PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852150

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1852150

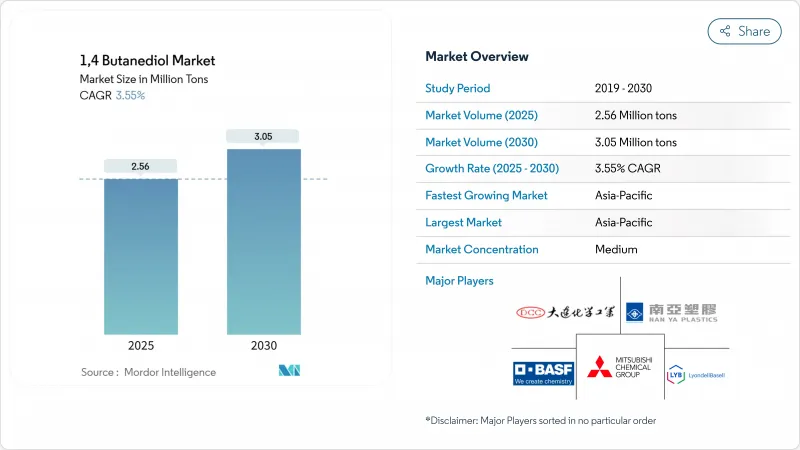

1,4 Butanediol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The 1,4 Butanediol Market size is estimated at 2.56 Million tons in 2025, and is expected to reach 3.05 Million tons by 2030, at a CAGR of 3.55% during the forecast period (2025-2030).

Output expansion rests on the interplay of incremental demand for tetrahydrofuran (THF) in spandex yarns, rising interest in polybutylene terephthalate (PBT) for electric-vehicle (EV) connectors, and the emergence of bio-fermentation routes that lower carbon intensity. Competitive intensity is rising as biotechnology licensors strike alliances with producers seeking greener capacity, while incumbent petrochemical players counter by debottlenecking Reppe-process assets. Government incentives in North America and Europe, combined with rising sustainability targets among automotive, electronics, and apparel brands, are accelerating investment in bio-based capacity even as conventional acetylene routes remain cost-competitive in coal-rich regions. At the same time, price volatility for calcium-carbide-derived acetylene and stricter health-and-safety regulations are pushing producers to diversify feedstocks.

Global 1,4 Butanediol Market Trends and Insights

Rising Demand for Tetrahydrofuran (THF) and Spandex Fibers

THF remains the pivotal derivative, feeding PTMEG for spandex yarns that underpin performance apparel, medical textiles, and automotive interiors. Spandex consumption is shifting from basic athleisure to high-function garments requiring enhanced stretch and recovery. Producers are therefore scaling catalytic upgrades such as biochar-supported Ru-Re systems that cut hydrogen usage and improve selectivity, helping stabilize margins amid recent Asian price swings. Apparel brands' push for recyclability is prompting THF suppliers to explore circular feedstocks, aligning with downstream mills that target lower scope-3 emissions. These converging dynamics keep the 1,4 butanediol market closely tied to the health of the synthetic-fiber chain.

Lightweighting Drive in EVs Fueling PBT Adoption in Auto Connectors

Automakers prioritizing energy-density gains are redesigning high-voltage architectures around PBT housings that trim system weight by 15-30% while preserving dielectric strength. Component makers report faster cycle times via injection molding versus legacy materials, enabling higher line speeds as EV demand accelerates. The North American supply base is responding with new compounding lines that pair bio-circular 1,4-butanediol with recycled polyesters, cutting product carbon footprints by over 30% and satisfying domestic content incentives. This structural tilt toward engineering thermoplastics cements a durable pull for the 1,4 butanediol market through the decade.

Health and Safety Concerns

Global regulators tighten exposure limits as 1,4 butanediol shows acute toxicity affecting the central nervous system. Europe's REACH and CLP frameworks require extensive documentation, triggering higher compliance costs and risking market exit for smaller formulators lacking advanced EHS infrastructure. Large producers mitigate this restraint via closed-loop handling and operator-training programs, yet downstream personal-care and consumer-product sectors face heightened hurdles. These dynamics temper growth in certain high-value applications and necessitate continuous investment in safety management systems across the 1,4 butanediol market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Polyurethane Applications

- Pharma-grade GBL Demand for Solvent-Based API Synthesis

- Raw Material Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 1,4 butanediol market size tied to the Reppe process stood at a commanding 70% share in 2024, underpinned by mature acetylene-based assets and favorable coal economics in China. Yet bio-fermentation volumes are scaling quickly at a 7.40% CAGR, propelled by metabolic-engineering breakthroughs that convert PET-waste-derived ethylene glycol into high-purity BDO. Commercial deployments such as the forthcoming 50,000 ton/yr Vietnamese unit highlight how licensors bridge laboratory titers with industrial purification technologies that now achieve more than 99% recovery at competitive unit costs.

Continued environmental levies on coal-based acetylene and prospective carbon-border adjustments in key export markets raise the cost bar for the Reppe route. Davy and butadiene-based syntheses offer process diversity where propylene-oxide co-product economics or regional butadiene surpluses prevail. The 1,4 butanediol market therefore reflects a portfolio approach in which producers hedge regulatory and feedstock risk by allocating capital across multiple routes while optimizing life-cycle emissions.

The 1, 4 Butanediol Market Report Segments the Industry by Production Process (Reppe Process, Davy Process, Butadiene-Based Process, and More), Derivative (Tetrahydrofuran (THF), Polybutylene Terephthalate (PBT), Gamma-Butyrolactone (GBL), and More), End-User Industry (Automotive, Textile, Electrical and Electronics, and More) and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific dominates the 1,4 butanediol market with a 76% share in 2024 and a projected 3.87% CAGR to 2030. China anchors this leadership through vast Reppe-route capacity supported by coal-derived acetylene, while new projects such as BASF's Zhanjiang Verbund site broaden regional production of engineering plastics. India and South Korea are scaling downstream elastomer, textile, and electronics plants, deepening regional integration and raising intra-Asian trade flows.

North America accounts for a meaningful share of global demand, supported by PBT usage in autos and rising bio-BDO investments. Qore's Iowa plant, scheduled to produce 66,000 tons annually from 2025, leverages corn-based dextrose and captures federal tax incentives, establishing a domestic low-carbon supply that resonates with brand-owner procurement policies. Canada and Mexico add incremental growth through automotive parts and technical-textile exports.

Europe exhibits slower headline expansion but leads in sustainability-led innovation. Novamont's Italian bio-BDO unit and multiple compounding facilities for bio-circular PBT illustrate regional alignment with circular-economy objectives. Stricter CLP compliance elevates entry barriers, encouraging specialty-grade production where premium pricing offsets higher operating costs. South America, the Middle East, and Africa contribute modest but rising demand, with Brazil's textile sector and Saudi Arabia's petrochemical clusters offering new pull for the 1,4 butanediol market.

- Ashland

- BASF SE

- Chang Chun Group

- CJ CHEILJEDANG CORP.

- DCC

- Genomatica, Inc.

- Grupa Azoty

- Henan Kaixiang Fine Chemical Co. Ltd

- Jiangsu Hailun Petrochemical Co. Ltd

- LyondellBasell Industries Holdings B.V.

- Markor Chemicals Group Co. Ltd

- Mitsubishi Chemical Group Corporation

- NAN YA PLASTICS CORPORATION

- Novamont SpA

- Shandong Yuanli Science And Technology Co. Ltd

- Shanxi Sanwei Group Co. Ltd

- Sinochem Internation Corporation

- Sipchem Company

- Xinjiang Blue Ridge Tunhe Sci.&Tech. Co., Ltd.

- Xinjiang Tianye (Group) Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

2 Study Assumptions and Market Definition

- 2.1 Scope of the Study

- 2.2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Tetrahydrofuran (THF) and Spandex Fibers

- 4.2.2 Lightweighting Drive in EVs Fueling PBT Adoption in Auto Connectors

- 4.2.3 Expansion of Polyurethane Applications

- 4.2.4 Pharma-grade GBL Demand for Solvent-Based API Synthesis

- 4.2.5 Government Subsidies for Bio-based BDO Plants in US and EU

- 4.3 Market Restraints

- 4.3.1 Health and Safety Concerns

- 4.3.2 Raw Material Price Volatility

- 4.3.3 Competition from Alternative Materials

- 4.4 Value Chain Analysis

- 4.5 Production Capacity Analysis (Major Players)

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Production Process

- 5.1.1 Reppe Process

- 5.1.2 Davy Process

- 5.1.3 Butadiene-Based Process

- 5.1.4 Propylene Oxide-Based Process

- 5.1.5 Bio-fermentation Route

- 5.2 By Derivative

- 5.2.1 Tetrahydrofuran (THF)

- 5.2.2 Polybutylene Terephthalate (PBT)

- 5.2.3 Gamma-Butyrolactone (GBL)

- 5.2.4 Polyurethane (PU)

- 5.2.5 Other Derivatives

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Textile

- 5.3.3 Electrical and Electronics

- 5.3.4 Healthcare and Pharmaceuticals

- 5.3.5 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Ashland

- 6.4.2 BASF SE

- 6.4.3 Chang Chun Group

- 6.4.4 CJ CHEILJEDANG CORP.

- 6.4.5 DCC

- 6.4.6 Genomatica, Inc.

- 6.4.7 Grupa Azoty

- 6.4.8 Henan Kaixiang Fine Chemical Co. Ltd

- 6.4.9 Jiangsu Hailun Petrochemical Co. Ltd

- 6.4.10 LyondellBasell Industries Holdings B.V.

- 6.4.11 Markor Chemicals Group Co. Ltd

- 6.4.12 Mitsubishi Chemical Group Corporation

- 6.4.13 NAN YA PLASTICS CORPORATION

- 6.4.14 Novamont SpA

- 6.4.15 Shandong Yuanli Science And Technology Co. Ltd

- 6.4.16 Shanxi Sanwei Group Co. Ltd

- 6.4.17 Sinochem Internation Corporation

- 6.4.18 Sipchem Company

- 6.4.19 Xinjiang Blue Ridge Tunhe Sci.&Tech. Co., Ltd.

- 6.4.20 Xinjiang Tianye (Group) Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Advancements in Bio-Based Production Technologies