PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906981

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906981

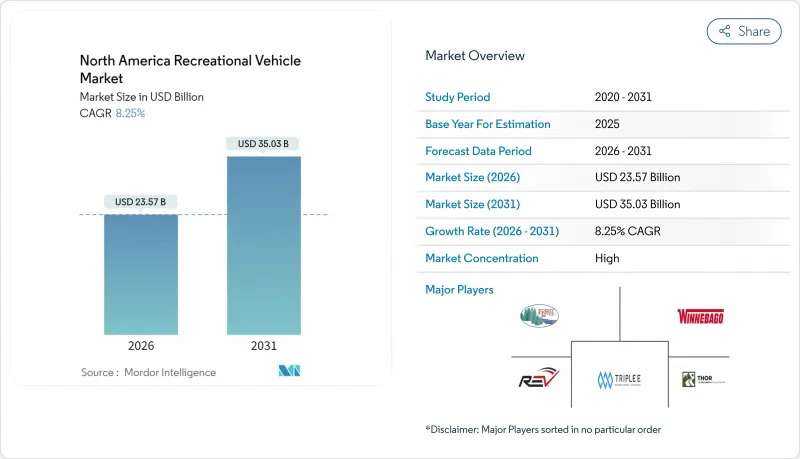

North America Recreational Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The North America RV market was valued at USD 21.77 billion in 2025 and estimated to grow from USD 23.57 billion in 2026 to reach USD 35.03 billion by 2031, at a CAGR of 8.25% during the forecast period (2026-2031).

Demand accelerates as remote work flexibility converts RVs from weekend escapes into viable long-term living spaces, while rising household ownership broadens the consumer base. Younger buyers represent a growing share of purchases, nudging product design toward connected, tech-rich floor plans. Electrified drivetrains gather momentum, helped by manufacturer commitments to hybrid and battery-electric models. Parallel growth in peer-to-peer rentals adds an access alternative that complements ownership and increases vehicle utilization. Despite macro-economic swings, the oligopolistic structure of leading suppliers speeds innovation cycles and cushions supply-chain shocks.

North America Recreational Vehicle Market Trends and Insights

Growth in Electrified & Hybrid RV Models

Battery-electric and hybrid powertrains represent the most disruptive product shift underway in the North America recreational vehicle market. Thor Industries unveiled a hybrid Class A coach featuring a 140-kWh battery pack and a gasoline range extender that delivers a 500-mile total range. The design answers range anxiety and qualifies for emerging low-emission regulations. Electric torque improves hill-climbing performance, while silent operation raises campsite comfort. Manufacturers highlight off-grid capability by pairing large battery packs with roof solar arrays, enabling auxiliary power for residential needs when parked. Sustainability messaging aligns with the Scope 1 and 2 emissions cut Thor achieved since 2019, sharpening brand appeal to eco-conscious buyers. As charging infrastructure grows, electric RV ownership barriers continue to fall.

Increased Domestic Road-Trip Tourism Post-COVID

Domestic road travel remains the preferred alternative to international trips even after border restrictions eased. Approximately 8.1 million American households own an RV, and 16.9 million are expected to own an RV in the coming five years. Average annual usage days jumped from 20 in 2021 to 30 in 2025, signaling deeper lifestyle integration. Younger cohorts under 50 now dominate new purchases, reinforcing a long replacement-demand runway. With high brand loyalty, more than 80% of pandemic-era buyers intend to repurchase the same marque, which creates predictable repeat sales for leading OEMs. The shift toward localized experiences and socially distanced recreation underpins persistent demand even as broader tourism normalizes.

Volatile Fuel Prices Increasing Trip Costs

Average U.S. gasoline prices averaged USD 3.30 per gallon in 2024, down 20 cents from 2023. Class A motorhomes consume 1 gallon every 6-10 miles, so a two-week tour can require USD 1,000 in fuel, making travel decisions sensitive to pump swings. Diesel variants face separate volatility patterns that complicate budgeting for commercial fleets. Persistently high costs have revived consumer interest in hybrid drivetrains and lighter composite materials that improve mileage. Electrification provides a structural hedge but will take years to scale due to charging-site investments.

Other drivers and restraints analyzed in the detailed report include:

- Rising Popularity of Remote Work Enabling Long-Term RV Living

- Advanced Connectivity & IoT Enhancing User Experience

- Rising Interest Rates Impacting Financing Affordability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Towable RVs held 63.52% of the North American Recreational Vehicle market share in 2025, while Motorhomes are forecast to log a 12.93% CAGR, positioning it as the principal growth engine for the North America RV market. Premium Type A models add residential finishes, slide-outs, and hybrid powertrains that reduce emissions and extend range. Type B camper vans target urban professionals who value maneuverability and stealth camping. Type C units balance price and livable space, widening appeal to families. Manufacturers deploy modular production that flexes between classes, preserving scale advantages while accommodating varied demand.

Towables retain relevance due to lower acquisition costs and the widespread availability of pickup trucks capable of towing. Travel trailers lead the category thanks to versatile floorplans and modest maintenance needs. Fifth-wheels add multi-level layouts and residential appliances suited for seasonal snowbird migration. Folding campers and truck campers serve entry-level budgets and off-road niches, respectively. This diversity keeps towable volume robust even as affluent cohorts shift into motorized products.

Private use captured 69.48% of the North American Recreational Vehicle market share in 2025, reflecting the recreational origins of the sector. Commercial usage, however, is forecast to compound at a 9.22% CAGR through 2031, outpacing the overall North America RV market size. Corporations deploy customized RVs as mobile command centers, pop-up showrooms, or temporary workforce housing on remote projects. Healthcare systems leverage self-contained clinics to expand rural reach. Hospitality firms outfit luxury units for glamping sites that command premium nightly rates.

The blurring of business and leisure travel fuels dual-use purchasing, allowing owners to classify expenses across personal and professional budgets. Tax advantages available in certain states further encourage commercial fleet formation. OEMs now offer factory-installed office pods, satellite connectivity, and generator packages that meet enterprise specifications.

The North America RV Market Report is Segmented by Type (Towable RVs and Motorhomes), Application (Private and Commercial), Fuel Type (Gasoline, Diesel, Hybrid, and Battery-Electric), Sales Channel (New RV Sales and Used RV Sales), and Geography (United States, Canada, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Thor Industries Inc.

- Forest River Inc.

- Winnebago Industries Inc.

- REV Group

- Tiffin Motorhomes Inc.

- Entegra Coach Inc.

- NeXus RV

- Cruiser RV

- Triple E Recreational Vehicles

- Newmar Corporation

- Jayco Inc.

- Airstream Inc.

- Lance Camper Manufacturing Corp.

- Pleasure-Way Industries

- Keystone RV Company

- Coachmen RV

- Grand Design RV

- Roadtrek Inc.

- Fleetwood RV

- Holiday Rambler

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth In Electrified and Hybrid RV Models

- 4.2.2 Increased Domestic Road-Trip Tourism Post-COVID

- 4.2.3 Rising Popularity Of Remote Work Enabling Long-Term RV Living

- 4.2.4 Advanced Connectivity and IoT Enhancing User Experience

- 4.2.5 Expansion Of RV-Sharing Peer-To-Peer Platforms

- 4.2.6 Favorable State Tax Incentives For Motorhome Ownership

- 4.3 Market Restraints

- 4.3.1 Volatile Fuel Prices Increasing Trip Costs

- 4.3.2 Rising Interest Rates Impacting Financing Affordability

- 4.3.3 Campground Capacity Shortages Limiting Usage

- 4.3.4 Proliferation Of RV Rental Platforms

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Type

- 5.1.1 Towable RVs

- 5.1.1.1 Travel Trailers

- 5.1.1.2 Fifth Wheel Trailers

- 5.1.1.3 Folding Camp Trailers

- 5.1.1.4 Truck Campers

- 5.1.2 Motorhomes

- 5.1.2.1 Type A

- 5.1.2.2 Type B

- 5.1.2.3 Type C

- 5.1.1 Towable RVs

- 5.2 By Application

- 5.2.1 Private

- 5.2.2 Commercial

- 5.3 By Fuel Type

- 5.3.1 Gasoline

- 5.3.2 Diesel

- 5.3.3 Hybrid

- 5.3.4 Battery-Electric

- 5.4 By Sales Channel

- 5.4.1 New RV Sales

- 5.4.2 Used RV Sales

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Thor Industries Inc.

- 6.4.2 Forest River Inc.

- 6.4.3 Winnebago Industries Inc.

- 6.4.4 REV Group

- 6.4.5 Tiffin Motorhomes Inc.

- 6.4.6 Entegra Coach Inc.

- 6.4.7 NeXus RV

- 6.4.8 Cruiser RV

- 6.4.9 Triple E Recreational Vehicles

- 6.4.10 Newmar Corporation

- 6.4.11 Jayco Inc.

- 6.4.12 Airstream Inc.

- 6.4.13 Lance Camper Manufacturing Corp.

- 6.4.14 Pleasure-Way Industries

- 6.4.15 Keystone RV Company

- 6.4.16 Coachmen RV

- 6.4.17 Grand Design RV

- 6.4.18 Roadtrek Inc.

- 6.4.19 Fleetwood RV

- 6.4.20 Holiday Rambler

7 Market Opportunities and Future Outlook

- 7.1 Autonomous RVs to transform caravanning experience

- 7.2 Subscription-based RV ownership models