PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939705

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939705

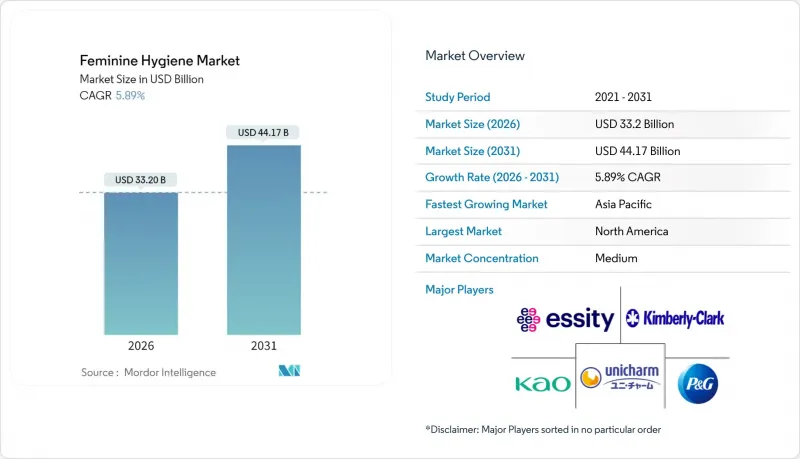

Feminine Hygiene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The feminine hygiene market was valued at USD 31.35 billion in 2025 and estimated to grow from USD 33.2 billion in 2026 to reach USD 44.17 billion by 2031, at a CAGR of 5.89% during the forecast period (2026-2031).

Heightened consumer interest in sustainable materials, widening institutional procurement mandated by menstrual equity laws, and rapid e-commerce adoption underpin this growth trajectory. North America remains the revenue leader, yet Asia-Pacific delivers the fastest incremental volumes as access programs and cultural acceptance converge with rising disposable income. Besides, disposable sanitary pads retain the largest individual category share, although reusable menstrual cups record the highest growth as value-minded and eco-conscious shoppers pivot toward long-life options. Additionally, channel dynamics continue to shift: pharmacy chains still dominate sales, but online platforms record the most robust traffic gains as discreet doorstep delivery and subscription replenishment appeal to digital-first consumers.

Global Feminine Hygiene Market Trends and Insights

Rising awareness and education about feminine hygiene and health

Educational initiatives and awareness programs are driving increased adoption of feminine hygiene products across markets. According to the United Nations International Children's Emergency Fund (UNICEF) and World Health Organization (WHO) Progress on Drinking Water, Sanitation and Hygiene in Schools 2015-2023 report, only 39% of schools provide menstrual health education. This figure varies significantly between primary schools (34%) and secondary schools in Central and Southern Asia (84%), indicating that younger girls often lack essential knowledge during the onset of menstruation . Government programs in developing markets are addressing this gap by implementing educational initiatives that improve school attendance and reduce urogenital infections through better hygiene practices. The inclusion of menstrual health in national education curricula has increased the demand for safe hygiene products over traditional alternatives like cloth rags, particularly in regions where cultural taboos have limited open discussion. Moreover, digital health platforms are expanding the reach of menstrual health education to remote and underserved communities through culturally appropriate content. This has created a network effect where educated individuals become advocates within their communities, leading to changes in consumer behavior and increased adoption of modern hygiene products. Major manufacturers such as Procter & Gamble's Always and Kenvu's Stayfree are supporting these educational initiatives through school-based campaigns and awareness programs. These efforts simultaneously advance menstrual health education and strengthen their market presence in developing regions. The combination of education, policy implementation, and corporate initiatives is transforming menstrual health awareness and contributing to market growth.

Increasing governmental and NGO initiatives promoting feminine hygiene awareness in developing regions

The feminine hygiene products market is experiencing transformation through government and NGO initiatives that position menstrual health as a public health and gender equity priority. Policy measures, such as free menstrual product programs implemented across 27 U.S. states and Washington, D.C., in January 2025, according to the Alliance for Period Supplies, have created significant institutional procurement channels that ensure consistent product demand . International development organizations integrate menstrual hygiene management into health and education programs, creating sustainable funding streams for product distribution in underserved areas. These programs often support locally manufactured products, strengthening regional suppliers and improving supply chain stability. The recognition of menstrual equity as a human rights issue has led to legislation affecting healthcare, workplace policies, and public facility requirements. This market expansion reflects broader social efforts to normalize menstruation, address cultural stigmas, and improve access to feminine hygiene products. Companies like Kotex participating in these initiatives gain enhanced institutional and public market access. These government and NGO programs create market opportunities, strengthen menstrual health's position in public policy, and support market growth through improved product accessibility, education, and empowerment.

Increasing regulation and scrutiny over personal care ingredients and claims

Increasing regulatory oversight and scrutiny regarding personal care ingredients and product claims significantly impacts manufacturers and product developers, with smaller companies facing heightened compliance burdens. The Food and Drug Administration (FDA) 2024 investigation into metal contamination in tampons, following a study that identified lead and arsenic in products across the U.S. and Europe, indicates potential future restrictions that may require product reformulation and supply chain modifications. The intensified regulatory framework has increased development costs and product launch timelines, benefiting companies with established compliance systems. While the FDA's classification of tampons as medical devices currently limits ingredient disclosure requirements, congressional and advocacy pressure is mounting for enhanced transparency and safety protocols. These regulatory changes influence product development strategies, particularly for established brands like Tampax, which must maintain consumer trust while adhering to evolving safety standards. Companies with comprehensive safety testing, supply chain monitoring, and quality control systems are better positioned to address these regulatory challenges, enhancing their market position. The increased regulatory oversight, while challenging, contributes to improved product safety and consumer confidence in the industry.

Other drivers and restraints analyzed in the detailed report include:

- Influence of social media diversifying product discovery

- Growing demand for sustainable and biodegradable products due to environmental concerns and shifting consumer preferences

- Environmental concerns regarding non-biodegradable wipes contributing to pollution and landfill issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The competitive landscape is transforming, with reusable alternatives gaining traction due to their superior long-term value propositions. Menstrual cups, for instance, are projected to grow at a 7.07% CAGR despite holding a smaller market share. In 2025, sanitary pads are expected to maintain a dominant 46.12% market share, supported by entrenched consumer habits and continuous advancements in materials and absorbency technologies. Innovations such as AI-powered smart sanitary pads are redefining traditional products by integrating health monitoring capabilities, offering added value beyond basic functionality. Conversely, tampons are experiencing declining popularity in certain regions. In the UK, sales have dropped as consumers shift toward menstrual cups and period underwear, driven by health and environmental concerns.

Emerging categories are bridging the gap between disposable and reusable options. Period panties and panty liners provide convenience while reducing environmental impact compared to traditional products. Growing awareness of pH balance and intimate health is driving demand for feminine wipes and intimate washes, although these products face increasing regulatory scrutiny over ingredient safety. Market diversification is evident in the "others" category, which includes intimate moisturizers and cleaning products, as brands expand their portfolios to encompass comprehensive intimate care solutions. The FDA's approval of innovative applications, such as Qvin's menstrual blood testing for health monitoring, highlights the convergence of feminine hygiene and digital health technologies. This development signals the creation of new product categories that extend beyond traditional absorption-focused solutions.

In 2025, consumer preferences for convenience are reflected in the 78.12% market share held by disposable products. However, reusable alternatives are gaining traction, achieving a robust 7.41% CAGR growth. This growth is driven by increasing sustainability concerns and the appeal of long-term cost savings. Technological advancements in materials science, such as antimicrobial fabrics and improved absorption capabilities, have addressed historical performance issues in the reusable segment. Additionally, consumer education initiatives are critical, as proper care and maintenance directly influence product longevity and user satisfaction. Inflationary pressures further strengthen the economic case for reusable products, as rising tampon prices make the higher upfront costs of cups and period underwear more attractive.

Manufacturers of disposable products are responding to sustainability demands by incorporating biodegradable materials and reducing packaging, aiming to balance environmental concerns with market retention. Institutions, particularly schools and public facilities adhering to menstrual equity mandates, favor disposable products due to hygiene protocols and maintenance requirements. Subscription models are emerging as a hybrid solution, combining the convenience of disposables with reduced packaging waste and predictable costs. Competitive dynamics are intensifying as reusable brands expand into retail channels traditionally dominated by disposables, prompting established manufacturers to develop dual-category strategies to remain competitive.

The Feminine Hygiene Market Report is Segmented by Product Type (Sanitary Pads/Napkins, Tampons, Menstrual Cups, Period Panties, and More), Product Category (Disposable Products, Reusable Products), Nature (Conventional and Natural/Organic), Distribution Channel (Supermarkets/Hypermarkets, Pharmacies/Drug Stores, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America holds the largest market share at approximately 36.60% as of 2025, supported by a well-established healthcare infrastructure and progressive menstrual equity policies that drive institutional demand, such as free product distribution programs in schools. The region's market maturity is reflected in consumer preferences for premium and sustainable products, bolstered by the strong presence of leading brands like Kotex and Tampax. The differing growth rates between Asia-Pacific and North America underscore the varying market dynamics, with North America focusing on innovation and sustainability, while Asia-Pacific prioritizes expanding access to basic products and enhancing affordability.

In comparison, Asia-Pacific is positioned as the fastest-growing region in the global feminine hygiene market, with a projected CAGR of approximately 6.54% through 2031. This growth is driven by improving economic conditions, government initiatives to enhance menstrual hygiene access, and efforts to foster cultural acceptance, particularly in high-population markets like India and China. Increased investments in awareness campaigns and menstrual hygiene education are accelerating product adoption, while urbanization and rising disposable incomes are enabling consumers to access a broader range of premium and innovative offerings. Regional players such as Prakati, Saathi, Eco Femme, and Anandi are capitalizing on this trend by introducing biodegradable and reusable feminine hygiene products, catering to the growing demand for environmentally friendly and health-conscious solutions.

Europe demonstrates steady market growth, driven by stringent environmental regulations favoring sustainable feminine hygiene products and robust healthcare systems that recognize menstrual health as a public health priority. South America shows potential for accelerated growth, supported by regional consolidation and the expansion of private labels, such as those in Colombia, which are optimizing distribution networks and improving cost efficiency. In the Middle East and Africa, increasing governmental and NGO-led initiatives are advancing menstrual hygiene education; however, cultural barriers and economic constraints continue to limit market penetration. Additionally, diverse regional regulatory frameworks, including tax exemptions in some markets and restrictions in others, significantly impact accessibility and affordability, shaping the global feminine hygiene market landscape.

- Procter & Gamble Company

- Unicharm Corporation

- Kenvue Inc.

- Kimberly-Clark Corporation

- Edgewell Personal Care Company

- Essity AB

- Kao Corporation

- Ontex Group

- TZMO Group

- Hengan Intl.

- Bodywise (UK) Ltd (Natracare)

- The Honey Pot Company

- Rael

- Premier FMCG Ltd (Lil-Lets Group)

- Urban Essentials India Pvt Ltd (Plush)

- Cora

- Prestige Consumer Healthcare Inc.

- Luna Daily

- Healthy HooHoo

- Maxim Hygiene

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising awareness and education about feminine hygiene and health

- 4.2.2 Increasing governmental and NGO initiatives promoting feminine hygiene awareness in developing regions

- 4.2.3 Influence of social media diversifying product discovery

- 4.2.4 Growing demand for sustainable and biodegradable products due to environmental concerns and shifting consumer preferences

- 4.2.5 Stricter mandates for ingredient disclosure and product labeling

- 4.2.6 Menstrual-equity mandates (free products in public spaces)

- 4.3 Market Restraints

- 4.3.1 Increasing regulation and scrutiny over personal care ingredients and claims

- 4.3.2 Environmental concerns regarding non-biodegradable wipes contributing to pollution and landfill issues

- 4.3.3 Cultural taboos and stigma surrounding menstruation

- 4.3.4 Upward pricing pressure and product affordability

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Sanitary Pads/Napkins

- 5.1.2 Tampons

- 5.1.3 Menstrual Cups

- 5.1.4 Period Panties

- 5.1.5 Panty Liners and Shields

- 5.1.6 Feminine Wipes and Intimate Washes

- 5.1.7 Others (Intimate moisturizers, Cleaning and deodorizing products)

- 5.2 By Product Category

- 5.2.1 Disposable Products

- 5.2.2 Reusable Products

- 5.3 By Nature

- 5.3.1 Conventional

- 5.3.2 Natural/Organic

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Pharmacies/Drug Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Procter & Gamble Company

- 6.4.2 Unicharm Corporation

- 6.4.3 Kenvue Inc.

- 6.4.4 Kimberly-Clark Corporation

- 6.4.5 Edgewell Personal Care Company

- 6.4.6 Essity AB

- 6.4.7 Kao Corporation

- 6.4.8 Ontex Group

- 6.4.9 TZMO Group

- 6.4.10 Hengan Intl.

- 6.4.11 Bodywise (UK) Ltd (Natracare)

- 6.4.12 The Honey Pot Company

- 6.4.13 Rael

- 6.4.14 Premier FMCG Ltd (Lil-Lets Group)

- 6.4.15 Urban Essentials India Pvt Ltd (Plush)

- 6.4.16 Cora

- 6.4.17 Prestige Consumer Healthcare Inc.

- 6.4.18 Luna Daily

- 6.4.19 Healthy HooHoo

- 6.4.20 Maxim Hygiene

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK