PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939155

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939155

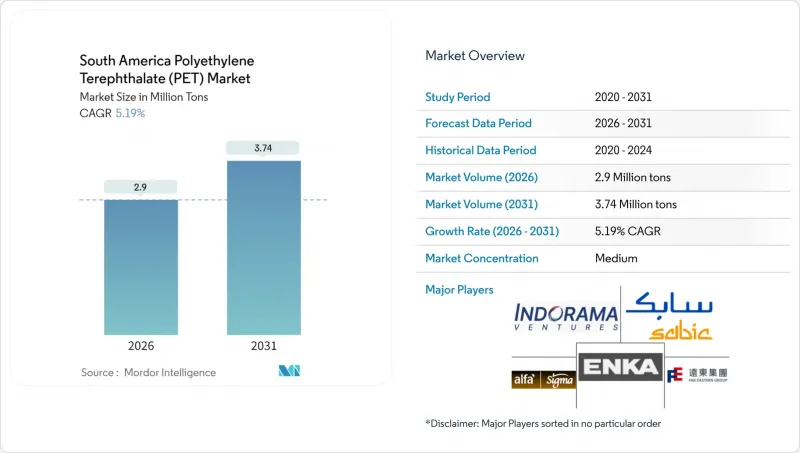

South America Polyethylene Terephthalate (PET) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The South America Polyethylene Terephthalate Market size in 2026 is estimated at 2.9 million tons, growing from 2025 value of 2.76 million tons with 2031 projections showing 3.74 million tons, growing at 5.19% CAGR over 2026-2031.

The growth curve highlights Brazil's decisive shift toward import substitution, mandatory recycled-content rules, and near-shoring moves by fast-moving consumer-goods majors that collectively anchor regional PET demand. Port congestion at Santos and Paranagua, while a short-term drag on inbound logistics, is nudging converters to favor local resin suppliers that can guarantee shorter lead times, thereby reinforcing domestic investment momentum. Active capacity expansion-such as Coca-Cola's BRL 7 billion, 14-line build-out-and public-private alliances in recycling are broadening supply options and cushioning volatility in crude-linked feedstock prices. Competitive intensity remains moderate; established multinationals leverage vertical integration, while emerging recyclers win share through collection-network outreach and technology licenses.

South America Polyethylene Terephthalate (PET) Market Trends and Insights

Brazil Mandatory Recycled-Content Targets for PET Bottles

The National Solid Waste Policy makes closed-loop recycling legally binding as of 2026, requiring beverage fillers to demonstrate that every bottle is collected and reprocessed. Brazil recycled 410,000 tons of PET in 2024, a 14% increase from 2022, yet volumes still fall short of compliance needs. Harmonized MERCOSUR food-grade rPET specifications enable producers to shuttle feedstock across borders, thereby trimming transport costs and enhancing grade uniformity. Supply chains now treat waste as a strategic asset, extending pickup routes from megacities to farming belts where bottled soft drink penetration is climbing. Investments in optical sorters and high-viscosity extrusion systems are scaling rapidly, with several facilities already boasting food-contact clearance under U.S. FDA equivalency audits. As reverse logistics reporting becomes enforceable, local players anticipate stronger bargaining power over bale pricing, thereby stabilizing input costs during crude price swings.

Growing On-Premise Beverage Demand Boosting Bottle-Grade PET

Latin America's post-pandemic leisure boom revives restaurant, stadium, and event traffic, lifting demand for premium PET bottles in the 0.31 L-0.51 L range. Coca-Cola has allocated BRL 7 billion to 14 new lines, many of which are dedicated to returnable PET, blending durability with lightweighting. PepsiCo's USD 100 million storage park in Uruguay enables same-week replenishment for 24 export markets, leveraging free-zone perks to minimize inventory holding days. Craft brewers and regional wineries are switching from glass to PET for open-air venues because weight reductions cut freight bills by up to 35% per pallet. Bottle-design differentiation-in colors, tactile finishes, and smart closures-supports higher shelf prices that absorb resin cost escalations. Equipment makers selling high-cavity blow-molders report order backlogs through late 2026, signaling sustained demand even if macroeconomic growth cools.

Crude-Oil-Linked Feedstock Price Volatility

PET margins fluctuate with shifts in naphtha and paraxylene prices, which follow changes in crude benchmarks. Petrobras plans USD 16.7 billion in refining upgrades through 2028, but fresh paraxylene or PTA streams remain unconfirmed, leaving converters exposed to Asian benchmark swings. Currency fluctuations add another layer because feedstock imports are clear in USD, while domestic sales settle in reals or pesos. Large integrated players hedge their exposures via swap arrangements and diversified cracker fleets, whereas small converters operate largely on a spot basis, absorbing immediate cost spikes. Frequent feedstock repricing complicates long-horizon project appraisals, thereby delaying the construction of green-field PET or preform plants. The volatility risk amplifies borrower-credit premiums, increasing finance costs for mid-tier recyclers seeking to incorporate solid-state reactors.

Other drivers and restraints analyzed in the detailed report include:

- Import-Substitution Push After Brazil Polymer Import-Tax Hike

- Rapid Expansion of rPET Capacity via Public-Private Partnerships

- Low South-American Recycling Infrastructure Utilization below 15%

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Packaging applications accounted for 98.58% of the 2025 volume, confirming the South America Polyethylene Terephthalate market as a packaging-centric ecosystem. The segment's structural lead reflects entrenched beverage lines, familiarity with PET's barrier properties, and widespread stretch-blow expertise. Electrical and electronics, although small, are pacing at a 7.15% CAGR and benefit from consumer electronics assemblies and low-voltage connector housings that tap PET's dielectric performance. Automotive uptake centers on fuel-tank liners and under-hood fluid reservoirs, where weight saving helps manufacturers meet efficiency norms. Building and construction uses PET sheets for daylighting and insulation, while industrial and machinery firms select PET for precision guides and pump components. Coca-Cola's 100% rPET preform pilot at Jundiai showcases packaging's sustainability vanguard, whereas Sidel's Super Combi lines enable converters to quickly switch between bottle formats, thereby protecting line uptime.

In the years ahead, additional returnable loops and tethered-cap regulations will likely consolidate packaging's share, while higher-margin electrical applications may pull incremental resin volumes as Latin American appliance output increases. Cross-learning on flame-retardant grades could broaden PET's electronics footprint, while automotive lightweighting targets foreshadow niche demand in fuel-cell stacks and battery components. Over the 2026-2031 period, packaging remains the anchor, but diversified end-use adoption helps buffer cyclical dips in beverage demand.

The South America Polyethylene Terephthalate (PET) Market Report is Segmented by End-User Industry (Automotive, Building and Construction, Electrical and Electronics, Industrial and Machinery, Packaging, and Other End-User Industries), Source Type (Virgin PET and Recycled PET), and Geography (Argentina, Brazil, and Rest of South America). The Market Forecasts are Provided in Terms of Volume (Tons) and Value (USD).

List of Companies Covered in this Report:

- Alfa S.A.B. de C.V.

- ALPLA

- China Petroleum & Chemical Corporation

- ENKA Insaat ve Sanayi A.S.

- Far Eastern New Century Corporation

- Formosa Plastics Group

- Indorama Ventures Public Company Limited

- Reliance Industries Limited

- SABIC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Brazil mandatory recycled content targets for PET bottles

- 4.2.2 Growing on-premise beverage demand boosting bottle-grade PET

- 4.2.3 Import-substitution push after Brazil polymer import-tax hike

- 4.2.4 Rapid expansion of rPET capacity via public-private partnerships

- 4.2.5 Near-shoring of FMCG bottling lines to mitigate supply-chain risks

- 4.3 Market Restraints

- 4.3.1 Crude-oil-linked feedstock price volatility

- 4.3.2 Port-congestion and customs-strike logistics bottlenecks

- 4.3.3 Low South-American recycling infrastructure utilisation below 15%

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Import And Export Trends

- 4.7 Price Trends

- 4.8 Form Trends

- 4.9 Recycling Overview

- 4.10 Regulatory Framework

- 4.11 End-use Sector Trends

- 4.11.1 Aerospace (Aerospace Component Production Revenue)

- 4.11.2 Automotive (Automobile Production)

- 4.11.3 Building and Construction (New Construction Floor Area)

- 4.11.4 Electrical and Electronics (Electrical and Electronics Production Revenue)

- 4.11.5 Packaging (Plastic Packaging Volume)

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By End-User Industry

- 5.1.1 Automotive

- 5.1.2 Building and Construction

- 5.1.3 Electrical and Electronics

- 5.1.4 Industrial and Machinery

- 5.1.5 Packaging

- 5.1.6 Other End-user Industries

- 5.2 By Source Type

- 5.2.1 Virgin PET

- 5.2.2 Recycled PET

- 5.3 By Country

- 5.3.1 Argentina

- 5.3.2 Brazil

- 5.3.3 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alfa S.A.B. de C.V.

- 6.4.2 ALPLA

- 6.4.3 China Petroleum & Chemical Corporation

- 6.4.4 ENKA Insaat ve Sanayi A.S.

- 6.4.5 Far Eastern New Century Corporation

- 6.4.6 Formosa Plastics Group

- 6.4.7 Indorama Ventures Public Company Limited

- 6.4.8 Reliance Industries Limited

- 6.4.9 SABIC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

8 Key Strategic Questions for CEOs