me" exemplifies this: the toy commandeers users' phones for heavy computation while delivering animated facial expressions through onboard servos. Console-linked growth springs from hardware horsepower that supports real-time, multi-user STEM simulations unreachable on mid-range handsets, enticing families already invested in home gaming.

The Smart Toys Market is Segmented by Interfacing Device (Smartphone-Connected, Tablet-Connected, Console/Other-connected), Technology(Wi-Fi, Bluetooth, and NFC/RFID and Others), Distribution Channel (Online Stores, Specialty and Convenience Stores), and Geography.

Geography Analysis

North America led with 34% of 2024 global revenue, supported by stringent but transparent safety regulations that bolster consumer confidence. Disposable income levels remain high, and parental spending on enrichment products is resilient despite a 2.2% uptick in toy prices following tariff adjustments in early 2025. Major vendors hedge risk by diversifying assembly footprints out of China; Mattel plans to drop Chinese output below 15% by 2026, reinforcing supply resilience.

Asia-Pacific is forecast to log a 14.7% CAGR to 2030, fueled by government mandates that embed robotics in STEM syllabi. China's humanoid-robot guidelines and India's USD 3 billion domestic toy program lower production costs and shorten lead times, catalyzing regional supply ecosystems. Japan's cultural affinity for emotive robotics further elevates demand for high-spec companions that blend entertainment with therapeutic value.

Europe sustains mid-single-digit expansion on the back of rigorous compliance regimes that create entry hurdles and justify price premiums. The EU's digital product passport initiative rewards firms with exhaustive traceability, aligning with consumer appetite for safe, sustainable purchases Meanwhile, South America and the Middle East & Africa show early-stage momentum as middle-class spending climbs, but currency volatility and patchy broadband slow premium penetration.

- Mattel

- LEGO Group

- Hasbro

- Spin Master

- VTech Holdings

- Playmobil (Brandstatter)

- LeapFrog Enterprises

- Sphero

- UBTECH Robotics

- WowWee Group

- Pillar Learning

- Seebo Interactive

- Curio Interactive

- TOSY Robotics

- TCL

- Fisher-Price (Mattel)

- Xiaomi (Smart Bunny line)

- Silverlit Electronics

- Miko.ai

- Casio

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study AssumptionsandMarket Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid rollout of kid-safe AI/LLM speech engines

- 4.2.2 Parental shift toward screen-free interactive ed-tech

- 4.2.3 Retailer private-label smart-toy lines expand shelf-space

- 4.2.4 Mainstream STEM curricula mandate hands-on robotics kits

- 4.2.5 5G/edge-cloud lowers latency for real-time multiplayer play

- 4.2.6 Toy-as-a-Service (TaaS) subscription models gain traction

- 4.3 Market Restraints

- 4.3.1 Rising compliance costs under global children-data laws

- 4.3.2 Battery-safety recalls erode consumer trust

- 4.3.3 Open-source firmware cloning hits premium brands

- 4.3.4 Semiconductor supply volatility inflates BOM costs

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Impact of COVID-19andSuccessive Macroeconomic Shocks

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Interfacing Device

- 5.1.1 Smartphone-connected

- 5.1.2 Tablet-connected

- 5.1.3 Console/Other-connected

- 5.2 By Technology

- 5.2.1 Wi-Fi

- 5.2.2 Bluetooth

- 5.2.3 NFC/RFIDandOthers

- 5.3 By Distribution Channel

- 5.3.1 Online Stores

- 5.3.2 SpecialtyandConvenience Stores

- 5.4 By Geography (Value)

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Russia

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, ProductsandServices, Recent Developments)

- 6.4.1 Mattel

- 6.4.2 LEGO Group

- 6.4.3 Hasbro

- 6.4.4 Spin Master

- 6.4.5 VTech Holdings

- 6.4.6 Playmobil (Brandstatter)

- 6.4.7 LeapFrog Enterprises

- 6.4.8 Sphero

- 6.4.9 UBTECH Robotics

- 6.4.10 WowWee Group

- 6.4.11 Pillar Learning

- 6.4.12 Seebo Interactive

- 6.4.13 Curio Interactive

- 6.4.14 TOSY Robotics

- 6.4.15 TCL

- 6.4.16 Fisher-Price (Mattel)

- 6.4.17 Xiaomi (Smart Bunny line)

- 6.4.18 Silverlit Electronics

- 6.4.19 Miko.ai

- 6.4.20 Casio

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-spaceandUnmet-Need Assessment