PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035006

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035006

Personalized Nutrition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

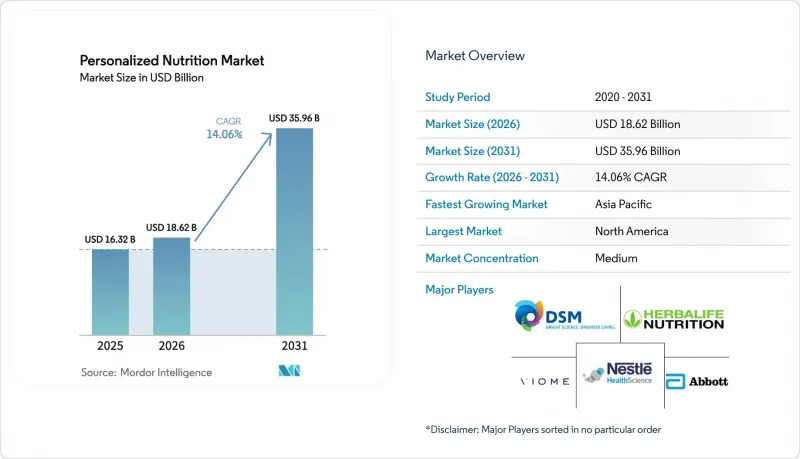

The personalized nutrition market size is expected to grow from USD 16.32 billion in 2025 to USD 18.62 billion in 2026 and is forecast to reach USD 35.96 billion by 2031 at 14.06% CAGR over 2026-2031.

This expansion reflects the shift from wellness add-ons to core healthcare tools powered by artificial intelligence, multi-omics testing, and continuous digital monitoring. Consumer willingness to invest in prevention rose sharply after the pandemic, while global spending on GLP-1 medications has made metabolic health top of mind across age groups. Employers are embedding precision wellness into benefit plans, and insurers in selected markets have begun to reimburse evidence-backed programs, signaling deeper integration into formal care pathways. Regulatory agencies now encourage science-based claims, which accelerates product approvals yet raises the bar for clinical proof and data stewardship.

Global Personalized Nutrition Market Trends and Insights

Shift in Consumer Health Awareness

Consumers now view food as a primary lever for disease prevention rather than an afterthought in treatment. Post-pandemic surveys show that 78% intend to make new wellness purchases by 2025, and more than half of those interested in personalized solutions are targeting weight management. Genetic testing kits appeal to a similar proportion, confirming mainstream readiness for individualized approaches. Companies such as Bioniq have capitalized, reporting a five-fold user increase in 2024 as transparency and measurable outcomes become non-negotiable purchasing criteria. The trend favors offerings that translate complex biomarker data into clear dietary actions, cementing demand for subscription-based models that enable continuous refinement.

Burden of Chronic Disease and Ageing Population

Type 2 diabetes affects more than 400 million people worldwide, and metabolic syndrome touches one-quarter of adults, pushing healthcare costs to unsustainable levels. Nutritional targeting has proved cost-effective in delaying progression, and randomized studies report measurable improvements in triglycerides, weight, and HbA1c when programs are personalized. Ageing intensifies the opportunity: adults over 65 are the fastest-growing group, seeking muscle preservation and cognitive support. Abbott's Ensure exceeded USD ~3 billion in 2024 on the back of this demographic shift. As payers recognize the economic upside, reimbursement pilots for nutrition-as-medicine are emerging, particularly for metabolic and cardiovascular indications.

High Product and Testing Costs

Comprehensive programs can reach USD 500 per month when testing, coaching, and customized supplements are bundled, limiting adoption among middle-income consumers. Manufacturing remains 3-5 times more expensive than standard capsules because small batches run counter to economies of scale. Insurance coverage is still sparse, exacerbating affordability issues in emerging markets where chronic disease prevalence is rising fastest. Tiered subscription models and simplified biomarker panels are lowering entry prices, yet core cost structures continue to restrain penetration until scale or automation offsets premium inputs.

Other drivers and restraints analyzed in the detailed report include:

- Digital-Health and Wearables Ecosystem Expansion

- AI-Enabled Microbiome Precision Formulations

- Data-Privacy and Ownership Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Active Measurement solutions contributed 57.48% of revenue in 2025, underscoring the appeal of quantified health feedback loops. The personalized nutrition market size for this segment is projected to expand at 15.23% CAGR to 2031, fueled by the rise of at-home biomarker kits and continuous glucose monitors that replace guesswork with data. Hyper-personalized blends generated from AI analysis of blood micronutrient gaps, such as Bioniq's "Build Your Own," position providers to upsell premium tiers that adjust compositions monthly.

Standard Measurement products still draw a loyal base seeking basic vitamin corrections at lower price points. However, their growth lags as consumers migrate toward offerings that promise measurable impacts. Partnerships with pharmacies and grocery chains could revive momentum by embedding entry-level kits into everyday shopping journeys. A hybrid strategy that pairs low-cost baseline formulations with optional data upgrades may allow Standard Measurement players to defend share without cannibalizing margins.

The Personalized Nutrition Market is Segmented by Product Type (Active Measurement and Standard Measurement), Application (Standard Supplements and Disease-Based Formulations), End User (Direct-To-Consumer, Wellness & Fitness Centres, Hospitals & Clinics), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 43.92% of global revenue in 2025 and remains the primary innovation hub for personalized nutrition market players. Venture funding, regulatory clarity, and high disposable incomes support premium pricing. The FDA's updated "healthy" labeling framework has further professionalized product claims. Canada contributes niche advances such as plant-based protein blends that outperform whey in clinical studies, reflecting regional demand for sustainable options. Employer wellness contracts and early insurer experiments continue to underpin North American leadership.

Asia Pacific is the fastest-growing region with a 14.34% CAGR forecast through 2031. China's three-year weight management plan and consumer openness to metabolic solutions draw multinational suppliers eager to localize formulas. India's 136 million pre-diabetic adults present a sizable addressable base, and local firms like Zantus Lifesciences have launched culturally adapted meal replacements to serve religious and taste preferences. Japan's Foods with Function Claims system, now valued at JPY 357 billion, provides a stringent yet predictable approval route, attracting cross-border entrants with evidence-backed ingredients. South Korea and Australia add momentum through technology adoption and public health campaigns.

Europe holds a significant share owing to evidence-driven consumer cultures and GDPR safeguards that encourage data trust. The European Food Safety Authority streamlined novel food evaluations in 2025, accelerating time to market for precision formulations. Germany, the United Kingdom, and France lead purchases, while Mediterranean countries focus on cardiovascular prevention programs that integrate nutrigenomics. Middle East and Africa, plus South America, remain in early adoption phases but benefit from rising internet penetration and private health investments. Strategic partnerships with local distributors, seen in iPRO's Saudi Arabia entry, illustrate the necessity of regional tailoring over one-size-fits-all approaches.

- Abbott Laboratories

- Amway

- Herbalife Nutrition

- Nestle

- DSM-Firmenich

- BASF

- Viome Life Sciences

- GX Sciences

- Metagenics

- ADM

- Care/of

- Persona Nutrition

- 23andMe

- InsideTracker

- ZOE

- Baze

- GNC

- Habit

- Nutrigenomix

- Superior Supplement Manufacturing

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift In Consumer Health Awareness

- 4.2.2 Burden Of Chronic Disease & Ageing Population

- 4.2.3 Digital-Health & Wearables Ecosystem Expansion

- 4.2.4 Direct-To-Consumer (DTC) Test Kit Affordability

- 4.2.5 Employer-Sponsored Precision-Wellness Programs

- 4.2.6 AI-Enabled Microbiome Precision Formulations

- 4.3 Market Restraints

- 4.3.1 High Product & Testing Costs

- 4.3.2 Limited Awareness In Emerging Nations

- 4.3.3 Data-Privacy & Ownership Concerns

- 4.3.4 Limited Clinical-Outcomes Validation

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Active Measurement

- 5.1.2 Standard Measurement

- 5.2 By Application

- 5.2.1 Standard Supplements

- 5.2.2 Disease-based Formulations

- 5.3 By End User

- 5.3.1 Direct-to-Consumer

- 5.3.2 Wellness & Fitness Centres

- 5.3.3 Hospitals & Clinics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Amway

- 6.3.3 Herbalife Nutrition

- 6.3.4 Nestle Health Science

- 6.3.5 DSM-Firmenich

- 6.3.6 BASF SE

- 6.3.7 Viome Life Sciences

- 6.3.8 GX Sciences

- 6.3.9 Metagenics

- 6.3.10 ADM

- 6.3.11 Care/of

- 6.3.12 Persona Nutrition

- 6.3.13 23andMe

- 6.3.14 InsideTracker

- 6.3.15 ZOE

- 6.3.16 Baze

- 6.3.17 GNC

- 6.3.18 Habit

- 6.3.19 Nutrigenomix

- 6.3.20 Superior Supplement Manufacturing

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment