PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906907

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906907

European Hair Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

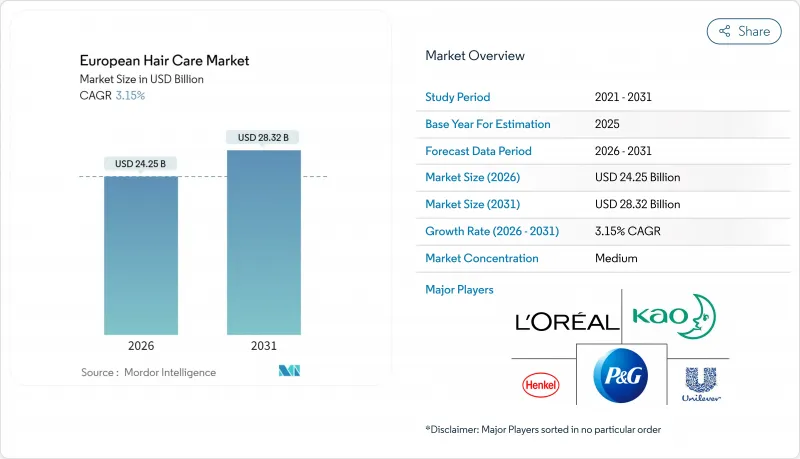

The European hair care market is expected to grow from USD 23.51 billion in 2025 to USD 24.25 billion in 2026 and is forecast to reach USD 28.32 billion by 2031 at 3.15% CAGR over 2026-2031.

As consumers in Europe increasingly prioritize wellness, sustainability, and premium experiences, the hair care market is undergoing a significant transformation, moving away from traditional mass-market offerings. While shampoos continue to dominate, there's a notable surge in demand for scalp-focused products. Brands like Head & Shoulders are expanding their anti-dandruff lines, catering to the German market's preference for science-backed efficacy. In France, the allure of botanical formulations is evident, with Klorane's plant-based shampoos drawing in buyers who lean towards natural alternatives. Sustainability is a key driver across Europe: L'Oreal is introducing refill stations in stores, while Henkel is promoting recyclable packaging for its Schwarzkopf line, both moves underscoring a shift towards eco-conscious purchasing. Social media platforms like TikTok and Instagram are becoming pivotal for younger consumers in Spain and Italy, spotlighting niche brands like Davines and Briogeo, which are witnessing growth owing to their digital-first approach. In the UK, Unilever's Dove Hair Therapy range is aligning with the hybrid work lifestyle, offering time-saving multifunctional styling products that blend care and convenience. While online platforms are emerging as vital retail channels, supermarkets and hypermarkets continue to dominate for everyday brands like Garnier and Pantene, showcasing a blend of digital and traditional shopping habits. Premium brands like Aveda and Rene Furterer are capitalizing on a growing segment of consumers willing to invest more for proven efficacy and holistic experiences.

European Hair Care Market Trends and Insights

Growing preference for organic and herbal shampoos

Driven by a heightened focus on ingredient purity, ethical sourcing, and overall wellness, European consumers are increasingly gravitating towards organic and herbal shampoos. A March 2025 study by NSF, a global public health and safety organization, found that 74% of consumers prioritize organic ingredients in personal care products . This trend is especially pronounced in Europe, where sustainability is woven into the fabric of consumer culture and regulatory policies. In late 2024, The Powder Shampoo made waves in the UK with its ECO Escapade Sets. These vegan, cruelty-free, plant-based powder-to-foam formulations come in plastic-free packaging, showcasing the innovative formats that eco-conscious shoppers are now embracing. Brands like Ethique and Plaine Products are tapping into the zero-waste movement, rolling out solid bars and refillable aluminum bottles in European outlets. Meanwhile, in Italy, heritage brands such as Davines and L'Erbolario are winning over consumers by blending tradition with eco-responsibility, using locally sourced botanicals like olive oil and rosemary. Supermarkets and pharmacies in France and Germany are increasingly dedicating shelf space to organic formulations, underscoring the rising demand for natural and chemical-free products. This momentum is not just a trend; it's propelling market expansion. As European consumers opt for premium organic choices, both established and emerging brands are responding by reformulating, innovating, and expanding their clean beauty lines.

Influence of social media and digital marketing

European hair-care brands are harnessing the power of social media and digital marketing to reshape how consumers discover, trust, and purchase their products. A 2024 survey from the University of Portsmouth revealed that about 60% of consumers place their trust in influencer recommendations, with nearly half of all purchasing decisions being influenced by these endorsements . This underscores the significant sway of genuine digital voices. For example, Hailey Bieber's Rhode brand in Europe: its strategy, heavily reliant on social media and bolstered by influencer content, has not only led to its expansion into Sephora outlets across the UK but also solidified its presence in the wider European market, moving beyond just direct-to-consumer sales. Similarly, Davines experienced a surge in demand for its OI styling mist, owing to a viral Instagram Reels campaign that showcased its effortless, plant-based shine, demonstrating the power of visual storytelling in driving product trials. In both Spain and Italy, influencers promoting Briogeo's scalp-care routines have shifted consumer focus towards more wellness-centric hair rituals. On another front, Henkel's Syoss launched a TikTok challenge-#SyossSalonAtHome-inviting users to showcase their color transformations, which not only heightened engagement but also led to a spike in e-commerce sales. These instances highlight the pivotal role of digital content and influencer credibility in seamlessly bridging the gap between inspiration and purchase, driving the expansion of the hair-care market across Europe.

High competition and market saturation

In the fiercely competitive and saturated European hair-care market, brands grapple to distinguish themselves and cultivate enduring consumer loyalty. In 2024, the prestige segment witnessed swift brand shifts: Color Wow surged from obscurity to the forefront, while Kerastase reasserted its dominance, highlighting the volatile nature of brand power in such crowded arenas. Smaller players face challenges; despite offering premium products, niche brands often find themselves eclipsed on both retail and digital platforms. This overshadowing is largely due to industry giants like L'Oreal, Unilever, and P&G, who inundate the market with frequent launches and promotions. Such tactics exert price pressures and squeeze margins, particularly for brands lacking substantial financial backing. Even established chains, like Boots, have felt the pinch, expanding their offerings to include salon-professional lines such as Kerastase and Aveda, just to remain competitive. This move underscores the limited space for smaller innovators in the market. As brands increasingly channel resources into marketing and differentiation, rather than innovation, it becomes evident that the saturation isn't just background noise; it's a pronounced hindrance to the overall dynamism of the European hair-care category.

Other drivers and restraints analyzed in the detailed report include:

- Increasing demand for men's hair care segment

- Sustainability and eco-friendly packaging

- Availability of counterfeit hair care products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In Europe's hair care market, shampoos dominate with a 38.40% share, underscoring their foundational role in consumer routines. Brands like L'Oreal Paris, Elvive, and Garnier Ultra Doux are leveraging premiumization, focusing on claims of repair, nourishment, and scalp care, which resonate with health-conscious consumers. As consumers prioritize trusted, performance-driven essentials, brands like Klorane are leading the charge with innovations like plant-based, sulfate-free shampoos, aligning with sustainability and wellness trends.

Hair styling products are witnessing the fastest growth, boasting a 3.27% CAGR, driven by social media influences and a surge in male grooming. There's a notable shift towards non-aerosol and multifunctional formats. For instance, Olaplex's Hair Perfector No. 3 mask offers deep repair, L'Oreal's Serioxyl targets thinning hair, and L'Oreal's Excellence Creme delivers professional-grade at-home coloring. Meanwhile, other segments like conditioners and hair colorants are enjoying steady growth, due to targeted claims and innovations, such as Davines' botanical conditioners emphasizing repair and protection. These trends highlight a market increasingly leaning towards multifunctional, consumer-centric solutions, fueling growth in Europe's hair care landscape.

In 2025, conventional hair care products command a dominant 72.95% market share in Europe, buoyed by established distribution channels and competitive pricing. Brands such as L'Oreal Elvive and Garnier Ultra Doux, while relying on their trusted formulations, are gradually rolling out cleaner, sulfate-free lines in response to heightened sustainability demands. Yet, even with their stronghold, these conventional products are under increasing pressure to reformulate with natural ingredients and switch to eco-friendly packaging, all in a bid to retain consumer loyalty and stay relevant in the market. A new trend is emerging: hybrid approaches that meld conventional efficacy with organic components, enabling mainstream brands to cater to consumers who prioritize performance without sidelining their natural preferences.

Organic hair care is on the rise, boasting a 4.84% CAGR, fueled by a growing consumer appetite for natural and sustainable products. Brands like Klorane with its botanical shampoos, Davines with the OI Hair Mask, and L'Oreal's organic-inspired Serioxyl serums highlight the allure of ingredient transparency and premium positioning for eco-conscious consumers. Regulatory benchmarks such as COSMOS and NATRUE not only guide informed consumer choices but also present differentiation avenues for brands that prioritize compliance and maintain verified supply chains. This shift is notably driven by younger, sustainability-focused consumers, pushing traditional brands to weave organic elements into their offerings. As this landscape evolves, it blurs the lines between categories, heightens competition for premium natural ingredients, and signals a broader market pivot towards clean and eco-friendly hair care solutions in Europe.

The European Hair Care Market Report is Segmented by Product Type (Shampoo, Conditioners, Hair Colorants, and More), Category (Organic, Conventional), Price Range (Mass, Luxury/Premium), Distribution Channel (Supermarkets/Hypermarkets, Convenience/Grocery Stores, and More), and Geography (Germany, United Kingdom, Italy, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- L'Oreal S.A.

- Henkel AG & Co. KGaA

- Pierre Fabre Dermo-Cosmetique

- Davines Group S.p.A.

- Alfaparf Milano Group S.p.A.

- L'Occitane International S.A.

- Oriflame Holding AG

- Wella Company GmbH

- Unilever PLC

- The Procter & Gamble Company

- Kao Corporation

- Beiersdorf AG

- Revlon, Inc.

- Estee Lauder Companies Inc.

- Coty Inc.

- Natura &Co Holding S.A.

- Shiseido Company, Limited

- Puig S.L.

- Herb UK Ltd.

- Weleda AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing preference for organic and herbal hair care

- 4.2.2 Influence of social media and digital marketing

- 4.2.3 Increasing demand for men's segment hair care

- 4.2.4 Rise of multifunctional shampoos with innovative active ingredients

- 4.2.5 Sustainability and eco-friendly packaging

- 4.2.6 Growing demand for AI-personalized and custom hair care

- 4.3 Market Restraints

- 4.3.1 Regulatory challenges

- 4.3.2 High competition and market saturation

- 4.3.3 Supply chain disruptions

- 4.3.4 Availability of counterfeit shampoos

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Shampoo

- 5.1.2 Conditioners

- 5.1.3 Hair Colorants

- 5.1.4 Hair Styling Products

- 5.1.5 Other Hair Care Products

- 5.2 By Category

- 5.2.1 Organic

- 5.2.2 Conventional

- 5.3 By Price Range

- 5.3.1 Mass

- 5.3.2 Luxury/Premium

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Convenience/Grocery Stores

- 5.4.3 Heath and Wellness Stores

- 5.4.4 Online Retail Stores

- 5.4.5 Other Distribution Channels

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 Italy

- 5.5.4 France

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Poland

- 5.5.8 Belgium

- 5.5.9 Sweden

- 5.5.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 L'Oreal S.A.

- 6.4.2 Henkel AG & Co. KGaA

- 6.4.3 Pierre Fabre Dermo-Cosmetique

- 6.4.4 Davines Group S.p.A.

- 6.4.5 Alfaparf Milano Group S.p.A.

- 6.4.6 L'Occitane International S.A.

- 6.4.7 Oriflame Holding AG

- 6.4.8 Wella Company GmbH

- 6.4.9 Unilever PLC

- 6.4.10 The Procter & Gamble Company

- 6.4.11 Kao Corporation

- 6.4.12 Beiersdorf AG

- 6.4.13 Revlon, Inc.

- 6.4.14 Estee Lauder Companies Inc.

- 6.4.15 Coty Inc.

- 6.4.16 Natura &Co Holding S.A.

- 6.4.17 Shiseido Company, Limited

- 6.4.18 Puig S.L.

- 6.4.19 Herb UK Ltd.

- 6.4.20 Weleda AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK