PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034989

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2034989

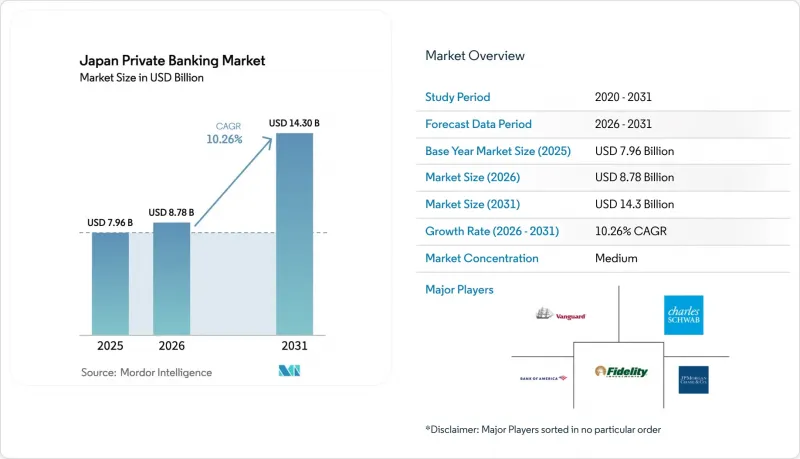

Japan Private Banking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan private banking market size is expected to grow from USD 7.96 billion in 2025 to USD 8.78 billion in 2026 and is forecast to reach USD 14.3 billion by 2031 at 10.26% CAGR over 2026-2031.

This expansion is fueled by the country's unprecedented inter-generational wealth transfer, incremental deregulation of fiduciary services, intensifying digital innovation, and rising equity valuations that swell investable assets. Scale advantages held by the largest domestic trust banks, rising demand for holistic succession solutions, and the rapid emergence of API-enabled advisory platforms are amplifying competitive intensity. Simultaneously, foreign houses are enlarging on-shore desks to serve ultra-high-net-worth (UHNW) clients who seek cross-border diversification, while domestic banks deepen fee-based revenue streams to offset margin pressure. Structural opportunities remain concentrated in wealth succession, discretionary mandates, and digital advisory tools that broaden access to specialist products.

Japan Private Banking Market Trends and Insights

Aging Population Wealth Transfer

Japan's demographic transition is creating the world's largest intergenerational wealth transfer event, with USD 2.21 trillion (Yen330 trillion) in assets expected to change hands by 2030 as baby boomers pass wealth to younger generations. This transfer represents approximately 60% of Japan's GDP and is concentrated among households with investable assets exceeding USD 670,000 (Yen100 million), creating a natural client base for private banking services. The complexity of Japan's inheritance tax system, which imposes rates up to 55% on estates exceeding USD 4.02 million (Yen600 million), is driving demand for sophisticated tax planning and trust structures. Recent legislative changes extending the inheritance tax clawback period from 3 to 7 years for overseas residents further amplifies the need for professional wealth structuring services. Cultural shifts are equally significant, with Nomura Research Institute data showing that 64.6% of business heirs have no intention of taking over family enterprises, necessitating alternative succession strategies through private banking channels.

Deregulation of Fiduciary Services Under Japan's Stewardship Code

The Financial Services Agency's 2024 amendments to Japan's Stewardship Code are dismantling traditional barriers between asset management and advisory services, enabling private banks to offer more integrated wealth solutions. These reforms allow institutions to provide discretionary investment management alongside traditional banking services, creating new revenue streams and improving client outcomes through holistic portfolio management. The deregulation particularly benefits trust banks like Sumitomo Mitsui Trust, which can now leverage their fiduciary expertise across broader client segments without regulatory constraints. Early adoption metrics show discretionary mandate growth of 23% year-over-year among major private banks in 2024, with average fee compression of 15 basis points as competition intensifies. This regulatory evolution aligns Japan with global best practices in wealth management while maintaining robust investor protection standards through enhanced disclosure requirements.

Low Interest-Rate Environment

The Bank of Japan's March 2024 policy lift to 0.1% concluded an era of negative rates, yet margins remain historically compressed. This environment particularly challenges smaller regional private banks that lack scale in advisory services, with average NIMs declining to 0.85% in 2024 from 1.2% in 2019 across the sector. The constraint is driving strategic pivots toward wealth management fees, with leading institutions targeting fee income ratios of 35-40% by 2030 compared to the current 25% average. Regulatory compliance factors under the Financial Instruments and Exchange Act require enhanced disclosure of fee structures, creating transparency that benefits clients but pressures institutional margins during the transition period.

Other drivers and restraints analyzed in the detailed report include:

- Digital Transformation of Wealth Platforms (APIs, Robo-Advisory)

- Rising Stock-Market Valuation Spurring Affluent Asset Growth

- Basel III Capital Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Trust Service held 23.89% of the Japan private banking market in 2025, underpinned by the nation's complex inheritance taxes and a legal culture that favors trust structures for asset continuity. Integration of portfolio management with trust administration has improved relationship depth and share-of-wallet among multi-generational families. Real Estate Consulting, while accounting for a smaller base, is projected to register the fastest 8.22% CAGR as tokenization of metropolitan properties and REIT-linked offerings democratize access to prime assets. The Japan private banking market size for real-estate-focused mandates is accelerating as blockchain platforms open fractional ownership opportunities to mass affluent investors. Insurance Service, backed by bancassurance tie-ups, commands 17.62% revenue through capital-protected wrappers popular among risk-averse seniors. Tax Consulting expands at 8.05% CAGR, driven by cross-border financial complexity as affluent households diversify overseas portfolios.

Digitalization permeates each service line. API bridges now feed trust-account data into portfolio dashboards, giving clients a single view of assets. High-volume advisory processes are automated, releasing capacity for bankers to focus on complex structures. The regulatory backdrop remains supportive: the Financial Services Agency streamlines trust-bank licensing, while property-token guidelines released in 2024 clarify custodial responsibilities. As a result, the Japan private banking market continues to migrate from transactional product silos toward holistic, digitally enabled service bundles.

The Japan Private Banking Market Report is Segmented by Type (Asset Management Service, Insurance Service, Trust Service, Tax Consulting, Real Estate Consulting), Application (Personal, Enterprise), Client Wealth Tier (Mass Affluent, High-Net-Worth, Ultra-High-Net-Worth), and Geography (Kanto, Kansai, Chubu, Hokkaido & Tohoku, Chugoku & Shikoku, Kyushu & Okinawa). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mitsubishi UFJ Morgan Stanley PB

- Sumitomo Mitsui Trust Bank

- Mizuho Private Wealth Management

- Nomura Holdings

- Daiwa Securities Group

- Resona Bank

- Rakuten Bank Wealth Management

- SBI Shinsei Bank

- J-Trust Bank

- Aozora Bank

- Norinchukin Bank

- Shizuoka Bank

- Fukuoka Financial Group

- Tokyo Star Bank

- SMBC Nikko Securities Private

- UBS SuMi TRUST Wealth

- Credit Suisse PB Japan

- Barclays PB Japan

- HSBC PB Japan

- Citi Private Bank Japan

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging population driving inter-generational wealth transfer

- 4.2.2 Deregulation of fiduciary services under Japan's Stewardship Code

- 4.2.3 Digital transformation of wealth platforms (APIs, robo-advisory)

- 4.2.4 Rising stock-market valuation spurring affluent asset growth

- 4.2.5 Corporate-governance reforms triggering executive liquidity events

- 4.2.6 Tokyo metropolitan real-estate tokenization enabling new PB products

- 4.3 Market Restraints

- 4.3.1 Persistently low interest-rate environment compressing NIMs

- 4.3.2 Stricter Basel III capital requirements limiting risk appetite

- 4.3.3 Intensifying competition from foreign private banks

- 4.3.4 Cultural hesitancy among SMEs to outsource succession planning

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Asset Management Service

- 5.1.2 Insurance Service

- 5.1.3 Trust Service

- 5.1.4 Tax Consulting

- 5.1.5 Real Estate Consulting

- 5.2 By Application

- 5.2.1 Personal

- 5.2.2 Enterprise

- 5.3 By Client Wealth Tier

- 5.3.1 Mass Affluent

- 5.3.2 High-Net-Worth

- 5.3.3 Ultra-High-Net-Worth

- 5.4 By Region

- 5.4.1 Kanto

- 5.4.2 Kansai

- 5.4.3 Chubu

- 5.4.4 Hokkaido & Tohoku

- 5.4.5 Chugoku & Shikoku

- 5.4.6 Kyushu & Okinawa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mitsubishi UFJ Morgan Stanley PB

- 6.4.2 Sumitomo Mitsui Trust Bank

- 6.4.3 Mizuho Private Wealth Management

- 6.4.4 Nomura Holdings

- 6.4.5 Daiwa Securities Group

- 6.4.6 Resona Bank

- 6.4.7 Rakuten Bank Wealth Management

- 6.4.8 SBI Shinsei Bank

- 6.4.9 J-Trust Bank

- 6.4.10 Aozora Bank

- 6.4.11 Norinchukin Bank

- 6.4.12 Shizuoka Bank

- 6.4.13 Fukuoka Financial Group

- 6.4.14 Tokyo Star Bank

- 6.4.15 SMBC Nikko Securities Private

- 6.4.16 UBS SuMi TRUST Wealth

- 6.4.17 Credit Suisse PB Japan

- 6.4.18 Barclays PB Japan

- 6.4.19 HSBC PB Japan

- 6.4.20 Citi Private Bank Japan

7 Market Opportunities & Future Outlook

- 7.1 ESG-aligned impact-investment mandates for HNW portfolios

- 7.2 Digital-yen (CBDC) integration for cross-border wealth services