PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910609

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910609

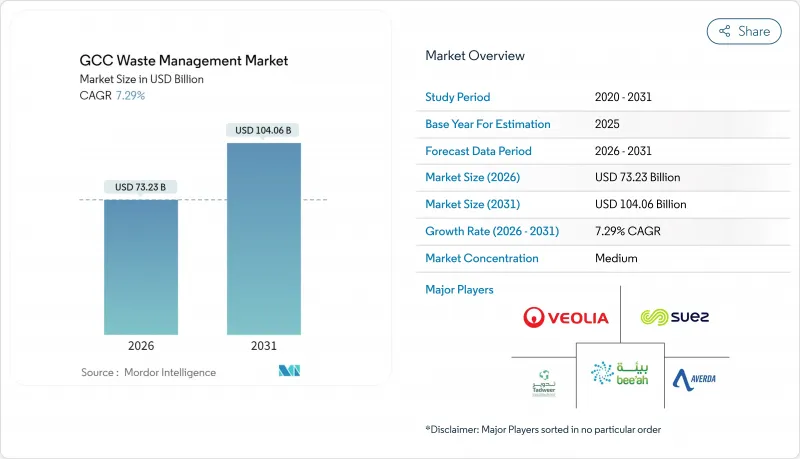

GCC Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

GCC Waste Management Market size in 2026 is estimated at USD 73.23 billion, growing from 2025 value of USD 68.25 billion with 2031 projections showing USD 104.06 billion, growing at 7.29% CAGR over 2026-2031.

Rapid urbanization, more than 80% of the region's residents now live in cities, continues to swell municipal solid waste volumes and intensify demand for modern treatment capacity. Mandatory landfill-diversion targets anchored in national visions, such as Saudi Arabia's 90% objective by 2040 and the UAE's 75% recycling ambition, convert policy pressure into steady revenue for integrated players. A rich pipeline of public-private partnerships, worth well over USD 1 trillion in broader infrastructure, is channeling private capital into large-scale waste complexes while accelerating technology transfer. Momentum is further sustained by industrial-symbiosis initiatives that funnel refuse-derived fuel to cement kilns, trimming disposal costs and cutting carbon footprints, and by reward-based reverse-vending schemes that nudge consumers toward recycling.

GCC Waste Management Market Trends and Insights

Landfill-diversion Mandates

Vision programs in Saudi Arabia and the UAE elevate waste services from a utility mindset to a strategic industry. Penalty-backed quotas compel municipalities to channel waste into recycling, composting, and energy recovery despite higher up-front costs. Incentive schemes reward early movers, lowering payback periods for new material-recovery facilities. Qatar's localized approach spurs smaller distributed assets, broadening the addressable contractor pool. ISO 14001 alignment favors players with proven compliance, tilting awards toward technology-rich multinationals.

Rapid Urban Population Growth

City-centric demographic expansion has pushed annual municipal solid waste beyond 27 million tons. Daily per-capita generation already tops 1.5 kg in Riyadh, testing conventional collection fleets. Rising affluence is shifting the composition toward packaging-heavy materials, complicating separation yet making scale economics attractive for automated sorting plants. Dense urban clusters reduce haul distances and improve plant utilization rates, supporting positive project cash flows. Urban planning codes now embed waste-management provisions, ensuring a predictable base of long-term demand.

High WTE Cost Versus Subsidized Landfill

Gate fees of USD 60-80 per ton remain needed for acceptable waste-to-energy returns, yet tip fees at subsidized landfills linger near USD 10-20 per ton, stunting plant pipelines. Smaller countries with limited tonnage struggle to unlock scale economies, and entrenched subsidy regimes resist externality pricing. Nonetheless, rising urban land prices and stricter environmental compliance steadily narrow the differential, improving bankability in dense metros such as Dubai and Abu Dhabi.

Other drivers and restraints analyzed in the detailed report include:

- PPP Surge for Waste Complexes

- Cement-kiln Co-processing Zones

- Fragmented Municipal Fee Collection

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential waste preserved a 54.03% share of the GCC waste management market in 2025, reflecting high per-capita generation tied to affluent consumption habits. Commercial waste, however, is forecast to climb 9.57% annually to 2031, fueled by retail expansion and tourism recovery across major cities. Industrial generators deploy circular-production strategies that check volume growth, whereas medical waste, about 21,000 tons in Saudi hospitals alone, commands premium treatment rates. Construction sites contribute up to 70% of Dubai's daily tonnage, creating a substantial recycled-aggregate opportunity.

Commercial growth also shifts value toward specialized sorting and organic digestion. Mixed-use megaprojects require bundled contracts that cover residential towers, hotels, and malls under single agreements, favoring operators able to scale rapidly. Institutional waste from ministries and universities offers predictable tonnage and compliance-driven margins, reinforcing demand diversity across the GCC waste management market.

The GCC Waste Management Market Report is Segmented by Source (Residential, Commercial, Industrial, and More), by Service Type (Collection, Transportation, Sorting & Segregation, and More), by Waste Type (Municipal Solid Waste, Industrial Hazardous Waste, E-Waste, Plastic Waste, Biomedical Waste, and More), and by Geography (UAE, Saudi Arabia, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Averda

- Bee'ah (Sharjah)

- Tadweer (Abu Dhabi Waste Management Co.)

- SUEZ Middle East Recycling LLC

- Veolia Middle East

- EnviroServe

- SEPCO Environment

- Saudi Investment Recycling Company

- Wasco

- Dulsco Waste Management Services

- Green Mountains

- Blue LLC

- Envac

- Power Waste Management & Transport LLC

- Al Haya Enviro

- United Waste Management Company

- Kuwait Waste Collection & Recycling Company

- Oman Environmental Services Holding Co. (be'ah Oman)

- Bin-Ovations

- Sharaf DG Recycling

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urban-population growth driving MSW volumes

- 4.2.2 Mandatory landfill-diversion targets under GCC Vision programmes

- 4.2.3 Surge in public-private partnerships (PPP) for integrated waste complexes

- 4.2.4 Industrial-symbiosis zones for cement-kiln co-processing

- 4.2.5 Commercial roll-out of reverse-vending machines in retail chains

- 4.3 Market Restraints

- 4.3.1 High levelised cost of waste-to-energy vs. subsidised landfill

- 4.3.2 Fragmented municipal fee-collection systems

- 4.3.3 Shortage of local hazardous-waste treatment capacity

- 4.3.4 Seasonal sandstorms disrupting collection logistics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Force Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Logistics Support & Infrastructure

- 4.9 Spotlight on Waste-Management Contracts

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Source

- 5.1.1 Residential

- 5.1.2 Commercial (retail, office, etc.)

- 5.1.3 Industrial

- 5.1.4 Medical (Health and Pharmaceutical)

- 5.1.5 Construction & Demolition

- 5.1.6 Others (institutional, agricultural, etc)

- 5.2 By Service Type

- 5.2.1 Collection, Transportation, Sorting & Segregation

- 5.2.2 Disposal / Treatment

- 5.2.2.1 Landfill

- 5.2.2.2 Recycling & Resource Recovery

- 5.2.2.3 Incineration & Waste-to-Energy

- 5.2.2.4 Others (Chemical Treatment, Composting, etc.)

- 5.2.3 Others (Consulting, Audit & Training, etc.)

- 5.3 By Waste Type

- 5.3.1 Municipal Solid Waste

- 5.3.2 Industrial Hazardous Waste

- 5.3.3 E-waste

- 5.3.4 Plastic Waste

- 5.3.5 Biomedical Waste

- 5.3.6 Construction & Demolition Waste

- 5.3.7 Agricultural Waste

- 5.3.8 Other Specialized Waste (radio active, etc)

- 5.4 By Country

- 5.4.1 United Arab Emirates

- 5.4.2 Saudi Arabia

- 5.4.3 Qatar

- 5.4.4 Kuwait

- 5.4.5 Oman

- 5.4.6 Bahrain

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Averda

- 6.4.2 Bee'ah (Sharjah)

- 6.4.3 Tadweer (Abu Dhabi Waste Management Co.)

- 6.4.4 SUEZ Middle East Recycling LLC

- 6.4.5 Veolia Middle East

- 6.4.6 EnviroServe

- 6.4.7 SEPCO Environment

- 6.4.8 Saudi Investment Recycling Company

- 6.4.9 Wasco

- 6.4.10 Dulsco Waste Management Services

- 6.4.11 Green Mountains

- 6.4.12 Blue LLC

- 6.4.13 Envac

- 6.4.14 Power Waste Management & Transport LLC

- 6.4.15 Al Haya Enviro

- 6.4.16 United Waste Management Company

- 6.4.17 Kuwait Waste Collection & Recycling Company

- 6.4.18 Oman Environmental Services Holding Co. (be'ah Oman)

- 6.4.19 Bin-Ovations

- 6.4.20 Sharaf DG Recycling

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment