PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939085

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939085

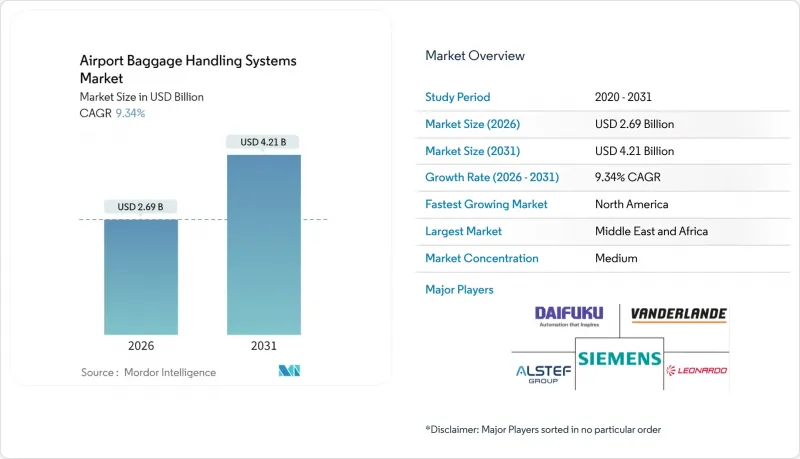

Airport Baggage Handling Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The airport baggage handling systems market was valued at USD 2.46 billion in 2025 and estimated to grow from USD 2.69 billion in 2026 to reach USD 4.21 billion by 2031, at a CAGR of 9.34% during the forecast period (2026-2031).

Growth is anchored in the aviation sector's passenger traffic rebound, steady capacity expansion pipelines, and airports' shift toward automation to hedge against labor shortages and rising security and compliance costs. Mid-life system retrofits, digital-twin-driven predictive maintenance, and computer-vision-based tracking are reshaping procurement priorities across every tier of the airport baggage handling systems market. Vendors that can combine conveyor reliability with AI-enabled analytics now command price premiums, while cybersecurity readiness has shifted from a back-office concern to a board-level procurement criterion, following regulators' tightening of incident-reporting timelines. Increasingly, capital projects bundle hybrid systems, energy-efficient motors, and UV-C disinfection modules to meet sustainability targets and public health guidelines.

Global Airport Baggage Handling Systems Market Trends and Insights

Surging Global Passenger Volumes

Passenger traffic has already surpassed pre-pandemic forecasts, placing acute strain on baggage infrastructure at hub airports that dominate the airport baggage handling systems market. The Airports Council International projects volumes will double by 2040, an outlook that accelerates equipment replacement cycles and spurs interest in expandable modular layouts. Mega-hubs processing more than 40 million travelers are adding early-baggage-storage modules and tote-based sorters to sustain throughput during peak waves. Although baggage mishandling fell to 6.9 per 1,000 passengers in 2023, each misrouted bag still costs airlines USD 100-200 in compensation and re-routing fees, driving airports to invest in AI-backed root-cause analytics. North American operators have earmarked upgrade budgets equivalent to 75% of their pre-pandemic spending over the next five years, underscoring the long-term demand floor for the airport baggage handling systems market.

Airport Capacity-Expansion Programs

Landmark projects, such as the USD 35 billion Al Maktoum International expansion, designed to handle 260 million annual passengers, illustrate the scale at which next-generation baggage systems are specified. European peers follow suit; Schiphol's EUR 6 billion (USD 8.13 billion) program modernizes its baggage basements while embedding climate-control upgrades that improve ergonomic working conditions. North American airports, from Salt Lake City to Seattle-Tacoma, are incorporating LEED-aligned motor technologies into new lines to reduce electricity consumption by up to 25% during light-load cycles. These projects generate long-tail aftermarket revenue streams for retrofit sensors, control software licenses, and cybersecurity audits within the airport baggage handling systems market.

High Capex and Long ROI Cycles

Comprehensive baggage projects routinely exceed initial budgets. Seattle-Tacoma's optimization jumped from USD 320 million to USD 540 million before commissioning, a cautionary tale for mid-tier airports evaluating similar scopes. Long payback periods of 10-15 years clash with concession periods for privatized terminals, forcing operators to securitize user-fee streams or tap green-bond structures. The Airports Council International now recommends that finance committees stress-test ROIs at hurdle rates 150 basis points above sovereign yields, yet smaller operators still find debt-service coverage challenging.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Integrated RFID Tracking

- Demand for End-to-End Automation

- Legacy IT and Interoperability Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger hubs with more than 40 million annual travelers controlled 39.88% of the airport baggage handling systems market share in 2025. These mega-facilities also posted a 10.25% CAGR, anchoring the airport baggage handling systems market size growth curve from 2026 to 2031. Their budgets support individual carrier systems, robotics, and AI-enabled control suites that smaller airports often adopt only after two technology cycles have passed. Dubai's Al Maktoum blueprint demonstrates how embedded smart conveyors and predictive-maintenance dashboards integrate with digital-twin master plans to future-proof demand surges.

Mid-tier airports in the 25-40 million bracket are closing the innovation gap by phasing upgrades, starting with early-baggage-storage zones that relieve peak-load pressure. Facilities serving 15-25 million passengers are standardizing on modular conveyors and RFID gateways to raise accuracy without full basement rebuilds. Small airports with fewer than 15 million passengers rely on shared-use, self-service devices to reduce capital expenditures and gradually expand their automation footprints. As vendor pricing falls, technology previously confined to mega-hubs flows downstream, lifting baseline expectations across every node of the airport baggage handling systems market.

Check-in and ticketing solutions represented 31.12% of the airport baggage handling systems market in 2025, reflecting their ubiquity at every terminal entrance stage. Yet, tracking and tracing solutions are experiencing a faster 10.98% CAGR, underscoring management's pivot from transaction automation to data-centric decision support. Airlines quantify mishandling cost-savings at up to USD 3 per passenger once end-to-end visibility becomes standard practice, incentivizing airports to embed RFID mats under reclaim belts and handover points.

Security screening modules retain procurement priority wherever regulators revise detection thresholds. The TSA alone earmarks USD 250 million per year for next-gen explosive detectors that must dovetail seamlessly with conveyor logic and supervisory control software. Early baggage-storage platforms monetize dwell time by offering airlines flexibility to accept bags hours in advance and even create retail pick-up services that add non-aeronautical revenue. The convergent effect continues to drive the expansion of the airport baggage handling systems market size across multiple revenue levers, not just passenger footfall growth.

The Airport Baggage Handling Systems Report is Segmented by Airport Capacity (Up To 15 Million, 15 To 25 Million, 25 To 40 Million, and Above 40 Million), Solution (Check-In and Ticketing Systems, Security Screening Systems, and More), Technology (Barcode, RFID, and More), System Type (Conveyor Belt Systems, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retains the lead in the airport baggage handling systems market, with a 31.85% share, backed by modernization mandates such as the TSA's yearly USD 250 million screening upgrade program, which fuels conveyor-maker order books. Yet, legacy infrastructure complicates expansion because retrofits must be integrated into crowded basements without interrupting operations, lifting installation schedules, and incurring additional integration costs. Canada and Mexico contribute incremental growth, but the US remains the fulcrum, owing to its dominance in the hub-and-spoke network and the maturation of its sustainability legislation.

The Middle East and Africa delivered the fastest growth, with a 12.09% CAGR, propelled by Gulf mega-projects that target passenger throughput exceeding that of many European states combined. Dubai's Al Maktoum expansion illustrates how regional planners are bypassing intermediate technology steps, installing robotics, AI dashboards, and touch-free disinfection modules in the first-phase builds. African gateways, such as Cape Town, have allocated modernization budgets exceeding USD 1 billion, although funding cycles may stagger implementation timelines. Strong cargo-volume upticks also translate into more integrated bag-and-freight handling solutions, widening the airport baggage handling systems market footprint beyond pure passenger applications.

Europe and Asia-Pacific form a technology vanguard where brownfield constraints meet stringent carbon targets. Schiphol's EUR 6 billion (USD 7.07 billion) plan rebuilds its entire baggage basement to deliver ergonomic workspaces and climate-stable conveyor halls that minimize heat-related motor failure. Asian hubs, from Hyderabad to Jakarta, operate as manufacturing outposts for global suppliers; Daifuku's new Indian plant quadruples output capacity, thereby lowering lead times for regional customers. South America remains smaller in absolute terms, but demonstrates catch-up momentum as carriers relaunch networks and airports leverage multilateral bank finance to de-risk greenfield upgrades.

- Daifuku Co. Ltd.

- Vanderlande Industries BV

- Siemens AG

- BEUMER Group GmbH & Co. KG

- Alstef Group SAS

- CIMC TianDa Holdings Co. Ltd.

- SITA N.V.

- Ansir Systems

- G&S Airport Conveyer

- Leonardo S.p.A

- Pteris Global Limited

- RBS Global Media Ltd.

- Amadeus IT Group, S.A.

- Lyngsoe Systems A/S

- Brock Solutions

- FIVES SAS

- Robson Handling Technology Ltd.

- ULMA Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging global passenger volumes

- 4.2.2 Airport capacity-expansion programs

- 4.2.3 Shift toward integrated RFID tracking

- 4.2.4 Demand for end-to-end automation

- 4.2.5 Early-baggage-storage (EBS) as revenue lever

- 4.2.6 Pandemic-driven disinfection retrofits

- 4.3 Market Restraints

- 4.3.1 High capex and long ROI cycles

- 4.3.2 Legacy IT and interoperability gaps

- 4.3.3 Airport labor unions' automation pushback

- 4.3.4 Cybersecurity compliance costs (EU NIS2/FAA AD)

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Airport Capacity

- 5.1.1 Up to 15 million

- 5.1.2 15 to 25 million

- 5.1.3 25 to 40 million

- 5.1.4 Above 40 million

- 5.2 By Solution

- 5.2.1 Check-In and Ticketing Systems

- 5.2.2 Security Screening Systems

- 5.2.3 Conveying and Sorting Systems

- 5.2.4 Early Baggage Storage

- 5.2.5 Baggage Reclaim/Unloading

- 5.2.6 Tracking and Tracing

- 5.3 By Technology

- 5.3.1 Barcode

- 5.3.2 RFID

- 5.3.3 IoT Sensors and Edge Devices

- 5.3.4 Robotics and Autonomous Vehicles

- 5.3.5 AI/ML Software

- 5.4 By System Type

- 5.4.1 Conveyor Belt Systems

- 5.4.2 Tilt-Tray and Cross-Belt Sorters

- 5.4.3 Destination-Coded Vehicle (DCV)

- 5.4.4 Tote-based/Individual Carrier Systems

- 5.4.5 Hybrid and Other Emerging Systems

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Daifuku Co. Ltd.

- 6.4.2 Vanderlande Industries BV

- 6.4.3 Siemens AG

- 6.4.4 BEUMER Group GmbH & Co. KG

- 6.4.5 Alstef Group SAS

- 6.4.6 CIMC TianDa Holdings Co. Ltd.

- 6.4.7 SITA N.V.

- 6.4.8 Ansir Systems

- 6.4.9 G&S Airport Conveyer

- 6.4.10 Leonardo S.p.A

- 6.4.11 Pteris Global Limited

- 6.4.12 RBS Global Media Ltd.

- 6.4.13 Amadeus IT Group, S.A.

- 6.4.14 Lyngsoe Systems A/S

- 6.4.15 Brock Solutions

- 6.4.16 FIVES SAS

- 6.4.17 Robson Handling Technology Ltd.

- 6.4.18 ULMA Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment