PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911498

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911498

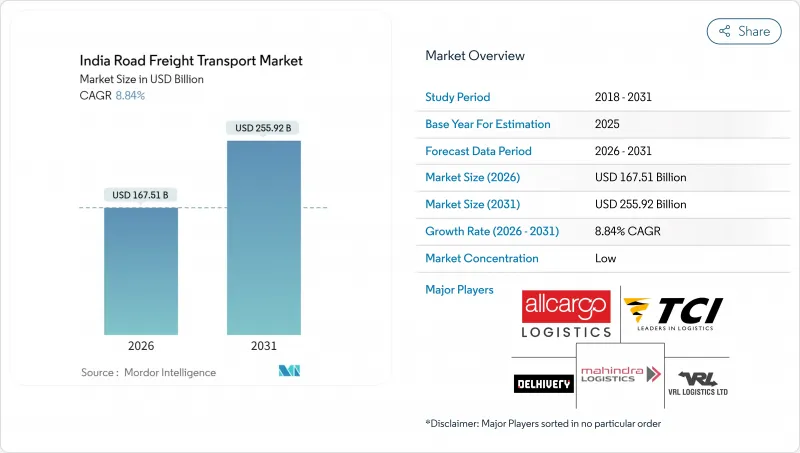

India Road Freight Transport - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

India road freight transport market size in 2026 is estimated at USD 167.51 billion, growing from 2025 value of USD 153.9 billion with 2031 projections showing USD 255.92 billion, growing at 8.84% CAGR over 2026-2031.

The headline growth mirrors India's position as the world's fastest-growing major economy, with a robust manufacturing revival, a booming e-commerce sector, and a decisive public-sector push on highways and multimodal corridors. Infrastructure additions such as the 146,145 km national highway network, widespread FASTag tolling, and the early roll-out of Dedicated Freight Corridors are shrinking transit times, lifting truck utilization, and easing capacity shortages. Organized logistics penetration is rising as GST, e-way bills, and customer-side service-level agreements push shippers toward compliant, technology-equipped providers. Meanwhile, India's rural consumption story, backed by digital payments and tier-3 and tier-4 e-commerce demand, is redrawing delivery routes and fortifying volume prospects for small and mid-distance hauls.

India Road Freight Transport Market Trends and Insights

E-commerce Fulfilment Boom Beyond Tier-1 and Tier-2 Cities

Penetration of online retail into tier-3 and tier-4 catchments is propelling steady incremental volumes for the India road freight transport market. India's e-commerce sector is tracking a 22% CAGR between 2025-2030 as rural smartphone ownership and UPI payments scale rapidly. Quick-commerce players are building micro-fulfilment hubs in secondary towns to meet ten-minute delivery pledges, raising demand for LTL consolidation and cross-docking. Delhivery now covers 18,700+ pin codes, signaling the breadth of new-age distribution lanes. Regional carriers that can negotiate state-level border checks, axle-load limits, and octroi substitutes are positioned to win loads that once stayed within informal networks. The digital payment backbone removes cash-on-delivery friction and supports transparent, trackable invoicing for small consignments.

Infrastructure Push via Bharatmala and Gati Shakti Corridors

Daily highway construction hit 40 km in 2024, underscoring the momentum behind Bharatmala's 34,800 km mandate. Integrated planning under PM Gati Shakti has compressed right-of-way approvals from multiple years to months and is aligning road, rail, and utility corridors. Improved port-to-factory links are already nudging average truck speeds upward by 15-20% on the Ahmedabad-Mumbai and Delhi-Kanpur arteries. Maersk's USD 5 billion port-side investment commitment underlines multinational confidence in corridor performance gains. The construction boom itself churns freight for cement, steel, and machinery, adding volume layers that reinforce basal manufacturing flows.

Driver Shortage and Ageing Workforce

Peak-season fleet idling due to driver gaps has clipped utilization by up to 20% on Delhi-Mumbai and Bangalore-Chennai sectors, inflating line-haul rates and stretching lead times. Young workers favor predictable shifts in e-commerce hubs over week-long interstate runs, causing an experience drain in long-haul trucking. State-run training centers work in silos, leaving skills certification uneven and safety standards patchy. Wage inflation, estimated at 12-15% year-on-year for heavy-vehicle operators, compounds cost-pass-through into shipper tariffs. Safety-tech aids help, yet human capital constraints remain a drag on capacity expansion in the India road freight transport market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Adoption of Organized 3PL/4PL Models by MSMEs

- Rapid Scaling of Digital Freight Marketplaces

- Slow Adoption of Vehicle-Scrappage Policy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Domestic manufacturing's link to Production Linked Incentive schemes is attracting electronics, auto-component, and pharmaceutical cap-ex, translating to elevated outbound tonnage. With a 10.05% CAGR between 2026-2031, manufacturing contributes the highest incremental volume to the India road freight transport market. Wholesale and Retail Trade remains the single-largest shareholder at 30.21%, powered by consumption-led FMCG and consumer durables backflows. Agriculture, Fishing, and Forestry retains a steady base, though its share inches down as industrial freight climbs.

PLI-linked factories are clustering near ports and Western Dedicated Freight Corridor junctions, prompting higher load density on Gujarat-Maharashtra-Delhi stretches. The Indian road freight transport market size for manufacturing consignments is likely to exceed USD 54.2 billion by 2031, assuming stable policy continuity and sustained foreign direct investment. Agriculture's share may steady around the low-teens as cold-chain gaps narrow, all else equal. Shipper preference for door-to-door flexibility continues to shield road carriers from modal leakage, even as Dedicated Freight Corridors bring rail into higher-value brackets.

The domestic lattice dominates today with a 63.02% share in 2025, yet future growth tilts toward cross-border links, which are clocking a 10.23% CAGR between 2026-2031. Near-term catalysts include paperless customs on the India-Bangladesh corridor and IMEC's pipeline, which promises multimodal savings on westbound cargo. Maersk's hinterland-driven port investments aim to double export-bound container capacity by 2030, lifting the international slice of the India road freight transport market.

Customs dwell time, averaging 85 hours, remains a bottleneck compared with leading Asian hubs. Digital customs and blockchain-enabled bills of lading are expected to chop that figure materially, pulling more exporters toward truck-plus-rail containerized loops. Domestic mileage will still swell as rural consumption rises, but global supply-chain realignments position India as a China-plus-one alternative, spurring bilateral lanes into GCC and Europe via emerging land-sea corridors.

Full-Truck-Load kept 80.12% share in 2025, serving minerals, steel coils, and packaged FMCG. Yet LTL's 9.89% CAGR between 2026-2031 outpaces the overall India road freight transport market. Hub-and-spoke depots in Nagpur, Indore, and Hyderabad feed rapid trans-shipment, cutting delivery promises to under 48 hours for 90% of urban pairs. Algorithms allocate mixed orders into palletized pods, lifting fill factors and shrinking per-kilo costs.

Asset-light third-party logistics use owner-operator micro fleets for last-mile links, minimizing cap-ex and accelerating coverage. Freight platforms supply dynamic dashboards that guarantee slot times, unlocking premium pricing for predictable service. FTL will remain irreplaceable for bulk commodities, yet its share ratio is projected to erode marginally as parcelization broadens.

The India Road Freight Transport Market Report is Segmented by End User Industry (Manufacturing, and More), Destination (Domestic and International), Truckload Specification (FTL and LTL), Distance (Long Haul and Short Haul), Goods Configuration (Fluid Goods and Solid Goods), Temperature Control (Non-Temperature and Temperature Controlled), and by Containerization. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- A.P. Moller-Maersk

- Allcargo Logistics (including Gati Express)

- CJ Darcl Logistics Limited

- Delhivery Ltd.

- DHL Group

- Expeditors International of Washington, Inc.

- GEODIS

- Mahindra Logistics

- Nippon Express Holdings

- Transport Corporation of India (TCI)

- V-Trans

- Varuna Group

- VRL Logistics Ltd.

- Safexpress

- Shree Tirupati Logistics

- Xpressbees

- Om Logistics Supply Chain

- CKB Group

- Glottis

- SAR Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 GDP Distribution by Economic Activity

- 4.3 GDP Growth by Economic Activity

- 4.4 Economic Performance and Profile

- 4.4.1 Trends in E-Commerce Industry

- 4.4.2 Trends in Manufacturing Industry

- 4.5 Transport and Storage Sector GDP

- 4.6 Logistics Performance

- 4.7 Length of Roads

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Pricing Trends

- 4.11 Trucking Operational Costs

- 4.12 Trucking Fleet Size by Type

- 4.13 Major Truck Suppliers

- 4.14 Road Freight Tonnage Trends

- 4.15 Road Freight Pricing Trends

- 4.16 Modal Share

- 4.17 Inflation

- 4.18 Regulatory Framework

- 4.19 Value Chain and Distribution Channel Analysis

- 4.20 Market Drivers

- 4.20.1 E-Commerce Fulfilment Boom Beyond Tier-1 and Tier-2 Cities

- 4.20.2 Infrastructure Push Via Bharatmala and Gati Shakti Corridors

- 4.20.3 Growing Adoption of Organised 3PL/4PL Models by MSMEs

- 4.20.4 Duty Rationalisation for Alternative Fuels (CNG/LNG)

- 4.20.5 Rapid Scaling of Digital Freight Marketplaces

- 4.20.6 Green-Lane Policy for Time-Critical Perishables

- 4.21 Market Restraints

- 4.21.1 Driver Shortage and Ageing Workforce

- 4.21.2 Slow Adoption of Vehicle-Scrappage Policy Keeps Ageing Fleet Operational, Raising Costs

- 4.21.3 Toll-Cost Inflation Despite FASTag Automation

- 4.21.4 Limited Cold-Chain Nodes Outside Metros

- 4.22 Technology Innovations in the Market

- 4.23 Porter's Five Forces Analysis

- 4.23.1 Threat of New Entrants

- 4.23.2 Bargaining Power of Buyers

- 4.23.3 Bargaining Power of Suppliers

- 4.23.4 Threat of Substitutes

- 4.23.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 End User Industry

- 5.1.1 Agriculture, Fishing, and Forestry

- 5.1.2 Construction

- 5.1.3 Manufacturing

- 5.1.4 Oil and Gas, Mining and Quarrying

- 5.1.5 Wholesale and Retail Trade

- 5.1.6 Others

- 5.2 Destination

- 5.2.1 Domestic

- 5.2.2 International

- 5.3 Truckload Specification

- 5.3.1 Full-Truck-Load (FTL)

- 5.3.2 Less than-Truck-Load (LTL)

- 5.4 Containerization

- 5.4.1 Containerized

- 5.4.2 Non-Containerized

- 5.5 Distance

- 5.5.1 Long Haul

- 5.5.2 Short Haul

- 5.6 Goods Configuration

- 5.6.1 Fluid Goods

- 5.6.2 Solid Goods

- 5.7 Temperature Control

- 5.7.1 Non-Temperature Controlled

- 5.7.2 Temperature Controlled

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 A.P. Moller-Maersk

- 6.4.2 Allcargo Logistics (including Gati Express)

- 6.4.3 CJ Darcl Logistics Limited

- 6.4.4 Delhivery Ltd.

- 6.4.5 DHL Group

- 6.4.6 Expeditors International of Washington, Inc.

- 6.4.7 GEODIS

- 6.4.8 Mahindra Logistics

- 6.4.9 Nippon Express Holdings

- 6.4.10 Transport Corporation of India (TCI)

- 6.4.11 V-Trans

- 6.4.12 Varuna Group

- 6.4.13 VRL Logistics Ltd.

- 6.4.14 Safexpress

- 6.4.15 Shree Tirupati Logistics

- 6.4.16 Xpressbees

- 6.4.17 Om Logistics Supply Chain

- 6.4.18 CKB Group

- 6.4.19 Glottis

- 6.4.20 SAR Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment