PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066774

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066774

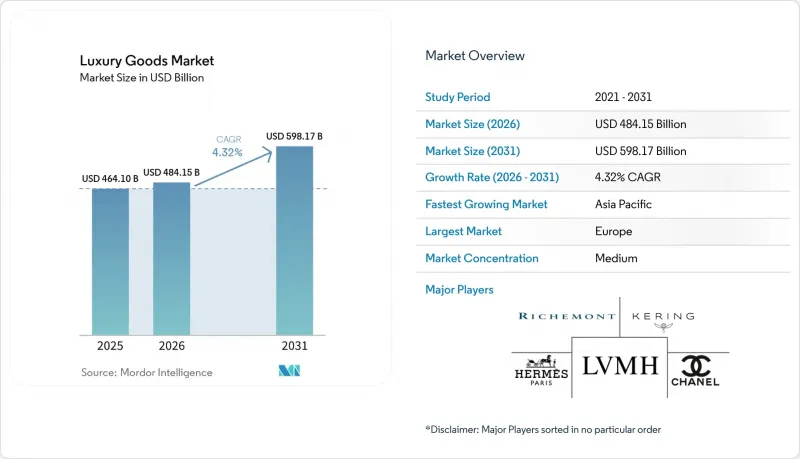

Luxury Goods - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the global luxury goods market size is expected to grow from USD 464.1 billion in 2025 to USD 484.15 billion in 2026 and is forecast to reach USD 598.17 billion by 2031 at 4.32% CAGR over 2026-2031.

This report is Segmented by Product Type (Clothing and Apparel, Footwear, and More), End User (Men, Women, and Unisex), Distribution Channel (Single Brand Stores, Multi Brand Stores, and More) and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Value (USD).

Global Luxury Goods Market Trends and Insights

Consumer shift toward sustainable and eco-certified luxury products

Sustainability is now a major factor driving the growth of the global luxury goods market. Luxury brands are increasingly adopting eco-friendly practices, such as offering buy-back programs, lifetime repair services, and creating collections from recycled materials in the luxury goods market. These efforts are further encouraged by regulatory requirements like the EU's Corporate Sustainability Reporting Directive and the upcoming digital product passports, which were implemented in September 2024 . This initiative, part of the Ecodesign for Sustainable Products Regulation, aims to enhance transparency across product value chains by providing comprehensive information about each product's origin, materials, environmental impact, and disposal recommendations. For instance, Chanel has announced its Nevold initiative, set to launch in 2025, which will transform unsold stock into premium recycled materials. Similarly, Bottega Veneta has introduced its "Certificate of Craft" program, which provides lifetime repair services and uses surplus leather to create new products. These sustainability-focused initiatives not only help luxury brands reduce their environmental impact but also enhance the exclusivity and value of their products.

Influence of social media and celebrity endorsement

Social media platforms like Instagram and TikTok have become vital tools for promoting and selling luxury goods, especially in rapidly growing markets. These platforms simplify the process for consumers, allowing them to easily discover products and make purchases. In the luxury goods market, widespread usage has made social media a key channel for luxury brands to connect with their audience. Influencer marketing has evolved from short-term promotions to long-term collaborations that build stronger brand associations. For instance, the long-term collaboration with David Beckham started in Q3 2024 with the Fall/Winter campaign, while the Spring/Summer 2024 collection featured Gisele Bundchen. These celebrity campaigns doubled social media engagement and reached 40 million livestream views. Similarly, Zendaya's role as an ambassador for Louis Vuitton continues to enhance the brand's appeal across both Western and Asian markets by creating aspirational connections with consumers. In 2024, Dior collaborated with Jisoo from BLACKPINK for a special campaign that combined the global influence of K-pop with the sophistication of Parisian high fashion.

Proliferation of counterfeit products

The rise of high-quality "superfakes" in the luxury goods market has made it harder to distinguish between genuine and counterfeit luxury products, pushing brands to adopt advanced technologies to protect their authenticity. In June 2025, Australian authorities arrested three individuals for selling counterfeit luxury goods worth AUD 10.7 million online. The operation also led to the seizure of over 500 fake luxury items, including handbags and watches, along with AUD 250,000 in cash and a gel blaster firearm. According to the OECD, the global trade in counterfeit goods reached USD 467 billion in 2025, posing significant risks to consumer safety and intellectual property rights . To combat this growing issue within the luxury goods market, brands like Prada and Vacheron Constantin have started using blockchain-based certificates to verify the authenticity of their products. The Aura Blockchain Consortium, supported by LVMH, Cartier, and Prada, has expanded its digital product passport initiative, which now tracks tens of millions of luxury items. As counterfeit goods become more normalized among younger consumers, luxury brands are not only increasing their enforcement efforts but also launching educational campaigns to emphasize the importance of authenticity as a core part of the luxury experience.

Other drivers and restraints analyzed in the detailed report include:

- Rising disposable income and wealth accumulation

- Consumers' inclination towards limited edition products

- Stringent regulatory environment and compliance costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, clothing and apparel dominated the global luxury goods market, claiming a 37.02% share. This underscores their pivotal role in shaping brand identities and weaving emotional narratives. Apparel, being one of the most prominent luxury categories, often acts as the initial touchpoint for consumers venturing into the luxury realm. Its engagement is perpetually heightened, influenced by seasonal trends, fashion weeks, and the sway of influencer marketing. The leather goods segment in the luxury goods market, intricately tied to fashion, is transforming, especially in Europe, where brands are turning to bio-based materials without compromising on luxury aesthetics. In the luxury goods market, the luxury beauty segment thrives, buoyed by the "lipstick effect." The premium skincare and cosmetics not only shine but also serve as more approachable gateways into the luxury world. This segment's vitality is further amplified by a resurgence in travel retail and an escalating self-care culture.

In the luxury goods market, luxury watches, however, are set to outpace all, with a projected CAGR of 4.38% through 2031. This surge underscores a notable pivot in consumer focus towards items that promise enduring value and emotional resonance. The allure of watches is bolstered by climbing auction prices, a burgeoning community of collectors, and the recognition of high-end mechanical timepieces as coveted, appreciating assets. In contrast to the ever-shifting world of fashion, watches boast a timeless charm, enduring functionality, and a storied brand legacy. Jewelry, too, stands resilient, cherished for its sentimental significance, cultural ties, and its reputation as a safeguard against inflation. Footwear and eyewear are carving out their niches, emphasizing comfort, sustainability, and advanced fitting technologies, ensuring their relevance in a luxury landscape increasingly driven by performance and values.

Geography Analysis

Europe contributed 52.10% of the revenue in the luxury goods market in 2025, driven by its famous luxury brands and strong tourism industry. Companies like Hermes, LVMH, and Kering have shown positive growth, but challenges such as currency changes and potential US tariffs create some uncertainty. Additionally, new EU sustainability rules are increasing costs, encouraging brands to invest in local production and innovative materials. European customers still prefer in-store shopping, making excellent service and exclusive product launches essential for maintaining loyalty. The region's mature market emphasizes the importance of creating unique shopping experiences to attract repeat customers and sustain growth in the luxury goods market.

In the luxury goods market, Asia-Pacific is expected to lead future growth, with a projected CAGR of 5.41% through 2031. China's recovery is supported by increased domestic spending and duty-free shopping policies in Hainan. India's growing beauty market and rising demand for designer clothing are also expanding the customer base. South-East Asia benefits from the rise of digital payments and the development of luxury-focused malls. To stay competitive, brands are adapting their products to local preferences, such as using lighter fabrics for tropical climates and launching special collections during regional festivals. This region's diverse markets offer significant opportunities for luxury brands to expand their presence.

North America continues to grow steadily, while unique shopping experiences in cities like Miami and Las Vegas encourage higher spending. The Middle East and Africa also show strong potential, with Dubai's flagship stores and Riyadh's Vision 2030 projects boosting demand for luxury goods. Africa's growing wealthy class is showing interest in jewelry and watches, though challenges like high import duties and logistics remain.

In South America, Brazil leads the luxury goods market, offering growth opportunities but requiring strategies like currency hedging and localized pricing to succeed.

- LVMH Moet Hennessy Louis Vuitton SE

- Kering SA

- Compagnie Financiere Richemont SA

- Chanel SA

- Hermes International SA

- Rolex SA

- The Swatch Group Ltd.

- Burberry Group Plc

- Capri Holdings Ltd

- Breitling SA

- Tapestry Inc.

- Moncler SpA

- Giorgio Armani SpA

- PVH Corp.

- Dolce & Gabbana Srl

- Audemars Piguet Holding SA

- Estee Lauder Companies Inc.

- Tod's S.p.A.

- MCM Global AG

- OTB Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Consumer Shift Toward Sustainable and Eco-Certified Luxury Products

- 4.2.2 Influence of Social Media and Celebrity Endorsement

- 4.2.3 Rising Disposable Income and Wealth Accumulation

- 4.2.4 Product Innovation in terms of Raw Material and Design

- 4.2.5 Consumers Inclination Towards Limited Edition Products

- 4.2.6 Growth of Experience-Based Luxury and Personalization Services

- 4.3 Market Restraints

- 4.3.1 Proliferation of counterfeit Products

- 4.3.2 Lesser demand from price sensitive consumers

- 4.3.3 Stringent Regulatory Environment and Compliance Costs

- 4.3.4 Economic Uncertainty and Inflation Impact on Consumer Spending

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Clothing and Apparel

- 5.1.2 Footwear

- 5.1.3 Eyewear

- 5.1.4 Leather Goods

- 5.1.5 Jewelry

- 5.1.6 Watches

- 5.1.7 Beauty and Personal Care

- 5.2 By End User

- 5.2.1 Men

- 5.2.2 Women

- 5.2.3 Unisex

- 5.3 By Distribution Channel

- 5.3.1 Single Brand Stores

- 5.3.2 Multi Brand Stores

- 5.3.3 Online Stores

- 5.3.4 Other Distribution Channels

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 LVMH Moet Hennessy Louis Vuitton SE

- 6.4.2 Kering SA

- 6.4.3 Compagnie Financiere Richemont SA

- 6.4.4 Chanel SA

- 6.4.5 Hermes International SA

- 6.4.6 Rolex SA

- 6.4.7 The Swatch Group Ltd.

- 6.4.8 Burberry Group Plc

- 6.4.9 Capri Holdings Ltd

- 6.4.10 Breitling SA

- 6.4.11 Tapestry Inc.

- 6.4.12 Moncler SpA

- 6.4.13 Giorgio Armani SpA

- 6.4.14 PVH Corp.

- 6.4.15 Dolce & Gabbana Srl

- 6.4.16 Audemars Piguet Holding SA

- 6.4.17 Estee Lauder Companies Inc.

- 6.4.18 Tod's S.p.A.

- 6.4.19 MCM Global AG

- 6.4.20 OTB Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK