PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940713

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940713

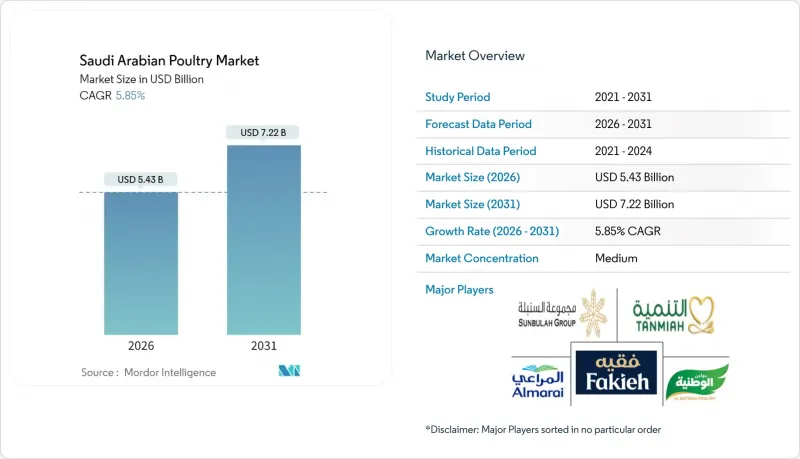

Saudi Arabian Poultry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Saudi Arabian Poultry Market was valued at USD 5.13 billion in 2025 and estimated to grow from USD 5.43 billion in 2026 to reach USD 7.22 billion by 2031, at a CAGR of 5.85% during the forecast period (2026-2031).

The Saudi Arabian poultry market is experiencing substantial growth driven by high poultry meat consumption among the country's predominantly Islamic population. In December 2024, Saudi Arabia's General Authority for Statistics (GASTAT) reported an annual poultry meat consumption of 43.40 kg per capita in the country. The market's expansion is further supported by increasing tourism, growth in the food service industry, evolving consumer preferences, and improved retail distribution networks. Furthermore, fast food chains like Al Baik, KFC, and Herfy are major contributors to this trend, as they rely heavily on processed poultry. Additionally, the growing influence of Western and international cuisines has led to an increased preference for processed chicken products like nuggets, and sausages are commonly found in supermarkets such as Danube and Carrefour. The rising demand for animal protein and consumer preference for low-fat, high-protein diets have significantly increased poultry meat consumption in Saudi Arabia. Market expansion is evidenced by recent developments, such as the February 2024 announcement by Meats & Cuts, a UAE-based artisan butcher shop and deli, to open 14 new branches across the GCC region. These developments have created new opportunities for both domestic and international players to enhance their market presence through innovative retail concepts and improved customer experiences.

Saudi Arabian Poultry Market Trends and Insights

Shift Toward Processed and Value-Added Products

The Kingdom's processed poultry segment is experiencing unprecedented transformation as manufacturers pivot from commodity production to value-engineered offerings. JBS's November 2024 launch of its USD 50 million Jeddah nugget facility exemplifies this shift, targeting the growing convenience food market while creating 500 specialized jobs. This strategic repositioning addresses the 25% annual growth in online grocery sales, where processed products command premium pricing and extended shelf life advantages. The Tyson-Tanmiah partnership's focus on doubling processed product capacity through advanced marination and tenderization technologies signals industry-wide recognition that value-addition drives margin expansion in an increasingly competitive landscape. Government incentives through the Agricultural Development Fund specifically target processing infrastructure, with Balady's SAR 1.14 billion expansion plan allocating 40% of investment toward processed product lines. The sector's evolution toward ready-to-cook and ready-to-eat formats aligns with demographic shifts, as 70% of the population under 35 prioritizes convenience over traditional preparation methods.

Expansion of Foodservice and QSR Chains

The foodservice sector's explosive growth creates structural demand shifts that fundamentally alter poultry consumption patterns across the Kingdom. Al Tazaj's expansion to 125 outlets across the MENA region, supported by Fakieh Poultry Farms' strategic 30% stake sale in December 2024, demonstrates how vertical integration between producers and QSR operators drives volume growth. The foodservice market's projected 10% annual growth through 2030 creates predictable demand streams that enable producers to optimize supply chain efficiency and product standardization. The sector benefits from tourism initiatives under Vision 2030, where international visitor growth drives demand for standardized, halal-certified poultry products across hotel and restaurant chains. QSR operators increasingly demand specialized cuts and portion sizes, pushing producers toward flexible manufacturing systems that can accommodate both retail and foodservice specifications.

Disease/Avian Influenza Risks

The Kingdom's poultry sector faces persistent biosecurity challenges, with avian encephalomyelitis virus outbreaks documented in the Eastern Province highlighting the ongoing disease management complexities. The global highly pathogenic avian influenza strategy for 2024-2033 emphasizes the critical need for enhanced surveillance and prevention measures, particularly relevant given Saudi Arabia's position as a major poultry importer from regions with documented HPAI cases. Biosecurity investments have intensified following international outbreaks, with producers implementing advanced monitoring systems and vaccination protocols that add 3-5% to production costs but provide essential protection against catastrophic losses. The sector's concentration among major producers creates systemic risks, where disease outbreaks at large facilities could significantly impact national supply chains and consumer confidence. Regulatory frameworks require continuous updates to address emerging pathogen threats, with the Saudi Food and Drug Authority implementing stringent import controls and domestic surveillance programs to maintain the Kingdom's disease-free status in key poultry segments.

Other drivers and restraints analyzed in the detailed report include:

- Government Support for Local Production

- Cultural Preference

- Environmental and Sustainability Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fresh/Chilled products command 55.08% market share in 2025, reflecting Saudi consumers' cultural preference for perceived quality and freshness over convenience Al Rajhi Capital. However, Canned products are experiencing the fastest growth at 7.21% CAGR through 2031, driven by expanding foodservice demand and shelf-life advantages in the Kingdom's challenging climate conditions. In Saudi Arabia, consumers are increasingly purchasing pre-seasoned and marinated frozen poultry products. For instance, in February 2022, Seara introduced its 'Shawaya' Chicken at Gulfood 2022, representing a notable development in the frozen foods market. This marinated frozen chicken was designed for direct cooking from 'freezer to oven,'. The product range includes frozen marinated whole chicken in three regional flavors, along with a pre-marinated tender whole chicken option. Fresh/chilled poultry meat offers greater culinary flexibility compared to frozen products. Consumers can easily marinate, season, and cook fresh/chilled poultry meat, resulting in enhanced flavors and textures. Market players continue to enhance their market presence through vertical integration, sustainable practices, and advanced production methods. For instancem, in July 2024, Tanmiah, a prominent fresh chicken producer in Saudi Arabia, achieved the AA+ Rating from BRCGS, representing a significant milestone in food safety certification.

Canned poultry products are widely utilized due to their convenience and ready-to-use characteristics. These products, typically pre-cooked, eliminate the need for processes such as thawing, marinating, or cooking from raw. They can be directly incorporated into various dishes, including sandwiches, salads, soups, or stews, offering significant time and effort savings. Suppliers are introducing high-quality products, such as organic and free-range options, to meet the demand for premium ingredients. Examples include organic canned chicken breast, free-range canned duck legs, gourmet canned turkey breast, premium canned quail, and organic canned Cornish hen, which provide opportunities for enhanced culinary applications. For instance, Swanson White Premium Chunk Canned Chicken, manufactured by Campbell Soup Company, is 98% fat-free, gluten-free, contains 18 grams of protein per 4.5-ounce can and is produced without antibiotics or added MSG, is available through both physical retail outlets and online platforms across the market.

The Saudi Arabian Poultry Market is Segmented by Form (Canned, Fresh/Chilled, Frozen, Processed), Nature (Organic and Conventional), Distribution Channel (Off-Trade and On-Trade), and Region (Western Region, Northern Region, Southern Region, and Central Region). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Al-Watania Poultry

- Fakieh Group

- Almarai Company Limited

- Tanmiah Food Company

- Sunbulah Group

- Americana Group Inc

- ARASCO Foods (Entaj)

- Arabian Agricultural Services Company

- Al Ola Poultry

- The Savola Group

- Emirated Rawabi Group (Al Rawdah Foods)

- Al Jazeera Poultry

- Al Wadi Poultry

- Al Kabeer Group

- BRF KSA

- Rahima Poultry Farms

- Astra Farms

- Mayar Holding

- Addoha Polutry Company

- Alinma Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Toward Processed and Value-Added Products

- 4.2.2 Expansion of Foodservice and QSR Chains

- 4.2.3 Government Support for Local Production

- 4.2.4 Cultural Preference

- 4.2.5 Consumer Health Awareness

- 4.2.6 Innovation in Product Formats and Packaging

- 4.3 Market Restraints

- 4.3.1 Disease/Avian Influenza Risks

- 4.3.2 Consumer Shifts Toward Alternatives

- 4.3.3 Environmental and Sustainability Concerns

- 4.3.4 Feed Cost Volatility

- 4.4 Supply Chain Analysis

- 4.5 Regualtory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE and VOLUME)

- 5.1 By Form

- 5.1.1 Canned

- 5.1.2 Fresh/Chilled

- 5.1.3 Frozen

- 5.1.4 Processed

- 5.1.4.1 Deli Meats

- 5.1.4.2 Marinated/Tenders

- 5.1.4.3 Meatballs

- 5.1.4.4 Nuggets

- 5.1.4.5 Sausages

- 5.1.4.6 Other Processed Poultry

- 5.2 By Nature

- 5.2.1 Organic

- 5.2.2 Conventional

- 5.3 By Distribution Channel

- 5.3.1 Off-trade

- 5.3.1.1 Supermarkets/Hypermarkets

- 5.3.1.2 Convenience Stores

- 5.3.1.3 Online Retail Stores

- 5.3.1.4 Others

- 5.3.2 On-trade

- 5.3.1 Off-trade

- 5.4 By Region

- 5.4.1 Western Region

- 5.4.2 Northern Region

- 5.4.3 Southern Region

- 5.4.4 Central Region

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Al-Watania Poultry

- 6.4.2 Fakieh Group

- 6.4.3 Almarai Company Limited

- 6.4.4 Tanmiah Food Company

- 6.4.5 Sunbulah Group

- 6.4.6 Americana Group Inc

- 6.4.7 ARASCO Foods (Entaj)

- 6.4.8 Arabian Agricultural Services Company

- 6.4.9 Al Ola Poultry

- 6.4.10 The Savola Group

- 6.4.11 Emirated Rawabi Group (Al Rawdah Foods)

- 6.4.12 Al Jazeera Poultry

- 6.4.13 Al Wadi Poultry

- 6.4.14 Al Kabeer Group

- 6.4.15 BRF KSA

- 6.4.16 Rahima Poultry Farms

- 6.4.17 Astra Farms

- 6.4.18 Mayar Holding

- 6.4.19 Addoha Polutry Company

- 6.4.20 Alinma Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK