PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940844

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940844

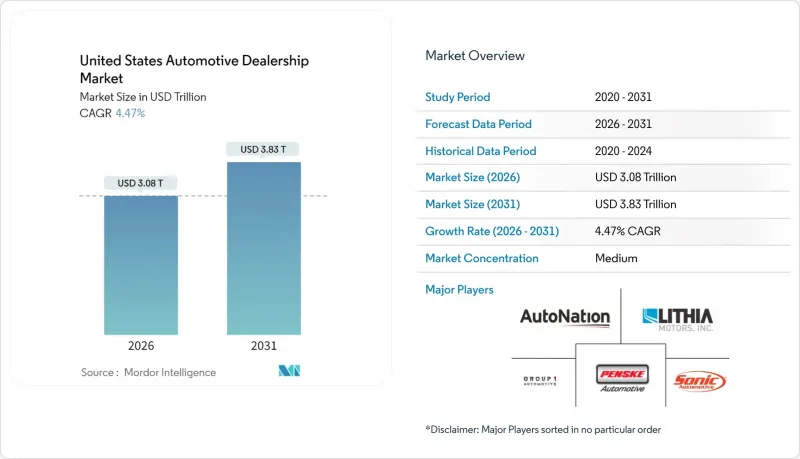

United States Automotive Dealership - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States automotive dealership market is expected to grow from USD 2.95 trillion in 2025 to USD 3.08 trillion in 2026 and is forecast to reach USD 3.83 trillion by 2031 at 4.47% CAGR over 2026-2031.

Well-balanced inventories, surging certified pre-owned (CPO) demand, and heavy electrification investments are underpinning steady revenue gains even as online price transparency squeezes gross margins. Dealer-led expansion of finance and insurance (F&I) portfolios is offsetting pressure on front-end profitability, while favorable state legislation is accelerating digital retail adoption. Rising medium and heavy-commercial-vehicle sales tied to fleet electrification offer an incremental profit pool, and sustained consumer preference for light trucks and SUVs continues to lift average transaction values. At the same time, substantial capital requirements for EV-ready service bays and over-the-air (OTA) software capability are widening the competitive gap between well-funded consolidators and under-capitalized independents.

United States Automotive Dealership Market Trends and Insights

Accelerating EV Model Launches

Franchise groups have pledged billions for EV-ready showrooms and service bays . Capital outlays per location range from USD 100,000 for Level 2 chargers to more than USD 1 million, where Level 3 DC fast-charging plus utility upgrades are required. Ford's Model e Certified Elite program illustrates OEM mandates that bundle training, tooling, and charger installation under strict timelines, reshaping cap-ex planning cycles for retailers. Early movers capture incremental service profits from battery warranty work and software-subscription enablement, offsetting EVs' lower mechanical-repair frequency. Geographic disparity persists; dealers in California and New York see higher charger utilization than peers in the Upper Midwest, yet nationwide EV registration growth in 2024 supports long-run investment viability.

Recovery in New-Vehicle Inventory Levels

OEM production stability lifted dealer stock to 3.23 million units by November 2024, close to the 3.4 - 3.5 million pre-pandemic norm. Improved supply lets retailers restore traditional incentive programs and recoup volume-based bonuses, reversing two years of margin erosion caused by constrained pipelines. Domestic brands, supported by normalized chip supply, re-establish competitive lease offers that draw payment-sensitive buyers back to showrooms. Dealers must manage slower turn-rates than in 2022's shortage era, prompting heavier reliance on AI-driven demand-forecasting engines to avoid over-stocking. Robust inventory also strengthens the negotiating power of large dealer groups, who can bulk-purchase allocations, widening their cost advantage over smaller independents.

High CAPEX for EV and ADAS Service Upgrades

EV battery hoists, insulated storage, and ADAS calibration rigs cost USD 56,000-650,000 per rooftop . Access to affordable power feeds and specialized technicians is especially constrained in rural markets, forcing some single-point operators to exit instead of refinancing aging facilities. Consolidators enjoy scale cost leverage and can amortize tooling over larger throughput, widening their variable-cost gap. OEM reimbursement programs partially defray expenses but usually require volume commitments, embedding further consolidation incentives. Consequently, capital intensity is the most immediate structural headwind for independents, lowering market-wide growth by an estimated 0.6 percentage points.

Other drivers and restraints analyzed in the detailed report include:

- Dealer-Led Expansion of F&I Products

- Growth of Certified Pre-Owned (CPO) Programs

- OEM Direct-to-Consumer Models

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The United States automotive dealership market size for used vehicles held a 52.85% share in 2025, cementing its role as the channel's economic backbone. Elevated residual values, bolstered by curtailed lease returns, helped dealers protect grosses even as wholesale indices normalized. Margins continue to benefit from private-party acquisition tools that circumvent auction fees and reduce inbound logistics costs. Certified tiers maintain premium pricing and 25% faster turn-rates, improving cash velocity that supports floorplan interest outlays.

New vehicles are projected to log a 5.41% CAGR, outpacing used growth through 2031 as OEM production constraints fade. Incentives averaging 6.8% of transaction price in early 2025 have pulled sidelined buyers back into showrooms, especially on entry-level trims. As supply normalizes, the United States automotive dealership market share for new vehicles is expected to climb modestly, though pricing transparency and agency pilots will cap front-end gross upside. Dealers tighten reconditioning cycles on trade-ins, aiming to flip used inventory within 27 days versus the 35-day industry median, sustaining blended gross performance across both vehicle streams.

Franchised groups controlled 57.60% of the United States automotive dealership market in 2025, and direct-to-consumer digital platforms record the highest forecast CAGR at 6.02% to 2031, underpinned by exclusive OEM allocations, warranty authority, and financing captive ties that erect high entry barriers. Market consolidators leverage acquisition synergies such as Lithia's economies in procurement and marketing to expand EBITDA per rooftop. Digital pure-plays leverage asset-light models, booking double-digit unit gains despite narrow contribution margins. Still, omnichannel hybrids are emerging, with Amazon Autos integrating dealer fulfillment to keep last-mile logistics cost-effective while preserving consumer convenience.

Independent lots retain relevance where price-sensitive shoppers value negotiation flexibility and non-OEM warranty bundles. Yet franchise operators' mandated EV tooling and OTA software rights grant them a structural advantage in an electrified future. Over time, the United States automotive dealership market size is expected to skew toward high-performing multi-state groups as succession planning and capital intensity prompt single-store owners to divest. Franchisees that invest in click-to-buy platforms and same-day service lanes will outperform peers relying solely on legacy walk-in traffic.

The United States Automotive Dealership Market Report is Segmented by Type (New-Vehicle Sales and Used-Vehicle Sales), Retailer (Franchised Dealers, Independent Dealers, and More), Vehicle Type (Passenger Cars, Light Trucks and SUVs, and More), Sales Channel (Brick and Mortar, Online/Omnichannel), Customer Segment, and Region. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- AutoNation Inc.

- Lithia Motors Inc.

- Penske Automotive Group

- Group 1 Automotive Inc.

- Sonic Automotive Inc.

- Asbury Automotive Group Inc.

- Hendrick Automotive Group

- CarMax Inc.

- Carvana Co.

- Larry H. Miller Dealerships

- Ken Garff Automotive Group

- Staluppi Auto Group

- Morgan Auto Group

- Holman Automotive

- Serra Automotive

- Napleton Automotive Group

- Suburban Collection

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating EV Model Launches

- 4.2.2 Recovery in New-Vehicle Inventory Levels

- 4.2.3 Dealer-Led Expansion of F&I Products

- 4.2.4 Growth of Certified Pre-Owned (CPO) Programs

- 4.2.5 State-Level Digital Retailing Legislation

- 4.2.6 OEM Subscription Models via Dealers

- 4.3 Market Restraints

- 4.3.1 High CAPEX for EV and ADAS Service Upgrades

- 4.3.2 OEM Direct-to-Consumer Models

- 4.3.3 Margin Compression from Online Price Transparency

- 4.3.4 Increased FTC Compliance Costs (F&I)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Type

- 5.1.1 New-Vehicle Sales

- 5.1.2 Used-Vehicle Sales

- 5.2 By Retailer

- 5.2.1 Franchised Dealers

- 5.2.2 Independent Dealers

- 5.2.3 Direct-to-Consumer Digital Retailers

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Trucks and SUVs

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.4 By Sales Channel

- 5.4.1 Brick and Mortar

- 5.4.2 Online / Omnichannel

- 5.5 By Customer Segment

- 5.5.1 Individual Consumers

- 5.5.2 Fleet and Corporate

- 5.6 By Region (United States)

- 5.6.1 Northeast

- 5.6.2 Midwest

- 5.6.3 South

- 5.6.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 AutoNation Inc.

- 6.4.2 Lithia Motors Inc.

- 6.4.3 Penske Automotive Group

- 6.4.4 Group 1 Automotive Inc.

- 6.4.5 Sonic Automotive Inc.

- 6.4.6 Asbury Automotive Group Inc.

- 6.4.7 Hendrick Automotive Group

- 6.4.8 CarMax Inc.

- 6.4.9 Carvana Co.

- 6.4.10 Larry H. Miller Dealerships

- 6.4.11 Ken Garff Automotive Group

- 6.4.12 Staluppi Auto Group

- 6.4.13 Morgan Auto Group

- 6.4.14 Holman Automotive

- 6.4.15 Serra Automotive

- 6.4.16 Napleton Automotive Group

- 6.4.17 Suburban Collection

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment