PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940811

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940811

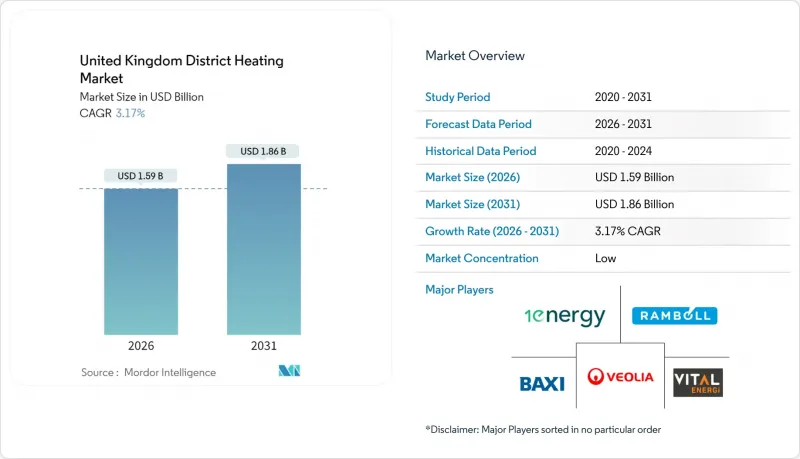

United Kingdom District Heating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The UK district heating market was valued at USD 1.54 billion in 2025 and estimated to grow from USD 1.59 billion in 2026 to reach USD 1.86 billion by 2031, at a CAGR of 3.17% during the forecast period (2026-2031).

This measured trajectory reflects the systemwide pivot from gas-dominant assets toward low-carbon heat pumps, waste-heat recovery, and large-scale thermal storage. Mandatory heat-network zoning is creating legally enforceable connection areas that de-risk customer acquisition, while the Green Heat Network Fund reduces capital outlay for projects integrating energy-from-waste heat or renewable electricity. Government grants now prioritize schemes delivering verifiable carbon cuts, prompting operators to blend river, mine-water, and wastewater heat with networked ground-source heat pumps. Investors are responding to these policy signals: institutional capital has intensified asset roll-ups that pool fragmented networks under professional management, accelerating technology upgrades such as 12-hour storage pits. Supply-chain constraints in skilled labour and metal commodities remain headwinds, yet Ofgem's incoming consumer-protection regime is expected to strengthen end-user confidence and encourage higher connection rates.

United Kingdom District Heating Market Trends and Insights

Statutory heat-network zoning from 2025-26

Heat-network zoning gives local authorities legal power to mandate customer connections within defined boundaries, securing the heat density essential for commercial viability. The Department for Energy Security and Net Zero released opportunity reports for 16 areas, guiding Birmingham, Leeds, and Newcastle to map mandatory zones that cover new builds and many retrofit sites. Zoning transforms district heating from an optional technology into a compliance obligation, lowering demand risk for operators and offering predictable revenue streams attractive to long-term investors. Developers gain clarity on network sizing and phased expansion, while existing building owners face clear deadlines to decarbonize. The policy, therefore, shifts market power toward network owners capable of rapid capital deployment and proven operational competence.

Green Heat Network Fund and HNES grants

The Green Heat Network Fund has disbursed more than GBP 380 million (USD 475 million) since launch, including GBP 19.5 million for Leeds's Aire Valley Heat and Power Network and GBP 7.2 million for the University of London's Bloomsbury Energy Network. Grants reduce the weighted average cost of capital, unlock large energy-from-waste heat sources, and improve internal rates of return by up to 2 percentage points. Award criteria reward projects that combine waste-heat capture with heat pumps, pushing market design toward hybrid configurations that can meet sub-50 gCO2/kWh targets. Funding certainty has also catalysed private lenders; several commercial banks now accept GHNF awards as de-risking instruments when structuring senior debt.

High front-end capex

Material inflation lifted insulation prices by 2-11.7% during 2024-2025, while copper and steel volatility added further strain to balance sheets. Arup estimates geothermal networks cost GBP 2-4 million per MWth, with drilling alone accounting for up to 45% of expenditure. The capital intensity lengthens payback horizons and limits bankability for smaller developers. GHNF grants soften but do not eliminate the risk of sunk costs during feasibility and permitting. Equity investors, therefore, demand higher internal returns, slowing financial close for projects without anchor loads or long-term heat-offtake agreements.

Other drivers and restraints analyzed in the detailed report include:

- Waste-heat capture mandate (EfW and sewage)

- Falling cost of river and mine-water heat pumps

- Gas-power price-spread volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential connections delivered 57.60% of UK district heating market share in 2025, benefiting from higher heat density in urban housing estates and mixed-use regeneration schemes. Social housing pilots underline the value proposition: the SHIELD trial indicates potential bill cuts of 40% for low-income tenants while meeting landlord retrofit obligations. Non-domestic demand is gaining momentum at 4.41% CAGR, driven by ESG imperatives and public-sector net-zero targets. Universities and hospitals, armed with capital grants and long asset-life planning horizons, now underwrite multi-megawatt expansions that lock in baseload demand.

Commercial property owners increasingly view heat networks as a hedge against future building-emissions taxes. Mandatory disclosure of operational carbon in leasing contracts pushes landlords toward networks that guarantee low-carbon coefficients. Meanwhile, local authorities bundle residential and municipal loads to unlock economies of scale, further widening the addressable base. The resulting blended customer mix stabilizes cash flows, positioning schemes for refinancing in private debt markets, and supporting the UK district heating market growth trajectory.

Gas-fired CHP retained 70.85% of UK district heating market size in 2025, though its dominance is eroding as carbon pricing and biomass-sustainability rules tighten. Low-carbon heat pumps and waste-heat systems expand at 5.08% CAGR, reflecting their eligibility for higher GHNF scoring and lower lifecycle emissions. The MEL Heat Network captures waste heat from the Millerhill Energy-from-Waste facility and boosts it with large heat pumps to serve Shawfair Town; Vattenfall calculates the hybrid system will avoid up to 90% of baseline emissions.

Ground-source configurations gain scale through networked arrays that share vertical boreholes across housing clusters, cutting per-dwelling drill costs by one-third. Air-source units increasingly act as summer top-up rather than sole supply, optimizing seasonal performance. Biomass remains niche in urban areas due to particulate limits, though rural estates still exploit local feedstock. Backup gas boilers persist for resilience, yet their runtime falls as storage and demand response improve.

The United Kingdom District Heating Market Report is Segmented by End User (Residential/Domestic, and Non-Domestic), Primary Heat Source (Gas-CHP, Low-Carbon HP and Waste-Heat, and More), Sector and Customer (Mixed-Use Regeneration District, Public and Social Housing, and More), Thermal-Storage Usage (No Integrated Storage, >=2 H Hot-Water Tanks, and >=12 H Pit/Tank Storage). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Vital Energi Utilities Ltd.

- 1Energy Group Ltd.

- Baxi Heating UK Ltd.

- Ramboll UK Ltd.

- Veolia Environnement SA

- Sweco UK Ltd.

- Vattenfall Heat UK Ltd.

- Equans Services Ltd.

- E.ON UK plc

- SSE Heat Networks Ltd.

- Metropolitan Infrastructure Ltd.

- ThamesWey Energy Ltd.

- Pinnacle Power Ltd.

- Fortum Carlisle Heat Networks Ltd.

- Cory Heat Networks Ltd.

- Kensa Utilities Ltd.

- Ener-Vate Ltd.

- Centrica Business Solutions UK Ltd.

- ENGIE (Energy Solutions UK) Ltd.

- Danpower UK Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Statutory heat-network zoning from 2025-26

- 4.2.2 Green Heat Network Fund and HNES grants

- 4.2.3 Waste-heat capture mandate (EfW and sewage)

- 4.2.4 Falling cost of river/mine-water heat pumps

- 4.2.5 Mandatory landlord tariff disclosure

- 4.2.6 Aggregation of thermal storage into ESO flexibility

- 4.3 Market Restraints

- 4.3.1 High front-end capex

- 4.3.2 Gas-power price-spread volatility

- 4.3.3 Skilled-labour shortage (pipe-welders/HIU)

- 4.3.4 Consumer "monopoly billing" perception

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter"s Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By End User

- 5.1.1 Residential / Domestic

- 5.1.2 Non-domestic

- 5.2 By Primary Heat Source

- 5.2.1 Gas-CHP

- 5.2.2 Low-carbon HP and Waste-heat

- 5.2.3 Biomass / Biogas

- 5.2.4 Other back-up (gas, electric)

- 5.3 By Sector and Customer

- 5.3.1 Mixed-use regeneration districts

- 5.3.2 Public and Social Housing

- 5.3.3 Universities and Hospitals

- 5.3.4 Commercial / Retail Parks

- 5.4 By Thermal-Storage Usage

- 5.4.1 No integrated storage

- 5.4.2 >=2 h hot-water tanks

- 5.4.3 >=12 h pit / tank storage

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Vital Energi Utilities Ltd.

- 6.4.2 1Energy Group Ltd.

- 6.4.3 Baxi Heating UK Ltd.

- 6.4.4 Ramboll UK Ltd.

- 6.4.5 Veolia Environnement SA

- 6.4.6 Sweco UK Ltd.

- 6.4.7 Vattenfall Heat UK Ltd.

- 6.4.8 Equans Services Ltd.

- 6.4.9 E.ON UK plc

- 6.4.10 SSE Heat Networks Ltd.

- 6.4.11 Metropolitan Infrastructure Ltd.

- 6.4.12 ThamesWey Energy Ltd.

- 6.4.13 Pinnacle Power Ltd.

- 6.4.14 Fortum Carlisle Heat Networks Ltd.

- 6.4.15 Cory Heat Networks Ltd.

- 6.4.16 Kensa Utilities Ltd.

- 6.4.17 Ener-Vate Ltd.

- 6.4.18 Centrica Business Solutions UK Ltd.

- 6.4.19 ENGIE (Energy Solutions UK) Ltd.

- 6.4.20 Danpower UK Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment