PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910608

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910608

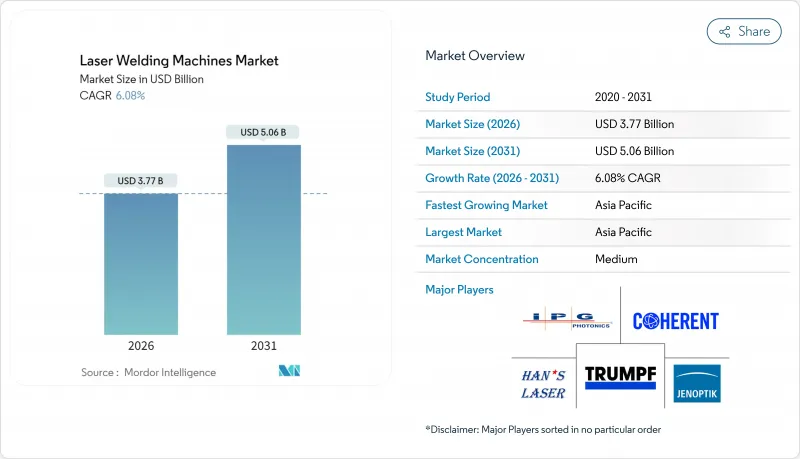

Laser Welding Machines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Laser Welding Machines market is expected to grow from USD 3.55 billion in 2025 to USD 3.77 billion in 2026 and is forecast to reach USD 5.06 billion by 2031 at 6.08% CAGR over 2026-2031.

Robust capital spending on battery-pack assembly lines, growing deployment of Industry 4.0 robotic cells, and wider availability of handheld four-in-one fiber systems are the primary engines behind this growth trajectory. The laser welding machines market also benefits from a gradual pivot away from conventional fusion methods as manufacturers seek tighter tolerances, lower heat input, and seamless automation. Material cost inflation linked to germanium and gallium restrictions has raised entry barriers, yet it simultaneously accelerates in-house laser source production among leading players. Pent-up demand for green-wavelength platforms capable of welding highly reflective copper further widens the addressable opportunity for premium vendors.

Global Laser Welding Machines Market Trends and Insights

Surge in EV-battery Pack Welding Demand

Escalating electric-vehicle penetration lifts demand for laser sources that achieve deeper copper penetration with minimal porosity. Tesla's 4680 cylindrical cells rely on welds surpassing 2 mm while maintaining electrical conductivity above 95% of base copper. Infrared lasers absorb only 5% of incident energy on copper, yet green-wavelength devices raise absorption to 35-50%, trimming spatter and rework. Premium pricing on green sources widens vendor margins, and automakers standardize these systems across future Gigafactories. The driver adds 1.2 percentage points to overall growth through mid-decade.

Hand-Held 4-in-1 Fiber Welders for SMEs

Portable units, such as IPG's LightWELD 2000 XR, consolidate welding, cutting, cleaning, and brazing in a 2 kW device priced below USD 50,000. The handheld form factor lets workshops replace multiple conventional stations while preserving mobility for field repairs. SMEs in ASEAN and Latin America acquire these systems to bypass USD 500,000 robotic installations, shrinking payback periods to under 18 months. Demand accelerates further as local banks bundle low-interest leasing packages, lifting the driver's short-term contribution to 1.1 percentage points.

High Capex Versus Arc Alternatives

Complete laser welding cells range from USD 200,000 to USD 2 million, dwarfing the USD 15,000-50,000 outlay for MIG or TIG setups. Manufacturers in lower-cost geographies where labor sits below USD 15 per hour delay adoption when ROI stretches beyond three years. Component price spikes arising from gallium and germanium restrictions inflate optics and chip costs by up to 25%, aggravating the hurdle. Financing initiatives exist, but credit access remains uneven, pulling down CAGR by 0.9 percentage points in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Green-Wavelength Copper Welding Efficiencies

- Adoption of Industry 4.0 Robotic Cells

- Shortage of Laser-Welding Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fiber platforms retained 43.68% of 2025 revenue on the back of favorable cost-performance ratios and established integrator ecosystems. The laser welding machines market size for fiber systems benefits from raw-fiber cost deflation, but beam parameter products typically hover between 4 and 8 mm-mrad, limiting ultra-fine work. Solid-state configurations, while pricier, deliver sub-2 mm-mrad outputs that drive micro-electronics and vascular stent assembly. This precision underpins a 6.43% CAGR for solid-state through 2031, the fastest inside the technology mix. Vendors hedge against cannibalization by bundling switchable beam modules that toggle between nanosecond pulsing and continuous wave. Meanwhile, CO2 lasers cling to niche plastic welding duties, and direct-diode devices secure automotive seat-back frame contracts where moderate precision suffices.

Green-wavelength units rise within the "Others" bucket because they reach copper absorption rates above 35%. TRUMPF's TruDisk Pulse sets new benchmarks in busbar welding, achieving stable keyhole regimes at 500 W average power. Integrators retrofit legacy fiber stations with frequency-doubled modules, upgrading optics rather than scrapping entire cells. The laser welding machines market captures annuity revenues from these retrofits, including calibration services and spare optics shipments, thereby thickening vendor margin profiles.

Robotic-integrated cells controlled 41.85% of the market value in 2025, owing to entrenched automotive and aerospace pipelines. These cells deliver repeatable sub-50 µm weld positioning through six-axis kinematics and vision-guided motion. However, handheld devices spark the most enthusiasm, expanding at 8.39% CAGR. The laser welding machines market share of handheld units benefits from drop-in power modules and all-in-one consumable cartridges, easing maintenance. Operators without shielding-gas infrastructure now employ built-in dual-gas nozzles that alternate between argon and nitrogen. Bench-top stations and hybrid machines target R&D labs and wafer-level packaging, respectively, but encounter slower uptake.

Field services such as ship-hull repair or wind-tower refurbishment form an untapped vein for portable systems. LightWELD 2000 XR completes on-site stainless repairs 70% faster than TIG, freeing vessels sooner. Insurance firms begin mandating laser repair in critical maritime assets, adding a regulatory tailwind to handheld adoption. Service contracts bundle training, optics swaps, and software updates under subscription, complementing initial equipment sales.

The Laser Welding Machines Market Report is Segmented by Technology (Fiber, CO2, Solid-State, and More), by System Type (Hand-held/Portable, Stationary Bench-Top, and More), by Application (Automotive, Electronics, Mining, Oil & Gas and More), by Material Type (Steel, Aluminum, Titanium, Copper, and More), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the laser welding machines market with 49.35% value in 2025 and remains the fastest-growing territory at a 7.62% CAGR to 2031. China's capacity surpassed 25,000 laser systems in 2024, with provincial governments subsidizing new plant builds to reinforce local supply chains. Japanese integrators combine precision robots with domestic fiber sources to absorb skilled-labor shortages, while South Korea channels subsidies toward battery-pack fabrication centers that demand multilayer copper welding. India's production-linked incentives nurture localized equipment assembly, reducing import duties and encouraging Western vendors to partner with Indian system houses.

North America leverages its entrenched aerospace and Class-III medical device clusters to maintain premium pricing. EV expansion across the United States Midwest accelerates green-wavelength cell installation, although germanium supply risks lift optics costs by as much as 75%. Canadian regulators fast-track rare-earth mining approvals, yet refining bottlenecks force continued import dependence. Federal tax credits under the Inflation Reduction Act reimburse up to 30% of capital expenditures on clean manufacturing assets, buffering capex sensitivity.

Europe experiences middling growth as German mid-sized machine builders contend with cost competition from Chinese entrants. The European Union's Carbon Border Adjustment Mechanism, effective 2026, incentivizes low-heat-input processes like laser welding, especially in steel-intensive sectors. Scandinavian shipyards trial handheld systems to retrofit ammonia-ready propulsion lines, while Eastern European auto plants adopt turnkey cells supplied by local integrators partnered with TRUMPF. Supply security legislation spurs consortiums to develop gallium-nitride epi-wafer capabilities inside the bloc, aiming to loosen China's stranglehold on upstream raw materials.

- TRUMPF Group

- IPG Photonics Corporation

- Han's Laser Technology Group

- Coherent Corp.

- Jenoptik AG

- Emerson Electric (Branson)

- FANUC Robotics

- Panasonic Smart Factory

- Huagong Laser Engineering

- Wuhan Golden Laser

- LaserStar Technologies

- Amada Miyachi

- Baison Laser

- Lincoln Electric (PythonX)

- Alpha Laser GmbH

- NLight Inc.

- Raycus Fiber Laser

- HGTECH

- II-VI Incorporated

- DILAS Diode Laser

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV-battery pack welding demand

- 4.2.2 Adoption of Industry 4.0 robotic cells

- 4.2.3 Hand-held 4-in-1 fiber welders for SMEs

- 4.2.4 Growth of precision medical-device assembly

- 4.2.5 Green-wavelength copper welding efficiencies

- 4.2.6 Subsidy races in China-EU clean-tech supply chains

- 4.3 Market Restraints

- 4.3.1 High capex vs. arc alternatives

- 4.3.2 Shortage of laser-welding technicians

- 4.3.3 Trade-compliance risks on dual-use lasers

- 4.3.4 Fiber-delivery contamination sensitivity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Spotlight on Laser Plastic Welding

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Technology

- 5.1.1 Fiber

- 5.1.2 CO2

- 5.1.3 Solid-State

- 5.1.4 Diode

- 5.1.5 Others (Hybrid, Green)

- 5.2 By System Type

- 5.2.1 Hand-held / Portable

- 5.2.2 Stationary Bench-top

- 5.2.3 Robotic-Integrated Cell

- 5.2.4 Hybrid Multi-Function (Weld-Cut-Clean)

- 5.3 By Application

- 5.3.1 Automotive

- 5.3.2 Electronics

- 5.3.3 Aerospace & Defense

- 5.3.4 Mining

- 5.3.5 Oil & Gas

- 5.3.6 Others (medical, jewelry, BES, etc.)

- 5.4 By Material Type

- 5.4.1 Steel

- 5.4.2 Aluminum

- 5.4.3 Titanium

- 5.4.4 Copper

- 5.4.5 Plastics & Polymers

- 5.4.6 Others (other metals nickel, nickel alloys, precious metals, magnesium & alloys, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 TRUMPF Group

- 6.4.2 IPG Photonics Corporation

- 6.4.3 Han's Laser Technology Group

- 6.4.4 Coherent Corp.

- 6.4.5 Jenoptik AG

- 6.4.6 Emerson Electric (Branson)

- 6.4.7 FANUC Robotics

- 6.4.8 Panasonic Smart Factory

- 6.4.9 Huagong Laser Engineering

- 6.4.10 Wuhan Golden Laser

- 6.4.11 LaserStar Technologies

- 6.4.12 Amada Miyachi

- 6.4.13 Baison Laser

- 6.4.14 Lincoln Electric (PythonX)

- 6.4.15 Alpha Laser GmbH

- 6.4.16 NLight Inc.

- 6.4.17 Raycus Fiber Laser

- 6.4.18 HGTECH

- 6.4.19 II-VI Incorporated

- 6.4.20 DILAS Diode Laser

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment