PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035034

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035034

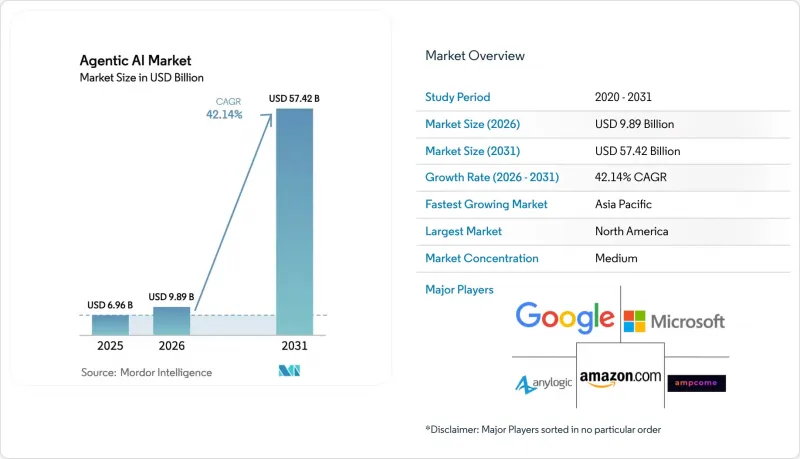

Agentic AI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The agentic AI market size was valued at USD 6.96 billion in 2025 and estimated to grow from USD 9.89 billion in 2026 to reach USD 57.42 billion by 2031, at a CAGR of 42.14% during the forecast period (2026-2031).

Accelerating enterprise migration toward autonomous systems, breakthroughs in large-language-model reasoning, and maturation of multi-agent orchestration frameworks anchor this trajectory. Cloud-native scalability is pushing deployments from proof-of-concept stages to production scale, while venture funding exceeding USD 40 billion in North America alone signals deep investor conviction. Large enterprises remain early adopters, yet simplified open-source stocks are opening the door for rapid SME entry. The competitive playing field is evolving toward platform ecosystems where orchestration reliability, data-sovereignty alignment, and domain-specific agent templates differentiate offerings.

Global Agentic AI Market Trends and Insights

Surge in Demand for Intelligent Automation

Enterprises are replacing rule-based bots with autonomous agents that manage unstructured, exception-heavy workstreams. Executive surveys show 61% of CEOs integrating agents into core operations, a level that surpassed adoption of earlier RPA waves. Wells Fargo's loan-processing agents synthesize multiple data feeds and adapt to compliance updates in real time, reducing turnaround to minutes. Supply-chain studies report 61% faster revenue growth for firms embedding intelligent automation over legacy workflow software. Such results prompting organizations to sunset static workflow engines and budget for end-to-end autonomous processes. The outcome is a direct uplift in the agentic AI market as digital employees displace siloed task automation.

Proliferation of Multi-Agent Systems for Complex Problem-Solving

Orchestration platforms now coordinate hundreds of specialized agents that collaborate to pursue enterprise-wide objectives. Microsoft's AutoGen allows customer service, sales, and technical-support agents to share state while optimizing outcomes. Siemens reached 90% touchless processing across industrial workflows, realizing EUR 5 million (USD 5.65 million) annual savings. Manufacturing, logistics, and financial hubs in APAC are adopting similar frameworks, driving the agentic AI market toward distributed architectures. As orchestration complexity grows, demand rises for platforms that guarantee reliable inter-agent communication, conflict resolution, and lineage tracking. These needs reinforce the market's shift away from monolithic AI toward modular, cooperative agent colonies.

Organizational Change-Management and Skill Gaps

Enterprises must rebuild governance, upskill staff, and redesign workflows to coexist with autonomous agents. Public-sector studies show potential savings of 1.2 billion labor hours annually, yet resistance remains high amid job-security concerns. Implementation stalls when legacy approval chains cannot accommodate non-human actors. Regulated industries wrestle with compliance frameworks written for human accountability, delaying rollouts. The shortage of AI-literate change-leaders slows the agentic AI market's diffusion even as technical viability improves. Vendors now bundle organizational-change consulting in service contracts to overcome this barrier.

Other drivers and restraints analyzed in the detailed report include:

- Advances in Cloud-Native AI Infrastructure

- Integration with Spatial-Computing/XR Ecosystems

- Ethical, Bias and Transparency Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is growing at 43.80% CAGR, outpacing the 61.65% solution share logged in 2025 as enterprises recognize that project success hinges on integration and change-management depth. Consulting teams architect agent frameworks, stitch legacy connectors, and institutionalize governance, often billing more than initial licensing. The agentic AI market size for services is expanding as continuous optimization and regulatory audits create recurring workstreams. Training and support remain vital as organizations tune agent behavior post-deployment. Leading vendors package pre-built domain agents still rely on professional services for bespoke orchestration and KPI alignment.

Implementation scope often spans data-quality assessment, model-governance policy, and employee-acceptance programs. UiPath's Maestro launch illustrated how orchestrator modules paired with premium consulting accelerate adoption. Other providers market "center-of-excellence in-a-box" offerings that embed best practices. As standards evolve, services partners able to certify ISO-aligned deployments will gain pricing power, reinforcing the agentic AI industry's services-heavy economics.

Hybrid environments post 44.60% CAGR, reflecting enterprises' need to balance cloud elasticity with on-premises sovereignty. Although cloud maintains 59.72% share, security-sensitive workflows, particularly in government and BFSI, demand local inference. The agentic AI market size allocated to hybrid stacks is rising as orchestration suites support seamless agent placement across Kubernetes clusters, private-cloud nodes, and edge gateways.

Automotive firms exemplify this split: supply-chain agents run in public clouds to ingest market feeds, while quality-control agents stay on factory servers to protect trade secrets. Vendors now tout zero-trust connectors, unified observability, and policy-based routing that decide where each agent executes. This flexibility reduces vendor lock-in but raises integration complexity, expanding service revenue.

The Agentic AI Market Report is Segmented by Component (Solution, Services), Deployment Mode (On-Premises, Cloud, Hybrid), Organization Size (Small and Medium Enterprises, Large Enterprises), End-User Industry (Healthcare, BFSI, and More), Agent Architecture (Single-Agent Systems, Multi-Agent Systems), Application (Autonomous Process Automation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 40.25% of the agentic AI market in 2025 thanks to deep venture pools, cloud infrastructure density, and research leadership. OpenAI's revenue path from USD 12.7 billion in 2025 toward USD 125 billion by 2029 highlights regional commercialization momentum. Federal agencies, guided by the DHS AI playbook, run pilots across mission-support functions and are earmarking multi-year budgets for scale-out. Canada fosters natural-resource optimization agents, while Mexico explores cross-border trade automation, reinforcing continental depth.

Asia-Pacific is the fastest-growing territory at 44.95% CAGR. China's projected expansion from USD 4.5 billion in 2023 to USD 82.1 billion by 2033 sets the tone, driven by factory automation and consumer-service bots. Japan applies agents to high-precision manufacturing, realizing 20% annual growth in deployments. India's developer ecosystem supplies global agent design, while South Korea and Singapore integrate agentic frameworks into smart-city platforms. Patent data showing 30% of global AGI filings emanating from China underscores APAC's technical ascendancy.

Europe advances steadily under stringent regulation. The EU AI Act compels transparent, auditable agent behavior, slowing volume but elevating governance standards. Germany leverages agents for Industry 4.0 excellence, the UK embeds them in fintech compliance, and France funds sovereign AI stacks. Middle East and Africa register nascent uptake through smart-city, oil-and-gas, and public-service rollouts, often drawing on hybrid architectures to navigate bandwidth and latency constraints.

- Microsoft Corporation

- Amazon Web Services Inc.

- Google LLC

- IBM Corporation

- Oracle Corporation

- Salesforce Inc.

- SAP SE

- UiPath Inc.

- Epicor Software Corp.

- Coupa Software Inc.

- Zycus Inc.

- The AnyLogic Company

- Ampcome Technologies Pvt Ltd

- OpenAI Ltd.

- Anthropic PBC

- Adept AI Labs

- Cohere Inc.

- Rasa Technologies GmbH

- Pegasystems Inc.

- Baidu Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in demand for intelligent automation

- 4.2.2 Proliferation of multi-agent systems for complex problem-solving

- 4.2.3 Advances in cloud-native AI infrastructure

- 4.2.4 Integration with spatial-computing/ XR ecosystems

- 4.2.5 Emergence of agentic AI performance benchmarks

- 4.2.6 Open-source agent frameworks for SMEs

- 4.3 Market Restraints

- 4.3.1 Organizational change-management and skill gaps

- 4.3.2 Ethical, bias and transparency concerns

- 4.3.3 Escalating compute/resource costs for agent orchestration

- 4.3.4 Lack of interoperability / vendor lock-in

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Framework of Agentic AI System

- 4.9 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solution

- 5.1.2 Services

- 5.1.2.1 Consulting and Integration Services

- 5.1.2.2 Training and Support Services

- 5.1.2.3 Other Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 Healthcare

- 5.4.2 BFSI

- 5.4.3 IT and Telecom

- 5.4.4 Manufacturing

- 5.4.5 Government and Public Sector

- 5.4.6 Automotive

- 5.4.7 Retail and E-commerce

- 5.4.8 Other End-user Industries

- 5.5 By Agent Architecture

- 5.5.1 Single-Agent Systems

- 5.5.2 Multi-Agent Systems (MAS)

- 5.6 By Application

- 5.6.1 Autonomous Process Automation

- 5.6.2 Predictive Analytics and Decision Support

- 5.6.3 Intelligent Virtual Assistants

- 5.6.4 RPA Integration

- 5.6.5 Smart Manufacturing and IIoT

- 5.6.6 Other Applications

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Chile

- 5.7.2.4 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Australia

- 5.7.4.6 Singapore

- 5.7.4.7 Malaysia

- 5.7.4.8 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 United Arab Emirates

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Nigeria

- 5.7.5.2.3 Egypt

- 5.7.5.2.4 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Amazon Web Services Inc.

- 6.4.3 Google LLC

- 6.4.4 IBM Corporation

- 6.4.5 Oracle Corporation

- 6.4.6 Salesforce Inc.

- 6.4.7 SAP SE

- 6.4.8 UiPath Inc.

- 6.4.9 Epicor Software Corp.

- 6.4.10 Coupa Software Inc.

- 6.4.11 Zycus Inc.

- 6.4.12 The AnyLogic Company

- 6.4.13 Ampcome Technologies Pvt Ltd

- 6.4.14 OpenAI Ltd.

- 6.4.15 Anthropic PBC

- 6.4.16 Adept AI Labs

- 6.4.17 Cohere Inc.

- 6.4.18 Rasa Technologies GmbH

- 6.4.19 Pegasystems Inc.

- 6.4.20 Baidu Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-space and Unmet-Need Assessment