PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035095

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035095

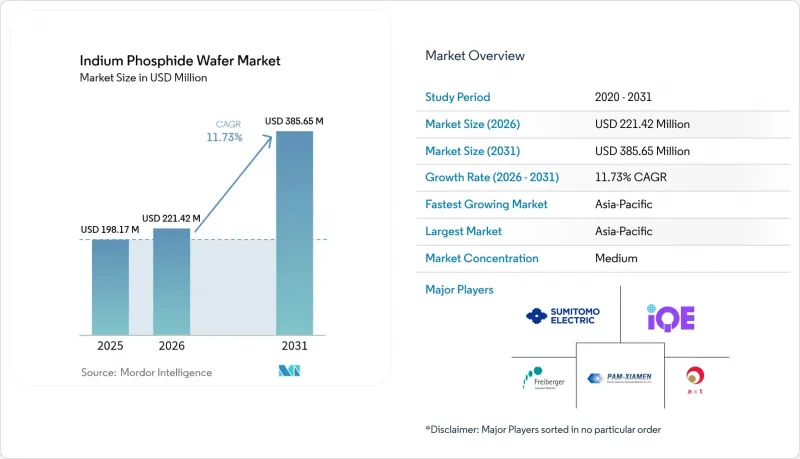

Indium Phosphide Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The indium phosphide wafer market size is expected to grow from USD 198.17 million in 2025 to USD 221.42 million in 2026 and is forecast to reach USD 385.65 million by 2031 at 11.73% CAGR over 2026-2031.

Hyperscale data-center upgrades drive momentum to 800 G and 1.6 T optics, the global rollout of 5 G and preparation for 6 G backhaul, as well as expanding quantum-photonics funding. Larger-diameter substrates lower unit costs, while hybrid InP-on-Si platforms promise further scalability. Asia-Pacific's integrated compound-semiconductor ecosystem anchors supply, yet Western re-shoring programs are accelerating domestic capacity. Competitive intensity stays moderate because crystal-growth know-how, long customer qualifications, and high capex deter new entrants.

Global Indium Phosphide Wafer Market Trends and Insights

High-speed optical-transceiver demand accelerates InP adoption

Cloud operators moving to 800 G and 1.6 T links require edge-emitting lasers and photodiodes that only indium phosphide can provide at the required speeds. Coherent tripled its InP-device output in Q4 2024 and is now sampling 3.2 T transceivers. Source Photonics demonstrated a 1.6 T coherent module using InP-based components, validating the material's indispensability for co-packaged optics. As switch ASICs advance toward 51T bandwidth, pluggable optics give way to on-board laser engines, reducing substrate volumes for the indium phosphide wafer market.

5G infrastructure rollout drives millimeter-wave demand

Commercial 5G backhaul operates above 28 GHz, where InP HBTs offer a cutoff frequency of more than 450 GHz and a breakdown voltage of more than 4.5 V. Nokia's USD 2.3 billion purchase of Infinera secures InP coherent expertise for transport nodes. Early 6G testbeds exploring terahertz frequencies rely on InP HEMTs, which have been validated up to 610 GHz. Consequently, substrate demand rises not only for optical front-ends but also for RF chains within the indium phosphide wafer market.

Supply-chain vulnerabilities threaten stability

China's 2024 expansion of export controls to indium-bearing compounds elevated price volatility and lead-time uncertainty. Western wafer makers now qualify alternative gallium and phosphorus suppliers, yet achieving raw-material self-sufficiency cannot be done quickly. Coherent's CHIPS Act project mitigates some risk, but near-term procurement pressure trims margins across the indium phosphide wafer market.

Other drivers and restraints analyzed in the detailed report include:

- Rising consumer SWIR sensing broadens addressable base

- Quantum-photonics R&D spurs specialty substrate demand

- Cost competitiveness limits penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 100 mm class retained a 43.72% indium phosphide wafer market share in 2025, catering to mainstream transceiver lines that strike a balance between cost and yield. A shift toward 150 mm substrates is underway, driven by Nokia's 6-inch pilot line utilizing AIXTRON G10-AsP reactors. The indium phosphide wafer market size for 150 mm formats is forecasted to grow at a 13.15% CAGR, narrowing the cost gap with GaAs. Yet, mechanical fragility above 6 inches restrains further scale, so 76.2 mm wafers remain relevant for specialty photonics that demand tight thickness uniformity.

Growth in large-diameter output hinges on investment in carriers and edge-grip tools designed for low-modulus crystals. Coherent's Texas expansion adopts automated handling to reduce breakage, targeting yields of over 85% for prime wafers. Meanwhile, 50.8 mm wafers persist in university R&D, where tooling upgrades are prohibitively expensive. A diverse diameter mix therefore co-exists within the indium phosphide wafer market through 2031.

Undoped conductive substrates led with a 36.18% share in 2025, underpinning photonic-integrated-circuit epitaxy. Semi-insulating Fe-doped wafers are projected to post a 12.93% CAGR, accelerating alongside 5G RF-power amplifiers that require substrate isolation for low noise. N-type Sn-doped and P-type Zn-doped slices target HEMT and HBT devices, but their volumes remain niche compared to Fe-doped growth in the indium phosphide wafer market size for RF front-ends.

Terahertz IC research highlights the impact of background dopant levels on gain at 300 GHz. The Ferdinand-Braun-Institut's HBTs utilized tailored Zn compensation to achieve a frequency of operation (fT) exceeding 450 GHz, underscoring how substrate doping profiles underpin system-level advances. Demand for ultra-pure, undoped wafers rises in quantum-photonics labs, but price elasticity is limited because such wafers can cost three times as much as standard conductive grades.

The Indium Phosphide Wafer Market Report is Segmented by Diameter (50. 8mm, 76. 2mm, and More), Wafer Doping Type (Undoped Conductive, and More), Application (Photonics and Optical Transceivers, and More), End-User Industry (Telecommunications and Datacom, and More), Manufacturing Technology (VGF-Grown Bulk, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 41.55% of revenue in 2025 and is projected to grow at a 12.41% CAGR. Japan's JX Nippon Mining and Metals provides a vertically integrated supply of purified indium and phosphorous feedstock, while Taiwan's Visual Photonics Epitaxy ramps 100 mm output for datacom lasers. Korea's advanced-materials ecosystem supplies MOCVD consumables, reinforcing regional liquidity. However, export-license complexities from China's raw-material controls create hedging demand for Japanese and Korean producers, who can command price premiums within the indium phosphide wafer market.

North America's share benefits from federal incentives. Coherent's USD 33 million CHIPS grant expands 150 mm line capacity in Texas to safeguard quantum-computing and defense supply chains. Universities such as MIT Lincoln Laboratory prototype InP-on-Si emitters for cryogenic qubit control, seeding future commercial pull. Yet domestic raw material dependence on overseas sources still challenges the cost structure.

Europe leverages deep photonics expertise across Germany and the Netherlands. Ferdinand-Braun-Institut collaborates with Fraunhofer IZM to co-design InP HBTs for terahertz radar, while SMART Photonics pushes foundry services for InP-based PICs. Freiberger Compound Materials supplies VGF wafers with <1e4 cm-2 dislocation density, securing design wins in quantum-communication pilots. EU research grants offset capex, but energy-price volatility narrows margins versus Asian peers, shaping competitive dynamics of the indium phosphide wafer market.

- Sumitomo Electric Semiconductor Materials, Inc.

- AXT, Inc.

- Freiberger Compound Materials GmbH

- Xiamen Powerway Advanced Material Co., Ltd.

- IQE plc

- II-VI Incorporated (Coherent Corp.)

- JX Nippon Mining & Metals Corporation

- Semiconductor Wafer, Inc.

- Visual Photonics Epitaxy Co., Ltd. (VPEC)

- IntellEPI

- VIGO Photonics S.A.

- Western Minmetals (SC) Corporation

- PAM-XIAMEN (Powerway Wafer)

- SHANGHAI FAMOUS TRADE CO., LTD (ZMKJ)

- Atecom Technology Co., Ltd.

- Ding Ten Industrial Inc.

- Logitech Ltd.

- LandMark Optoelectronics Corporation

- Epihouse Optoelectronics Co., Ltd.

- Century Goldray Semiconductor Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High-speed optical transceiver demand (400G/800G/1.6T)

- 4.2.2 5G and emerging 6G backhaul infrastructure rollout

- 4.2.3 Rising consumer SWIR sensing in smartphones and wearables

- 4.2.4 Quantum photonics R&D programs accelerating InP PIC funding

- 4.2.5 Defense IR-imaging re-shoring mandates boosting domestic InP substrates

- 4.2.6 Migration to 6-inch InP substrates to leverage idle GaAs 6-inch lines

- 4.3 Market Restraints

- 4.3.1 High wafer cost versus Si/GaAs alternatives

- 4.3.2 Supply-chain exposure to Ga-/P-export controls and price volatility

- 4.3.3 Mechanical fragility limiting yields beyond 6-inch wafers

- 4.3.4 Si-photonics hybrid laser platforms reducing pure InP wafer volumes

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Diameter

- 5.1.1 50.8 mm

- 5.1.2 76.2 mm

- 5.1.3 100 mm

- 5.1.4 150 mm and Above

- 5.2 By Wafer Doping Type

- 5.2.1 Undoped Conductive

- 5.2.2 N-Type (S / Sn-doped)

- 5.2.3 P-Type (Zn-doped)

- 5.2.4 Semi-insulating (Fe-doped)

- 5.3 By Application

- 5.3.1 Photonics and Optical Transceivers

- 5.3.2 RF and mm-Wave Devices (HEMT, HBT)

- 5.3.3 Photovoltaics and Power Conversion

- 5.3.4 Quantum and Specialty Sensing

- 5.4 By End-user Industry

- 5.4.1 Telecommunications and Datacom

- 5.4.2 Consumer Electronics and Wearables

- 5.4.3 Aerospace and Defense

- 5.4.4 Automotive and Transportation

- 5.4.5 Medical and Life-sciences

- 5.5 By Manufacturing Technology

- 5.5.1 VGF-grown Bulk Wafers

- 5.5.2 LEC/tCZ-grown Bulk Wafers

- 5.5.3 Epitaxial InP-on-Si (Hybrid)

- 5.5.4 MBE/MOCVD Epi-ready Substrates

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Sumitomo Electric Semiconductor Materials, Inc.

- 6.4.2 AXT, Inc.

- 6.4.3 Freiberger Compound Materials GmbH

- 6.4.4 Xiamen Powerway Advanced Material Co., Ltd.

- 6.4.5 IQE plc

- 6.4.6 II-VI Incorporated (Coherent Corp.)

- 6.4.7 JX Nippon Mining & Metals Corporation

- 6.4.8 Semiconductor Wafer, Inc.

- 6.4.9 Visual Photonics Epitaxy Co., Ltd. (VPEC)

- 6.4.10 IntellEPI

- 6.4.11 VIGO Photonics S.A.

- 6.4.12 Western Minmetals (SC) Corporation

- 6.4.13 PAM-XIAMEN (Powerway Wafer)

- 6.4.14 SHANGHAI FAMOUS TRADE CO., LTD (ZMKJ)

- 6.4.15 Atecom Technology Co., Ltd.

- 6.4.16 Ding Ten Industrial Inc.

- 6.4.17 Logitech Ltd.

- 6.4.18 LandMark Optoelectronics Corporation

- 6.4.19 Epihouse Optoelectronics Co., Ltd.

- 6.4.20 Century Goldray Semiconductor Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment