PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035088

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035088

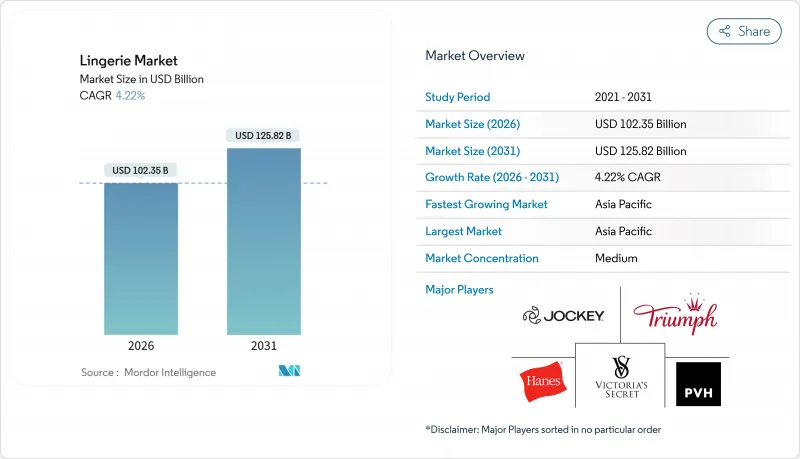

Lingerie - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The lingerie market size is USD 102.35 billion in 2026 and is projected to reach USD 125.82 billion by 2031, reflecting a 4.22% CAGR.

This growth is being driven by several key factors, including the ongoing trend of urbanization, the increasing participation of women in the workforce, and the rapid adoption of virtual fitting technologies. These elements are collectively propelling the lingerie market toward higher-margin digital sales channels. Brands are increasingly focusing on strategies such as offering extended sizing options, utilizing recyclable fibers, and leveraging data-driven product launches to meet evolving consumer demands. However, the market faces challenges, including fluctuations in raw material prices and the prevalence of counterfeit products, which are impacting overall profitability. The competitive landscape is undergoing a significant transformation, shifting away from traditional department-store aisles to omnichannel ecosystems. In these ecosystems, algorithm-driven fit recommendations and influencer-led storytelling are becoming critical factors in driving customer conversions. The Asia-Pacific region continues to be the epicenter of market growth, fueled by rising disposable incomes and changing consumer preferences. Meanwhile, North America and Europe are prioritizing sustainability initiatives, using eco-friendly practices and materials to justify premium pricing and appeal to environmentally conscious consumers.

Global Lingerie Market Trends and Insights

Rising body positivity trends fuel demand for inclusive sizing and styles

Body-positive messaging has evolved from being a focus of social-media activism to becoming a practical reality within supply chains. This shift has driven brands to expand their size ranges and feature models who represent their actual customer base, moving away from traditional runway standards. In 2024, ThirdLove launched a 78-size matrix, utilizing machine-learning algorithms trained on 15 million fit profiles. This approach aims to identify the ideal cup-and-band combinations for underserved body types. Similarly, in 2025, Savage X Fenty expanded its size range to include 4XL. This move was paired with celebrity endorsements that helped normalize lingerie for individuals with fuller figures. These changes are pressuring established players to adapt by updating manufacturing processes and retraining retail staff, which incurs significant short-term costs that smaller brands often cannot manage. Additionally, this shift complicates inventory management, as brands must carry a broader range of sizes without a proportional increase in sales velocity. This dynamic increases working-capital demands and the risk of markdowns. Although regulatory influence in this area remains minimal, voluntary commitments to size diversity are becoming an industry norm, driven by consumer backlash against brands perceived as exclusionary.

Increasing disposable income supports premium and luxury lingerie purchases

The premium lingerie segment is experiencing growth, driven by increasing disposable incomes in emerging markets. According to the Office for National Statistics data from 2024, the median household disposable income in the United Kingdom was GBP 43,500. Rising household incomes in Asia-Pacific and the Middle East are fueling increased demand for premium lingerie, contrasting with the luxury-spending fatigue seen in mature markets. Bank of America's 2025 consumer survey highlighted that affluent shoppers in China and India are prioritizing intimate apparel, considering it both a functional need and an aspirational purchase. To address this trend, brands are introducing tiered collections, including mass-market lines for higher sales volumes and exclusive limited-edition silk or lace pieces to achieve better margins. This approach helps brands attract aspirational first-time buyers while retaining repeat customers willing to upgrade. However, the strategy carries the risk of brand dilution if premium and mass-market products are displayed in the same retail spaces or promoted through the same marketing channels. The impact is particularly significant in urban areas, where disposable income growth surpasses inflation, creating high-margin demand pockets within predominantly price-sensitive markets.

Counterfeit and low-quality products dilute brand value and consumer trust

Counterfeit lingerie not only undermines brand equity but also poses safety risks. Fake products frequently utilize substandard materials, leading to skin irritations or inadequate support. This issue is especially pronounced in e-commerce, where visual checks are limited, and consumers often prioritize price over authenticity. In 2024, United States Customs and Border Protection reported seizing nearly USD 5 billion worth of counterfeit luxury items, including fashion and footwear products . The problem is exacerbated on online marketplaces, where third-party platforms frequently list counterfeit lingerie at discounted prices, undermining legitimate retailers. In response, brands are turning to blockchain authentication and QR-code traceability to fight counterfeits. However, these solutions come with added costs and necessitate consumer education. Furthermore, the rise of counterfeits muddles demand signals for brands, making it challenging to discern between genuine shifts in consumer preference and a move towards cheaper imitations. This confusion complicates inventory management and the development of new products.

Other drivers and restraints analyzed in the detailed report include:

- Technological innovations like virtual fitting rooms improve customer experience

- Celebrity endorsements and social media marketing enhance brand visibility

- Intense competition from local and unbranded players pressures pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Brassieres accounted for 58.36% of the 2025 revenue and are projected to grow at a rate of 9.27% through 2031. This growth is driven by the introduction of expanded size ranges and the use of moisture-wicking fabrics, enhancing their appeal for activewear. In 2024 and 2025, wireless and bralette styles gained popularity as work-from-home trends persisted, with consumers favoring comfort over traditional structured support. Briefs, the second-largest category, capitalized on the athleisure trend. Seamless and high-waisted designs in briefs increasingly blurred the distinction between intimate apparel and outerwear. Other product categories, such as shapewear, camisoles, and sleepwear, hold a smaller market share but are attracting significant innovation. Efforts are particularly focused on sustainable materials and adaptive designs tailored for postpartum and mastectomy customers.

The shift toward inclusive sizing is significantly altering manufacturing dynamics and economics. Brands are now required to stock between 50 to 80 SKUs per style, a substantial increase from the historical range of 20 to 30 SKUs. This shift has led to higher inventory carrying costs and an elevated risk of markdowns if demand forecasts are inaccurate, posing challenges for inventory management and profitability. Despite limited regulatory influence, voluntary commitments to size diversity are becoming increasingly important in the competitive landscape. These commitments are now viewed as essential by consumers, who are more likely to penalize brands perceived as exclusionary. As a result, inclusive sizing has emerged as a critical factor for brands aiming to maintain relevance and competitiveness in the market.

Mass-market lingerie accounted for 75.84% of the revenue in 2025, targeting price-sensitive consumers in emerging markets and budget-conscious shoppers in developed economies. At the same time, the premium segment is projected to grow at a rate of 9.62%. This growth is driven by affluent buyers who, despite a general slowdown in luxury spending, are choosing to "trade up." In both China and India, affluent shoppers increasingly perceive intimate apparel as both a necessity and an aspirational luxury. Premium brands are distinguishing themselves through strategies such as limited-edition fabrics, celebrity collaborations, and unique retail experiences. For instance, La Perla opened a flagship store in Dubai in 2024, featuring private fitting suites and champagne service, aimed at high-net-worth individuals willing to spend between USD 200 to USD 500 per piece.

The gap between mass and premium segments continues to widen. Brands are introducing tiered collections to appeal to both segments, but this approach risks brand dilution, particularly when premium and mass products share the same retail or marketing platforms. In 2025, Hanesbrands launched a premium sub-brand that highlighted organic cotton and lace and was priced higher than its core Hanes line. However, the brand struggled to establish its luxury credibility among consumers. Conversely, premium brands like Chantelle and Calida are exploring more accessible price points to sustain volume, though they face challenges with margin compression affecting profitability. The premium segment's resilience is attributed to its relatively lower price point compared to luxury handbags or jewelry, making it a more attainable entry into luxury for younger consumers who are building brand loyalty.

The Global Lingerie Market Report is Segmented by Product Type (Brassiere, Briefs, Other Product Types), Price Range (Mass, Premium), Material (Cotton, Silk and Satin, Synthetic, and More), Distribution Channel (Supermarkets/Hypermarkets, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units)

Geography Analysis

In 2025, the Asia-Pacific region accounted for 62.38% of the revenue share and is expected to grow at a rate of 10.14% through 2031. This growth is primarily driven by increasing middle-class incomes in China and India. Notably, tier-2 and tier-3 cities in these countries are emerging as key areas for new customer acquisitions. Furthermore, the rising participation of women in the workforce supports market growth. For example, data from India's Ministry of Statistics and Programme Implementation showed an increase in female labor force participation from 33.4% in April-June 2025 to 33.7% in July-September 2025 . Although logistics costs in China's lower-tier cities are higher than in coastal hubs, discouraging brands from offering full assortments, e-commerce platforms like Tmall and JD.com are addressing these challenges by providing subsidized shipping and virtual fitting tools. Japan's market, which matured earlier, is led by brands like Wacoal and Triumph. These companies focus on innovations catering to an aging population, with products such as wider bands and softer fabrics gaining traction in 2024 and 2025. Southeast Asia's market is fragmented: Indonesia and Thailand prefer locally priced brands, while Singapore and Malaysia's higher disposable incomes and exposure to Western fashion trends drive premium market penetration.

North America and Europe together contributed approximately 30% of the 2025 sales. However, both regions faced challenges from market saturation and shifting consumer preferences. In Europe, a growing emphasis on sustainability increased demand for Global Organic Textile Standard (GOTS)-certified organic cotton and recycled polyester. This trend is expected to accelerate with the European Union's Ecodesign for Sustainable Products Regulation, set to take effect in 2027, which will require carbon-footprint disclosures. Canada and Mexico displayed differing market dynamics: Canada followed United States trends, focusing on inclusive sizing and digital platforms, while Mexico's market remained divided between premium imports and local unbranded products.

Urban centers in South America, the Middle East, and Africa drove the remaining market share. Brazil's lingerie market benefited from a strong domestic manufacturing base and a cultural preference for bold designs. However, economic instability and currency depreciation constrained growth in the premium segment. The Middle East's luxury demand, supported by high incomes in Gulf Cooperation Council countries, faced challenges due to conservative cultural norms that limited advertising and product visibility. As a result, brands relied on word-of-mouth and influencer partnerships. South Africa's market reflected broader African trends: organized retail penetration remained low, and distribution challenges in smaller cities hindered brands from tapping into latent demand. Nevertheless, the adoption of mobile commerce provided an opportunity to reach underserved consumers.

- Victoria's Secret and Co.

- Hanesbrands Inc.

- PVH Corp.

- Wacoal Holdings Corp.

- Triumph International

- Berkshire Hathaway Inc. (Fruit of the Loom)

- MAS Holdings

- Jockey International Inc.

- Aimer Group

- Etam Developpement

- Chantelle Groupe

- Calida Holding AG

- Hunkemoller International B.V.

- Savage X Fenty

- ThirdLove

- La Perla Global Management (UK) Ltd.

- Chico's FAS

- Inditex S.A.

- Cosabella

- Marks and Spencer Group plc

- Fast Retailing Co., Ltd.

- Adore Me Inc.

- Oysho (Added)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Body Positivity Trends Fuel Demand for Inclusive Sizing and Styles

- 4.2.2 Increasing Disposable Income Supports Premium and Luxury Lingerie Purchases

- 4.2.3 Celebrity Endorsements and Social Media Marketing Enhance Brand Visibility

- 4.2.4 Technological Innovations Like Virtual Fitting Rooms Improve Customer Experience

- 4.2.5 Rising Demand for Sustainable and Ethically Made Lingerie Influences Buying Choices

- 4.2.6 Expansion of E-Commerce Improves Accessibility and Product Variety

- 4.3 Market Restraints

- 4.3.1 Counterfeit And Low-Quality Products Dilute Brand Value and Consumer Trust

- 4.3.2 Intense Competition from Local and Unbranded Players Pressures Pricing

- 4.3.3 Conservative Cultural Norms in Some Markets Discourage Open Lingerie Advertising

- 4.3.4 Limited Access to Quality Lingerie in Tier 2 And 3 Cities Restricts Potential Demand

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Product Type

- 5.1.1 Brassiere

- 5.1.2 Briefs

- 5.1.3 Other Product Types

- 5.2 By Price Range

- 5.2.1 Mass

- 5.2.2 Premium

- 5.3 By Material

- 5.3.1 Cotton

- 5.3.2 Silk and Satin

- 5.3.3 Synthetic (Nylon, Polyester, Spandex)

- 5.3.4 Recycled and Bio-based Fibers

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Specialty Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Colombia

- 5.5.2.4 Chile

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Sweden

- 5.5.3.8 Belgium

- 5.5.3.9 Poland

- 5.5.3.10 Netherlands

- 5.5.3.11 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Thailand

- 5.5.4.5 Singapore

- 5.5.4.6 Indonesia

- 5.5.4.7 South Korea

- 5.5.4.8 Australia

- 5.5.4.9 New Zealand

- 5.5.4.10 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Victoria's Secret and Co.

- 6.4.2 Hanesbrands Inc.

- 6.4.3 PVH Corp.

- 6.4.4 Wacoal Holdings Corp.

- 6.4.5 Triumph International

- 6.4.6 Berkshire Hathaway Inc. (Fruit of the Loom)

- 6.4.7 MAS Holdings

- 6.4.8 Jockey International Inc.

- 6.4.9 Aimer Group

- 6.4.10 Etam Developpement

- 6.4.11 Chantelle Groupe

- 6.4.12 Calida Holding AG

- 6.4.13 Hunkemoller International B.V.

- 6.4.14 Savage X Fenty

- 6.4.15 ThirdLove

- 6.4.16 La Perla Global Management (UK) Ltd.

- 6.4.17 Chico's FAS

- 6.4.18 Inditex S.A.

- 6.4.19 Cosabella

- 6.4.20 Marks and Spencer Group plc

- 6.4.21 Fast Retailing Co., Ltd.

- 6.4.22 Adore Me Inc.

- 6.4.23 Oysho (Added)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK