PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035057

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035057

Telecom Towers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

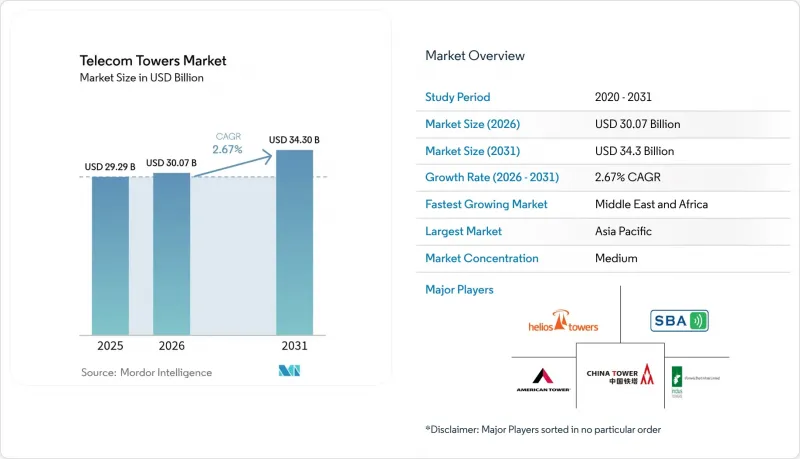

The Telecom Towers Market size was valued at USD 29.29 billion in 2025 and estimated to grow from USD 30.07 billion in 2026 to reach USD 34.3 billion by 2031, at a CAGR of 2.67% during the forecast period (2026-2031).

This steady trajectory reflects how mobile network operators (MNOs) are shifting from rapid green-field rollouts toward infrastructure sharing and energy-efficient upgrades that protect margins in a capital-intensive environment. Continued 5G densification, government-backed rural coverage programs, and accelerating adoption of hybrid renewable power systems keep demand resilient, yet the overall pace remains measured as co-location ratios climb, and spectrum costs weigh on operator budgets. Regionally, Asia-Pacific leads growth thanks to China Tower's 2.04 million-site portfolio and India's USD 16.1 billion rural connectivity plan, while North America and Europe focus on optimizing existing assets amid zoning headwinds. Transaction activity highlights the sector's maturation: operators are monetizing tower portfolios and redeploying proceeds into spectrum and core-network upgrades, underscoring a strategic pivot toward asset-light operating models.

Global Telecom Towers Market Trends and Insights

5G Network Rollouts Drive Infrastructure Densification

Operators must increase site density by three to five times compared with 4G to deliver 5G's low-latency targets, especially in high-band millimetre-wave spectrum. Latin America alone is expected to reach 425 million 5G connections by 2030, necessitating both traditional macro towers and growing layers of small cells. Regulatory bodies are responding: the Canadian Radio-television and Telecommunications Commission (CRTC) streamlined attachment rules so carriers can add 5G radios on existing structures without lengthy permissions. These policy shifts shorten deployment cycles and support consistent upward demand for new and upgraded tower sites across major urban corridors.

Rising Mobile Data Usage Pressures Network Capacity

U.S. wireless data consumption climbed 36% during 2024 as video streaming, cloud gaming, and enterprise mobility took hold, forcing carriers such as Crown Castle's tenants to densify urban footprints and expand rural coverage. Emerging markets mirror this surge as affordable smartphones proliferate. Techniques like carrier aggregation and massive-MIMO can stretch the spectrum, yet physical infrastructure remains the gating factor. As a result, the telecom towers market continues to exhibit incremental but durable expansion, with operators relying on tower companies to accelerate capacity meets.

Tower-Sharing Saturation Limits Mature-Market Upside

Co-location ratios in North America and Western Europe hover around 2.7 tenants per tower, leaving limited headroom for incremental leasing revenue. Structural limits complicate upgrades for heavier 5G equipment, prompting costly reinforcements that erode returns. While new tenancy pipelines remain healthy in emerging economies, saturation tempers growth in established regions, nudging the global telecom towers market toward a more balanced expansion profile.

Other drivers and restraints analyzed in the detailed report include:

- Rural Connectivity Programs Unlock New Market Opportunities

- MNO Tower-Asset Monetization Accelerates Industry Restructuring

- Environmental and Zoning Restrictions Complicate Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Non-renewable sources dominated with 72.88% telecom towers market share in 2025, anchored by grid electricity and diesel generators for macro-cell sites. However, renewables deliver the fastest growth at a 5.22% CAGR as operators pivot to solar-battery hybrids that slash operating expense in remote areas. Renewable adoption is most pronounced in regions with erratic grid supply and high diesel logistics costs; Telefonica Germany's energy self-sufficient 5G tower demonstrates viability in temperate climates. Hybrid systems also curb carbon output, aligning infrastructure providers with tightening ESG mandates and drawing green-finance capital toward the telecom towers market.

Progressive tower companies now bundle energy-as-a-service contracts, allowing MNOs to outsource both site and power management. As smart controllers and AI-driven battery analytics optimize consumption curves, the telecom towers industry is transitioning from energy consumer to localized producer. That evolution widens margin opportunity, diversifies revenue, and reinforces the sector's role in sustainable connectivity.

Lattice towers retained a 55.62% share in 2025 because their triangulated-steel design supports heavy multi-band payloads at economical cost. They remain the backbone for wide-area coverage across rural expanses of Asia-Pacific and Africa. Monopoles, though, exhibit the highest growth at 4.12% CAGR in urban corridors. Their single-column form factors reduce right-of-way and skirt aesthetic objections, enabling faster permitting cycles. Carbon-fiber monopoles introduced in 2024 weigh one-twelfth of steel yet deliver twelve times the tensile strength, curbing transport and foundation expense while extending asset life.

Stealth and guyed variants round out the portfolio: stealth solutions satisfy zoning mandates in heritage districts, while guyed towers address ultra-tall applications where land is abundant. Collectively, diversified designs help the telecom towers market serve both densification and rural outreach targets without compromising economics.

The Telecom Towers Market Report is Segmented by Fuel Type (Renewable, Non-Renewable), Type of Tower (Lattice Tower, Guyed Tower, Monopole Tower, Stealth Tower), Installation (Rooftop, Ground-Based), Ownership (Operator-Owned, Joint Venture, Private-Owned, MNO Captive), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific remains the engine of global growth, backed by China's 2.04 million-site footprint and India's aggressive 5G targets that will add hundreds of thousands of new tenancies by 2030. Government policy is supportive: spectrum auctions prioritize coverage, and rural subsidies narrow viability gaps. Japan and South Korea refine ultra-dense architectures that layer small cells onto macro grids, while Southeast Asian markets pursue tower-sharing frameworks to accelerate rollout and contain costs. These dynamics solidify Asia-Pacific's status as both the largest and fastest-growing slice of the telecom towers market.

North America presents a mature but technologically advanced landscape. Extensive co-location has tempered new-build volumes, yet 5G upgrades and edge-data-center initiatives sustain leasing demand. Federal programs such as the Rural 5G Fund bridge the economics of sparsely populated territories, steering incremental growth toward underserved communities. Regulatory headwinds arise at the municipal level, where zoning inertia and aesthetic opposition can extend project timelines, but federal pre-emption measures are narrowing the window for local vetoes.

Europe shows a two-speed pattern. Western markets face saturation and stringent environmental scrutiny, prompting tower companies to innovate with renewable-powered sites and stealth designs that satisfy eco-centric regulations. Eastern Europe and the Balkans, in contrast, are earlier in the 5G curve; spectrum auctions and EU connectivity funds support green-field construction that lifts overall regional momentum. Meanwhile, the Middle East advances consolidation, with TowerCo share surpassing 44% on the back of STC's TAWAL and Zain's TASC platforms. Latin America benefits from America Movil's USD 7.7 billion Brazil commitment and expanding 5G auctions, while Africa's long-term potential rests on government digitization plans that combine satellite backhaul, rural subsidies, and universal-service mandates.

- American Tower Corporation

- Cellnex Telecom S.A.

- China Tower Corporation Limited

- SBA Communications Corporation

- Indus Towers Limited

- Helios Towers PLC

- IHS Holding Limited

- Vantage Towers AG

- Deutsche Funkturm GmbH

- TAWAL Company Ltd.

- Telxius Telecom S.A.

- Telesites S.A.B. de C.V.

- AT&T Inc.

- T-Mobile US, Inc.

- GTL Infrastructure Limited

- Orange S.A.

- Telenor ASA

- PT Dayamitra Telekomunikasi Tbk (Mitratel)

- Ooredoo Q.P.S.C.

- Zong Pakistan (CMPak Limited)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G network roll-outs

- 4.2.2 Rising mobile data and smartphone usage

- 4.2.3 Rural connectivity programmes

- 4.2.4 MNO tower-asset monetisation

- 4.2.5 Edge data-centre co-location demand

- 4.2.6 Hybrid renewable power systems adoption

- 4.3 Market Restraints

- 4.3.1 Tower-sharing saturation

- 4.3.2 Environmental and zoning restrictions

- 4.3.3 High-strength steel and composite supply constraints

- 4.3.4 LEO-satellite rural coverage substitution

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Fuel Type

- 5.1.1 Renewable

- 5.1.2 Non-Renewable

- 5.2 By Type of Tower

- 5.2.1 Lattice Tower

- 5.2.2 Guyed Tower

- 5.2.3 Monopole Tower

- 5.2.4 Stealth Tower

- 5.3 By Installation

- 5.3.1 Rooftop

- 5.3.2 Ground-based

- 5.4 By Ownership

- 5.4.1 Operator-owned

- 5.4.2 Joint Venture

- 5.4.3 Private-owned

- 5.4.4 MNO Captive

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 American Tower Corporation

- 6.4.2 Cellnex Telecom S.A.

- 6.4.3 China Tower Corporation Limited

- 6.4.4 SBA Communications Corporation

- 6.4.5 Indus Towers Limited

- 6.4.6 Helios Towers PLC

- 6.4.7 IHS Holding Limited

- 6.4.8 Vantage Towers AG

- 6.4.9 Deutsche Funkturm GmbH

- 6.4.10 TAWAL Company Ltd.

- 6.4.11 Telxius Telecom S.A.

- 6.4.12 Telesites S.A.B. de C.V.

- 6.4.13 AT&T Inc.

- 6.4.14 T-Mobile US, Inc.

- 6.4.15 GTL Infrastructure Limited

- 6.4.16 Orange S.A.

- 6.4.17 Telenor ASA

- 6.4.18 PT Dayamitra Telekomunikasi Tbk (Mitratel)

- 6.4.19 Ooredoo Q.P.S.C.

- 6.4.20 Zong Pakistan (CMPak Limited)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment