PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940898

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1940898

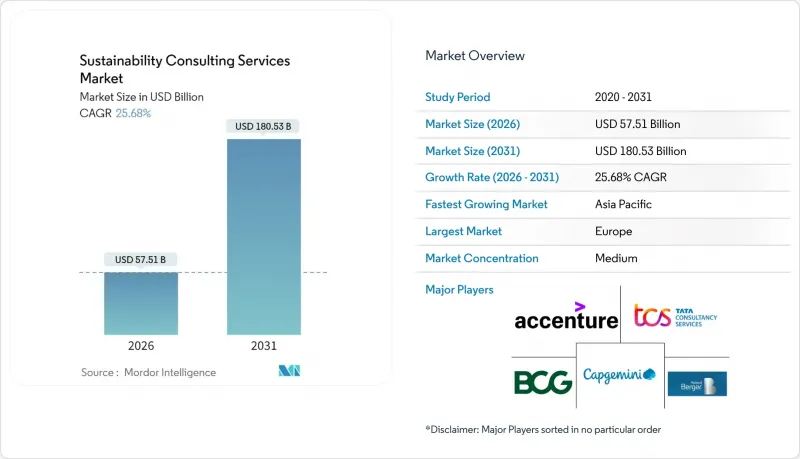

Sustainability Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The sustainability consulting services market was valued at USD 45.75 billion in 2025 and estimated to grow from USD 57.51 billion in 2026 to reach USD 180.53 billion by 2031, at a CAGR of 25.68% during the forecast period (2026-2031).

Heightened regulatory mandates, fast-rising corporate net-zero pledges and digital carbon-data platforms are turning environmental, social and governance management into a board-level priority. The European Union's Corporate Sustainability Reporting Directive alone brings more than 50,000 firms into mandatory disclosure scope, multiplying demand for specialized guidance. At the same time, investors are reallocating capital toward climate-aligned assets, prompting companies to seek external verification of decarbonization plans. Technology adoption is reshaping service delivery as AI-enabled carbon-accounting engines automate data capture, freeing consultants to focus on high-value advisory. Competition is intensifying, yet the market remains sufficiently fragmented for both global majors and niche boutiques to capture share in emerging areas such as biodiversity, circularity and nature-based solutions.

Global Sustainability Consulting Services Market Trends and Insights

Corporate Net-Zero Commitments Accelerating Advisory Spend

Large enterprises now treat net-zero targets as hard compliance deadlines rather than aspirational statements. Boards must translate science-based targets into operational roadmaps that span supply-chain mapping, technology selection and stakeholder engagement. Scope 3 emissions regularly exceed 70% of total footprints, amplifying complexity and elevating the need for third-party guidance. Only 16% of the world's 2,000 largest firms remain on track for 2050 net-zero, underscoring a vast execution gap that external advisors are hired to close . Continuous monitoring, target recalibration and assurance requirements sustain multi-year consulting engagements as regulations tighten and methodologies evolve.

Expanding ESG and Sustainability Disclosure Regulations

The EU CSRD introduces double materiality analysis, structured digital tagging and third-party assurance, creating a steep learning curve for companies with European operations. Staggered adoption timelines from 2024 to 2026 keep advisory demand elevated across successive cohorts of filers. Non-EU multinationals with significant regional sales also fall within scope, extending compliance projects worldwide. Required data-collection depth forces upgrades to reporting processes, IT systems and internal controls, areas where consultancies provide assessment, design and change-management services.

Acute Talent Shortage Inflating Billing Rates

Demand for professionals who blend climate science, regulatory insight and strategic consulting far outweighs supply. Specialized roles in biodiversity valuation, circular-product design and AI-driven emissions analytics remain especially scarce. Firms raise compensation, poach competitors and invest in upskilling programs, yet pipeline constraints persist. Elevated day rates deter some midmarket clients, dampening project volumes and placing a natural brake on the sustainability consulting services market. Technology-enabled delivery models partly offset the shortfall, but complex engagements still require human expertise.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Carbon-Accounting Platforms Driving Integration Projects

- Public-Sector Decarbonization Stimulus Programs

- Off-the-Shelf SaaS Sustainability Tools Disintermediating Consulting

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Climate-change consulting accounted for 29.12% of 2025 revenue within the sustainability consulting services market. Circular-economy and resource-efficiency engagements, though smaller, will post the strongest 18.05% CAGR to 2031, reflecting growing corporate interest in waste elimination and regenerative design. ESG-reporting advisory gains traction as disclosure obligations expand, while green-building consulting benefits from stricter codes and certification schemes.

Clients pursuing circular-economy strategies demand product redesign, reverse-logistics planning and new revenue-model development. Advisory teams integrate life-cycle assessment tools with financial-impact modeling to guide decision-making. As material costs rise and landfill regulations tighten, leaders view circularity as both risk mitigation and value creation, reinforcing long-run expansion of the sustainability consulting services market.

Energy and power companies generated 23.78% of 2025 spending, underscoring the sector's central role in global decarbonization. Manufacturers, however, will pace growth at a 15.74% CAGR as supply-chain mandates propagate and Industry 4.0 investments intersect with resource-efficiency goals. Financial-services clients request climate-risk scenario analysis and sustainable-finance product design, while construction and real estate engagements revolve around green-building codes and embodied-carbon tracking.

Manufacturers face mounting pressure to report scope-3 emissions, comply with customer-driven supplier codes and reduce energy intensity. Consulting assignments span material-flow mapping, renewable-energy sourcing and digital twin deployment. As regulatory and commercial drivers converge, industrial clients contribute an ever-larger slice of the sustainability consulting services market size.

Sustainability Consulting Services Market is Segmented by Service Type (Climate-Change Consulting, Green-Building Consulting, and More), End-User Industry (Energy and Power, Construction and Real Estate, and More), Consulting Delivery Model (Strategy and Advisory, and More), Sustainability Focus Area (Climate-Change and Net-Zero, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe generated 38.74% of 2025 revenue, reflecting early regulatory adoption and mature corporate sustainability practices. The CSRD, EU Taxonomy and national climate-neutrality laws sustain multiyear advisory pipelines. German federal agencies, for instance, enlist consultants to draft sector-specific decarbonization roadmaps and monitor progress toward the 2045 neutrality goal. Complex double-materiality assessments and digital tagging rules reinforce demand for integrated legal, financial, and technical expertise.

Asia-Pacific will deliver the fastest 16.92% CAGR to 2031. Industrialization, supply-chain export exposure and sovereign-wealth-fund mandates converge to spur consulting spend. Nations such as China and India launch emissions-trading pilots and green-finance frameworks, compelling domestic firms to seek guidance on compliance and opportunity capture. BloombergNEF projects the region needs USD 74-89 trillion in transition capital through 2050, anchoring a sizeable sustainability consulting services market. Service providers that localize offerings while leveraging global playbooks are best positioned.

North America remains sizeable though maturing. Voluntary corporate commitments, state-level clean-energy standards and investor activism underpin steady growth, yet lack of comprehensive federal regulation tempers acceleration. South American demand is emerging as multinational supply-chain requirements extend downstream, whereas the Middle East and Africa benefit from resource-sector diversification agendas and sovereign-fund ESG goals. Varied policy maturity across geographies ensures differentiated service mixes, bolstering global resilience of the sustainability consulting services market.

- Accenture plc

- Boston Consulting Group, Inc.

- Tata Consultancy Services Ltd.

- Capgemini SE

- Roland Berger GmbH

- Bain and Company, Inc.

- KPMG International Ltd.

- Ernst and Young Global Ltd.

- Deloitte Touche Tohmatsu Ltd.

- PricewaterhouseCoopers LLP

- McKinsey and Company, Inc.

- AECOM

- WSP Global Inc.

- Environmental Resources Management Ltd.

- Jacobs Solutions Inc.

- Arcadis N.V.

- Wood Group plc

- Tetra Tech, Inc.

- Ramboll Group A/S

- Stantec Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Corporate net-zero commitments accelerating advisory spend

- 4.2.2 Expanding ESG and sustainability disclosure regulations (e.g., CSRD)

- 4.2.3 Investor pressure for climate-risk-aligned capital allocation

- 4.2.4 Public-sector decarbonization stimulus programs

- 4.2.5 AI-enabled carbon-accounting platforms driving integration projects

- 4.2.6 Sovereign-wealth-fund sustainability mandates in emerging markets

- 4.3 Market Restraints

- 4.3.1 Acute talent shortage inflating billing rates

- 4.3.2 Regulatory-certainty gaps and greenwashing litigation risk

- 4.3.3 Off-the-shelf SaaS sustainability tools disintermediating consulting

- 4.3.4 Carbon-credit price volatility undermining ROI narratives

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Industry Ecosystem Analysis

- 4.9 Key Use Cases and Case Studies

- 4.10 Assessment of Macroeconomic Trends

- 4.11 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Climate-Change Consulting

- 5.1.2 Green-Building Consulting

- 5.1.3 ESG and Reporting Advisory

- 5.1.4 Circular-Economy and Resource-Efficiency Consulting

- 5.1.5 Sustainability Strategy and Governance

- 5.2 By End-User Industry

- 5.2.1 Energy and Power

- 5.2.2 Construction and Real Estate

- 5.2.3 Manufacturing and Industrials

- 5.2.4 Financial Services and Insurance

- 5.2.5 Public Sector and NGOs

- 5.3 By Consulting Delivery Model

- 5.3.1 Strategy and Advisory

- 5.3.2 Implementation and Integration

- 5.3.3 Managed Services / Outsourcing

- 5.3.4 Digital Platforms and Analytics

- 5.3.5 Training and Capacity-Building

- 5.4 By Sustainability Focus Area

- 5.4.1 Climate-Change and Net-Zero

- 5.4.2 Biodiversity and Nature-Based Solutions

- 5.4.3 Circular-Economy and Waste-Management

- 5.4.4 Social Impact and DEI

- 5.4.5 Sustainable Finance and Reporting

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Colombia

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Singapore

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Boston Consulting Group, Inc.

- 6.4.3 Tata Consultancy Services Ltd.

- 6.4.4 Capgemini SE

- 6.4.5 Roland Berger GmbH

- 6.4.6 Bain and Company, Inc.

- 6.4.7 KPMG International Ltd.

- 6.4.8 Ernst and Young Global Ltd.

- 6.4.9 Deloitte Touche Tohmatsu Ltd.

- 6.4.10 PricewaterhouseCoopers LLP

- 6.4.11 McKinsey and Company, Inc.

- 6.4.12 AECOM

- 6.4.13 WSP Global Inc.

- 6.4.14 Environmental Resources Management Ltd.

- 6.4.15 Jacobs Solutions Inc.

- 6.4.16 Arcadis N.V.

- 6.4.17 Wood Group plc

- 6.4.18 Tetra Tech, Inc.

- 6.4.19 Ramboll Group A/S

- 6.4.20 Stantec Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment