PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937349

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1937349

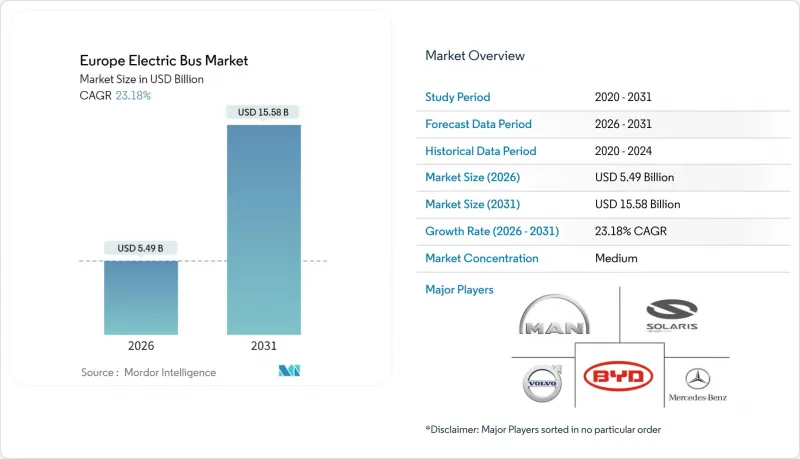

Europe Electric Bus - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe electric bus market size was valued at USD 4.46 billion in 2025 and estimated to grow from USD 5.49 billion in 2026 to reach USD 15.58 billion by 2031, at a CAGR of 23.18% during the forecast period (2026-2031).

Aggressive EU-level CO2 standards, expanding clean-vehicle procurement quotas, and widening gaps in total cost of ownership versus diesel have converged to make battery-electric buses the default option for municipal fleets. Operators increasingly favor electrification because battery prices continue to fall, charging infrastructure is backed by a EUR 1 billion EU funding stream, and ETS-2 carbon pricing is set to raise diesel fuel costs from 2027. The Europe electric bus market, therefore, combines regulatory certainty with improving economics and rising corporate appetite for sustainability branding, reinforcing the investment cycle.

Europe Electric Bus Market Trends and Insights

Falling Total Cost of Ownership Versus Diesel After 2026

Battery prices fell sharply in 2024 on wider LFP adoption, cutting pack costs by about 20% compared with NMC. When maintenance savings and ETS-2 carbon charges are added, an electric bus purchased in 2025 is projected to reach TCO parity with a diesel unit within four years of service. Early deployments of the Mercedes-Benz eCitaro in Berlin and Utrecht reveal annual maintenance savings exceeding 30% thanks to fewer drivetrain wear parts. Fleet operators are now standardizing three-shift duty cycles that push electric utilization above 96%, which accelerates payback. Such economics underpin private-sector confidence and explain why venture funding for specialized e-bus operators climbed 18% in 2025 .

EU Clean-Vehicles Directive Deadlines

Binding procurement targets under the Clean-Vehicles Directive remove uncertainty for city transport agencies, prompting multi-year tenders that bundle vehicle supply and charging solutions. Germany's Saubere-Fahrzeuge-Beschaffungs-Gesetz lifts required clean-vehicle purchases to 65% for 2026-2030, half of which must be zero-emission. Similar transpositions in France and Spain are clustering demand into large, predictable tranches that let manufacturers optimize production lines and reduce per-unit costs. National flexibility to pool targets across contracting authorities also raises purchasing power, helping smaller cities gain volume discounts. As a result, more than 49% of new EU city buses were already zero-emission in 2024, a share expected to exceed 70% by 2027 .

Grid-Connection Bottlenecks at Legacy Depots

Upgrading substations and cabling at sites built for diesel fleets remains slow because utilities face long permitting backlogs. Operators in Milan and Munich report waits of 18 months or more for 2-MW connections, forcing interim reliance on mobile chargers that limit overnight energy intake. The European Commission's Action Plan for Grids identifies a 60% increase in electricity demand by 2030, yet many city centers have little spare cabling capacity to handle clustered charging. Delays can push back contract start dates and inflate depot conversion budgets, cooling near-term delivery schedules despite healthy order books.

Other drivers and restraints analyzed in the detailed report include:

- National Zero-Emission Public-Procurement Quotas

- On-Site Depot Battery-Storage Shaving Peak-Demand Charges

- Residual-Value Uncertainty for First-Generation E-Buses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery-electric technology controlled 81.95% of the Europe electric bus market in 2025, driven by regulatory mandates and the maturing supply chain that reduce purchase price gaps. Strong policy backing, simpler drivetrains, and falling battery costs support a 24.10% CAGR for the segment through 2031. Fuel-cell buses remain a strategic hedge for routes exceeding 400 km daily, but scarce hydrogen refueling sites restrict widespread adoption. Plug-in hybrids now serve mostly in transitional contracts where depot upgrades are incomplete.

Manufacturers are standardizing power electronics and thermal-management systems across their electric and hydrogen lines, which lowers development expense. Solaris is executing a 130-unit hydrogen order for Bologna while maintaining battery-electric production at volume, ensuring flexibility if policy signals shift. Because heavy municipal subsidies target zero tailpipe emissions rather than a specific technology, fleet managers continue to pick battery-electric options for near-term compliance and cost reliability, cementing segment leadership for the next five years.

Lithium-iron-phosphate packs captured 48.75% Europe electric bus market share in 2025 and lead the category with the fastest projected expansion of 24.60% CAGR through 2031, driven by cost advantages and superior thermal stability that resonate with operator safety and economic priorities. The chemistry's cycle life of 4,000+ charge events helps operators plan for 12-year asset lives without mid-life battery swaps, cutting lifetime capex. Renault's decision to source LFP modules from CATL's Hungarian plant illustrates OEM confidence in European supply security. Lithium nickel manganese cobalt oxide remains the chemistry of choice for articulated buses that need high energy density, but rising cobalt prices and ESG scrutiny create headwinds.

Europe electric bus market size gains tied to LFP are reinforced by EU Battery Regulation recycled-content quotas that are easier to meet with iron-based cathodes. Operators in Helsinki and Vienna report battery warranty claims trending lower than early NMC fleets, signaling reduced technical risk. Over the forecast horizon, sodium-ion research may add yet another low-cost chemistry, but commercial scale is unlikely before 2030, leaving LFP dominant.

The Europe Electric Bus Market Report is Segmented by Propulsion Type (Battery Electric Bus (BEB), Plug-In Hybrid Electric Bus (PHEB), and More), Battery Chemistry (Lithium-Iron-Phosphate (LFP), Nickel-Metal Hydride (NiMH), and More), Bus Length (Less Than 9 M, 9-14 M (Standard), and More), Consumer Type, Application and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Solaris Bus & Coach sp. z o.o.

- MAN Truck & Bus

- Mercedes-Benz Group AG

- Volvo Buses

- BYD Auto Co., Ltd

- VDL Bus & Coach

- Ebusco

- IVECO Group

- Scania

- Otokar

- Van Hool

- Yutong Europe

- Irizar e-mobility

- Wrightbus

- Karsan

- CaetanoBus

- Temsa

- Bozankaya

- Switch Mobility

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU Clean-Vehicles Directive compliance deadlines

- 4.2.2 Falling total-cost-of-ownership versus diesel after 2026

- 4.2.3 National zero-emission public-procurement quotas

- 4.2.4 On-site depot battery-storage shaving peak-demand charges

- 4.2.5 Battery-as-a-Service contracts lowering capex risk

- 4.2.6 Escalating EU carbon-pricing under ETS-2 boosts diesel operating costs, accelerating e-bus switch

- 4.3 Market Restraints

- 4.3.1 Grid-connection bottlenecks at legacy depots

- 4.3.2 High residual-value uncertainty for first-generation e-buses

- 4.3.3 Potential EU tariffs on Chinese e-buses could raise system costs

- 4.3.4 Shortage of certified high-voltage maintenance technicians

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Propulsion Type

- 5.1.1 Battery Electric Bus (BEB)

- 5.1.2 Plug-in Hybrid Electric Bus (PHEB)

- 5.1.3 Fuel-Cell Electric Bus (FCEB)

- 5.2 By Battery Chemistry

- 5.2.1 Lithium-Iron-Phosphate (LFP)

- 5.2.2 Lithium Nickel Manganese Cobalt Oxide (NMC)

- 5.2.3 Nickel-Metal Hydride (NiMH)

- 5.2.4 Others (Sodium-ion, Solid-state)

- 5.3 By Bus Length

- 5.3.1 Less than 9 m

- 5.3.2 9-14 m (Standard)

- 5.3.3 Above 14 m (Articulated/Double-decker)

- 5.4 By Consumer Type

- 5.4.1 Government / Municipal Transit Agencies

- 5.4.2 Private Fleet Operators

- 5.5 By Application

- 5.5.1 Intra-city Urban Transit

- 5.5.2 Inter-city & Regional

- 5.5.3 Airport & Shuttle Services

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Netherlands

- 5.6.7 Norway

- 5.6.8 Poland

- 5.6.9 Sweden

- 5.6.10 Finland

- 5.6.11 Belgium

- 5.6.12 Switzerland

- 5.6.13 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Solaris Bus & Coach sp. z o.o.

- 6.4.2 MAN Truck & Bus

- 6.4.3 Mercedes-Benz Group AG

- 6.4.4 Volvo Buses

- 6.4.5 BYD Auto Co., Ltd

- 6.4.6 VDL Bus & Coach

- 6.4.7 Ebusco

- 6.4.8 IVECO Group

- 6.4.9 Scania

- 6.4.10 Otokar

- 6.4.11 Van Hool

- 6.4.12 Yutong Europe

- 6.4.13 Irizar e-mobility

- 6.4.14 Wrightbus

- 6.4.15 Karsan

- 6.4.16 CaetanoBus

- 6.4.17 Temsa

- 6.4.18 Bozankaya

- 6.4.19 Switch Mobility

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment