PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940894

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940894

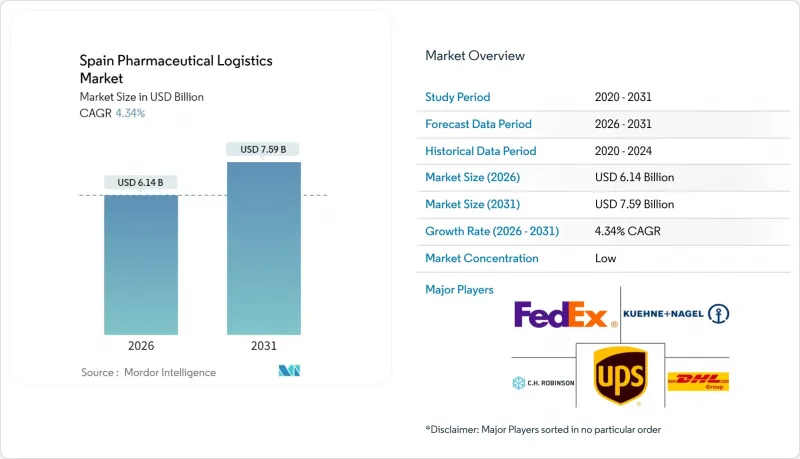

Spain Pharmaceutical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Spain Pharmaceutical Logistics Market size in 2026 is estimated at USD 6.14 billion, growing from 2025 value of USD 5.88 billion with 2031 projections showing USD 7.59 billion, growing at 4.34% CAGR over 2026-2031.

Robust motorway, port, and airport capacity positions Spain as a Southern European gateway that reduces lead times for temperature-sensitive medicines and heightens demand for end-to-end visibility tools. Logistic parks clustered along the Mediterranean and Atlantic corridors speed cross-border flows into France and Italy, which is critical as 80% of European medicines now require temperature control. Regulatory reforms around GDP certification tighten quality thresholds and reward operators with automated monitoring systems. Competitive intensity is rising because global leaders are injecting billions into Spanish capacity, accelerating technology adoption, and sparking consolidation.

Spain Pharmaceutical Logistics Market Trends and Insights

Rising Domestic Pharmaceutical Sales Volume

Annual domestic drug revenue exceeds EUR 23 billion (USD 25 billion) and supports more than 260,000 jobs, which strengthens the baseline for logistics growth. Public health spending at EUR 134 billion (USD 143 billion) creates dependable demand across the Spanish pharmaceutical logistics market. Per-capita medicine outlays at EUR 477 (USD 510) surpass European averages, reinforcing volume stability. Yet drug shortages jumped 41% in 2024, with 4,983 items affected, exposing vulnerabilities in replenishment cycles. January 2024 recorded 947 unavailable products, underscoring the need for predictive inventory tools that reduce cascading care disruptions.

Ageing Population & Chronic Disease Burden Intensifying Last-Mile Demand

Long-term demographic projections show a sharply rising proportion of citizens older than 65 by 2074. Chronic illnesses shift dispensing patterns toward repeat prescriptions delivered to patients' homes, which magnifies last-mile complexity within Spain pharmaceutical logistics market. Digital health platforms integrate telemedicine with pharmacy networks and require timed deliveries of cardiovascular and diabetes drugs. Generic penetration led by Kern Pharma and Teva supports affordability but raises shipment frequency. Personalized oncology regimens from PharmaMar demand traceable, patient-specific cold-chain movements that extend beyond hospital pharmacies into home-care settings.

Driver Shortage & Escalating Labour Costs

Cold-chain operators represent 2.5% of Iberian food GDP and face acute driver shortages that inflate wage bills. DHL answered with a EUR 2 billion (USD 2.08 billion) health-logistics program that prioritizes automation to counter labor gaps. UPS seeks to double healthcare revenue to USD 20 billion by 2026, banking on robotics and routing software to lift productivity. Despite capital injections, immediate driver scarcity restricts capacity during influenza vaccine peaks, restraining Spain pharmaceutical logistics market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Biologics & Temperature-Sensitive Therapies

- EU Falsified Medicines Directive Serialization Deadline Enforcement

- Rising Energy Costs Impacting Refrigerated-Warehouse Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation captured 59.30% of Spain pharmaceutical logistics market share in 2025, propelled by 15,825 km of motorways connecting ports at Barcelona, Valencia, and Algeciras. This backbone delivers medicines to 200,000 European points of sale through networks managed by Logista and DHL. Road haulage remains the preferred mode for its overnight reach, but airfreight is scaling via Girona and Zaragoza airports to meet urgent biologic demand. Sea and rail corridors increasingly attract shippers pursuing carbon-reduction targets, with CEVA citing 70% lower emissions for refrigerated sea lanes. Value-added services & others are expected to post a 4.66% CAGR to 2031 as GDP documentation, kitting, and late-stage customization become standard contract inclusions. FedEx secured a CEIV Pharma Corporate Certificate in 2025 and won USD 400 million in healthcare contracts, illustrating the commercial payoff from compliance excellence.

Spain pharmaceutical logistics market size for value-added services & others is forecast to rise, aligned with expanding outsourcing by Spanish hospitals. The modal mix will tilt toward temperature-controlled containers that embed IoT sensors, creating data streams monetized through predictive lane validation services. UPS's integration of Frigo-Trans and BPL widens its European 2-8 °C footprint and offers Spanish pharma exporters a single invoice solution spanning road, sea and air. Sustainability is another driver, with electric trucks now servicing inner-city clinics in Madrid under CEVA's FORPLANET label, reducing emissions by 26,000 tons in 2024.

The Spain Pharmaceutical Logistics Market Report is Segmented by Service Type (Transportation, Warehousing & Storage, and Value-Added Services & Others), Mode of Operation (Cold-Chain Logistics and Non-Cold-Chain Logistics), Product Type (Prescription Drugs, OTC Drugs, Biologics & Biosimilars, Vaccines & Blood Products, Cell & Gene Therapies, Veterinary Medicine, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- DHL Supply Chain Spain

- FedEx Express

- Kuehne + Nagel S.A.

- United Parcel Service (UPS)

- C.H. Robinson

- CEVA Logistics

- DSV

- Movianto

- Eurotranspharma

- Primafrio

- Cencora

- Yusen Logistics (Part of NYK Line)

- Scan Global Logistics

- Rhenus Logistics

- Geodis

- TIBA

- Logista Pharma

- Noatum Logistics

- Ibercondor

- Logisber

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising domestic pharmaceutical sales volume

- 4.2.2 Ageing population & chronic disease burden intensifying last-mile demand

- 4.2.3 Expansion of biologics & temperature-sensitive therapies

- 4.2.4 EU Falsified Medicines Directive serialization deadline enforcement

- 4.2.5 RRF-backed cold-chain infrastructure investments

- 4.2.6 Hospital network shift toward outsourced supply models

- 4.3 Market Restraints

- 4.3.1 Driver shortage & escalating labour costs

- 4.3.2 Ensuring end-to-end temperature integrity amid climate extremes

- 4.3.3 Fragmented cold-storage real-estate ownership

- 4.3.4 Rising energy costs impacting refrigerated-warehouse margins

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geopolitics & Pandemic on the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road Freight

- 5.1.1.2 Air Freight

- 5.1.1.3 Sea Freight

- 5.1.1.4 Rail Freight

- 5.1.2 Warehousing & Storage

- 5.1.3 Value-added Services and Others

- 5.1.1 Transportation

- 5.2 By Mode of Operation

- 5.2.1 Cold-Chain Logistics

- 5.2.2 Non-Cold-Chain Logistics

- 5.3 By Product Type

- 5.3.1 Prescription Drugs

- 5.3.2 OTC Drugs

- 5.3.3 Biologics & Biosimilars

- 5.3.4 Vaccines & Blood Products

- 5.3.5 Clinical Trail Materials

- 5.3.6 Cell & Gene Therapies

- 5.3.7 Medical Devices & Diagnostics

- 5.3.8 Veterinary Medicine

- 5.3.9 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Supply Chain Spain

- 6.4.2 FedEx Express

- 6.4.3 Kuehne + Nagel S.A.

- 6.4.4 United Parcel Service (UPS)

- 6.4.5 C.H. Robinson

- 6.4.6 CEVA Logistics

- 6.4.7 DSV

- 6.4.8 Movianto

- 6.4.9 Eurotranspharma

- 6.4.10 Primafrio

- 6.4.11 Cencora

- 6.4.12 Yusen Logistics (Part of NYK Line)

- 6.4.13 Scan Global Logistics

- 6.4.14 Rhenus Logistics

- 6.4.15 Geodis

- 6.4.16 TIBA

- 6.4.17 Logista Pharma

- 6.4.18 Noatum Logistics

- 6.4.19 Ibercondor

- 6.4.20 Logisber

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment