PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907331

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1907331

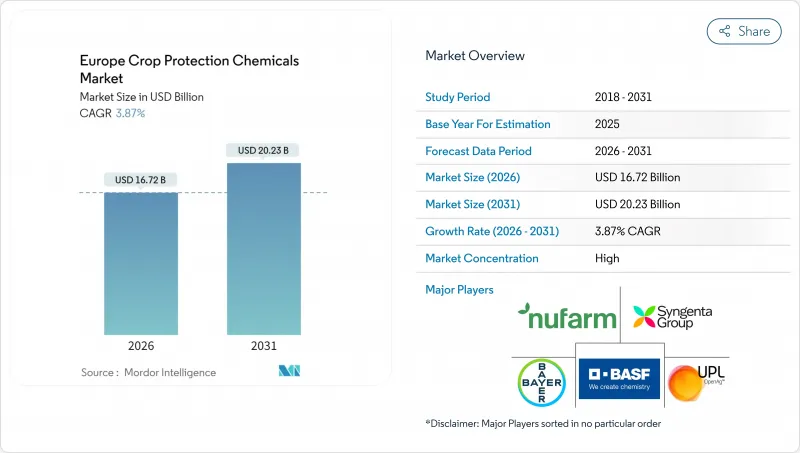

Europe Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe crop protection chemicals market was valued at USD 16.1 billion in 2025 and estimated to grow from USD 16.72 billion in 2026 to reach USD 20.23 billion by 2031, at a CAGR of 3.87% during the forecast period (2026-2031).

Sustained regulatory pressure, climate-driven pest incidence, and the premiumization of low-risk formulations together underpin this steady expansion. Farmers across the region continue to invest in integrated pest management (IPM) tools, and digital advisory platforms that balance profitability with compliance. Large manufacturers are reshaping portfolios toward biostimulant-pesticide co-formulations, while distributors integrate artificial-intelligence (AI) decision support into service packages. At the same time, price-sensitive segments in Eastern Europe adopt cost-effective generics, anchoring a two-tiered demand structure within the Europe crop protection chemicals market. Competitive intensity remains high as rising Registration, Evaluation, Authorization and Restriction of Chemicals (REACH) costs elevate scale advantages for the top players, yet novel entrants armed with RNA interference (RNAi) and microbial solutions introduce disruptive possibilities.

Europe Crop Protection Chemicals Market Trends and Insights

Expanding Integrated Pest Management Adoption

Integrated pest management adoption is rising, shifting farmer purchasing criteria from bulk volume toward targeted efficacy. The European Food Safety Authority (EFSA) recorded a 23% increase in IPM implementation during 2024, with Dutch commercial growers achieving 89% adoption. This shift increases demand for monitoring devices, selective chemistries, and biological control agents that command 15-30% price premiums. Digital scouting and sensor networks reduce active ingredient use by up to 40%, allowing suppliers to transition from volume-driven to service-oriented revenue models within the Europe crop protection chemicals market.

Surge in Conservation-Tillage Practices

Conservation tillage, including no-till and strip-till, now covers 19% of the European Union's arable land, up from 14% in 2023, according to the Joint Research Centre of the European Commission. Farmers adopt these practices to reduce soil erosion, retain moisture, and lower diesel costs, though increased weed pressure boosts herbicide demand. Equipment upgrades like high-residue disc drills and herbicide-tolerant crops drive sales of selective chemistries and precision spraying services.

Fast-track Bans on Key Actives (e.g., Glyphosate)

Accelerated reviews of legacy molecules, exemplified by the 2024 glyphosate phase-out debate, inject investment uncertainty. Sudden neonicotinoid seed-treatment bans removed USD 1.3 billion in annual sales, forcing reformulation cycles and inventory write-downs. Diversified portfolios cushion impact yet smaller firms reliant on single actives face market exit in the Europe crop protection chemicals market. This regulatory volatility favors companies with diversified product portfolios but penalizes firms dependent on specific active ingredients, creating market share redistribution opportunities for agile competitors.

Other drivers and restraints analyzed in the detailed report include:

- Climate-Change-Driven Pest Pressure

- Rapid Biostimulant Pesticide Co-formulation Launches

- Escalating Registration Costs Under REACH

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Advanced weed resistance management drives herbicide innovation as traditional active ingredients face regulatory restrictions. Herbicides command 35.01% market share in 2025, yet insecticides demonstrate superior growth dynamics with 4.45% CAGR through 2031, reflecting climate-driven pest pressure and precision application adoption. The herbicide segment confronts dual pressures from glyphosate phase-out timelines and evolved weed resistance that renders established chemistries ineffective across 40% of European agricultural land. Fungicides maintain steady demand driven by climate-induced disease pressure, while molluscicides and nematicides serve specialized market niches with limited growth potential.

Regulatory compliance under the Sustainable Use Regulation creates opportunities for companies developing novel modes of action. The European Medicines Agency's expedited review process for low-risk substances provides competitive advantages for firms investing in RNA interference technologies and microbial-based solutions. Precision application technologies enable herbicide manufacturers to maintain market share despite volume restrictions by optimizing efficacy through targeted delivery systems that reduce environmental exposure while preserving weed control effectiveness.

The Europe Crop Protection Chemicals Market is Segmented by Function (Fungicide, Herbicide, Insecticide, and More), Application Mode (Chemigation, Foliar, Fumigation, and More), Crop Type (Commercial Crops, Fruits and Vegetables, Grains and Cereals, and More), and Geography (France, Germany, Netherlands, Russia, Spain, Ukraine, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Syngenta Group

- Bayer AG

- BASF SE

- Corteva Agriscience

- FMC Corporation

- UPL Limited

- Nufarm

- Sumitomo Chemical Co., Ltd.

- Albaugh LLC

- Rovensa (Bridgepoint Group plc)

- Belchim Crop Protection (Mitsui and Co.)

- Koppert B.V.

- Sipcam SpA

- Zhejiang Wynca Chemical Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 France

- 4.3.2 Germany

- 4.3.3 Italy

- 4.3.4 Netherlands

- 4.3.5 Russia

- 4.3.6 Spain

- 4.3.7 Ukraine

- 4.3.8 United Kingdom

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Expanding Integrated Pest Management adoption

- 4.5.2 Surge in conservation-tillage practices

- 4.5.3 Climate-change-driven pest pressure

- 4.5.4 Rapid biostimulant pesticide co-formulation launches

- 4.5.5 AI-based prescription spraying platforms

- 4.5.6 Rising cereal acreage in Eastern Europe

- 4.6 Market Restraints

- 4.6.1 Fast-track bans on key actives (e.g., glyphosate)

- 4.6.2 Escalating registration costs under REACH

- 4.6.3 Counterfeit pesticide penetration via gray imports

- 4.6.4 Growing vegan / organic consumer lobby

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits and Vegetables

- 5.3.3 Grains and Cereals

- 5.3.4 Pulses and Oilseeds

- 5.3.5 Turf and Ornamental

- 5.4 Country

- 5.4.1 France

- 5.4.2 Germany

- 5.4.3 Italy

- 5.4.4 Netherlands

- 5.4.5 Russia

- 5.4.6 Spain

- 5.4.7 Ukraine

- 5.4.8 United Kingdom

- 5.4.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level overview, Core Business Segments, Financials, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Syngenta Group

- 6.4.2 Bayer AG

- 6.4.3 BASF SE

- 6.4.4 Corteva Agriscience

- 6.4.5 FMC Corporation

- 6.4.6 UPL Limited

- 6.4.7 Nufarm

- 6.4.8 Sumitomo Chemical Co., Ltd.

- 6.4.9 Albaugh LLC

- 6.4.10 Rovensa (Bridgepoint Group plc)

- 6.4.11 Belchim Crop Protection (Mitsui and Co.)

- 6.4.12 Koppert B.V.

- 6.4.13 Sipcam SpA

- 6.4.14 Zhejiang Wynca Chemical Group Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS