PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035098

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035098

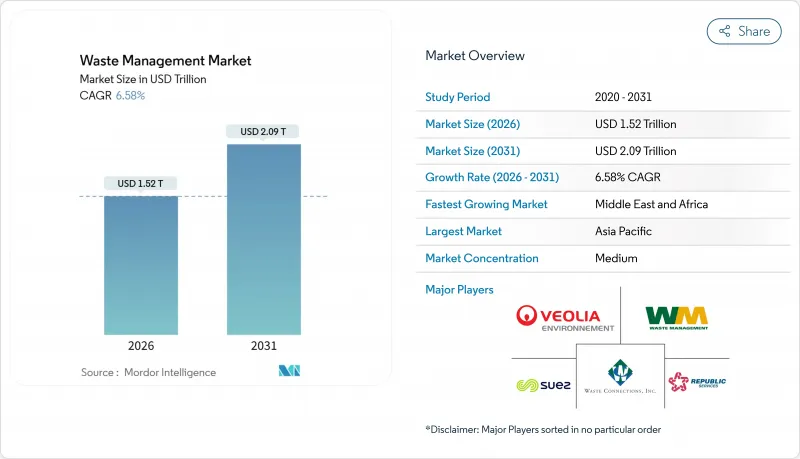

Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Waste Management Market size is estimated at USD 1.52 trillion in 2026, and is expected to reach USD 2.09 trillion by 2031, at a CAGR of 6.58% during the forecast period (2026-2031).

The opening shift from disposal-centric operations toward resource recovery underscores this market size and growth trajectory. Mandatory recycled-content laws in the European Union and several U.S. states, broader extended-producer-responsibility (EPR) mandates across Asia-Pacific, and Scope-3 waste reporting tied to corporate science-based targets are accelerating capital flows into advanced sorting, chemical recycling, and waste-to-energy infrastructure. Landfill services still anchor revenue, yet operators are pivoting as recycling and resource-recovery lines attract 6.80% annual growth, supported by artificial-intelligence robotics that deliver 99% purity at material-recovery facilities. Asia-Pacific remains the revenue epicenter, but sovereign-wealth-fund financing of waste-to-energy projects is lifting the Middle East and Africa to the fastest regional CAGR (9.1%). Competitive pressure is intensifying as energy majors and digital-sorting start-ups push incumbents to bundle collection, treatment, and renewable-fuel production within integrated offerings.

Global Waste Management Market Trends and Insights

Mandatory Recycled-Content Laws for Plastic Packaging (EU, US)

Legislation such as the European Union's Packaging and Packaging Waste Regulation 2025/40 and California's Senate Bill 54 compels brand owners to integrate defined shares of post-consumer resin in all primary packaging, driving multi-year offtake contracts with mechanical and chemical recyclers. These statutes tighten quality standards, prompting upgrades in optical-sorter lines and investment in depolymerization units capable of food-grade outputs. The International Energy Agency estimates that meeting statutory targets could divert 15 million metric tons of plastic from landfills annually by 2030, provided collection systems keep pace. Larger recyclers equipped with ISO 9001 and ISO 14001 certifications are absorbing compliance premiums, while smaller facilities lacking traceability tools struggle to remain viable. Penalties for non-compliance escalate, and procurement teams increasingly reward operators offering guaranteed purity and long-term capacity.

EPR Expansion to Textiles & Electronics Across APAC

Singapore, Hong Kong, and India broadened EPR frameworks during 2024-2025, shifting waste-collection and treatment costs upstream to product manufacturers. Penalties now reach USD 74,000 per violation in Singapore, and India's revised targets demand 70% take-back volumes by 2027, sharpening financial incentives for design-for-disassembly. Formal collection remains below 20% in much of Asia, so compliance pushes brand owners to co-fund municipal drop-off points and reverse-logistics hubs. These policies channel private capital into electronics-dismantling centers and high-throughput textile shredders, expanding addressable revenue pools beyond packaging. Industry analysts expect more jurisdictions to replicate EPR schemes as landfill capacity tightens and informal recycling draws regulatory scrutiny.

High Interest Rates Weakening PPP Financing for Recycling Plants

Global monetary tightening pushed public-private partnership (PPP) waste projects down 25% in 2024, with investment falling to USD 6.8 billion as debt-service ratios worsened. Canceled tenders in South Africa and postponed treatment plants in Indonesia illustrate how higher capital costs deter sponsors from long-tenor concessions. Municipalities lacking credit enhancements must now offer higher gate-fee guarantees or risk facility delays, extending landfill lifespans and undermining diversion targets. The financing squeeze also raises barriers for small technology providers that rely on project finance for scale-up. Unless interest rates ease, many emerging-market recycling projects will hinge on concessional or blended-finance structures.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Science-Based Targets Requiring Waste Scope-3 Reporting

- Sustainability-Linked Bonds Financing Waste Infrastructure in Emerging Markets

- Labor Shortages Inflating Collection Wages in OECD Countries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial streams are gaining prominence even though residential waste still accounted for 46.54% of revenue in 2025, the largest share within the Waste Management market share landscape. The segment's faster 8.3% CAGR stems from manufacturers installing on-site neutralization units to satisfy stricter occupational-safety rules such as OSHA's 2024 Hazard Communication Standard revision. Many plants now couple closed-loop water systems with hazardous-waste pretreatment, reducing off-site hauling volumes and permitting costs. Electronics assemblers in Malaysia and Vietnam added acid-scrubbing reactors in 2025 to comply with European import audits, illustrating how downstream buyers dictate upstream waste behavior. Automotive suppliers in Mexico deployed solvent-recovery stills that recaptured 95% of isopropanol, cutting material expense and avoiding flammable-waste surcharges. These examples show that compliance investments are lining up with cost avoidance, a combination that sustains segment growth even when commodity prices dip.

Over the forecast horizon, industrial operators will sign multi-year "net-zero waste" service contracts that embed pay-for-performance clauses rather than simple tonnage fees, a structure already piloted by semiconductor fabs in Arizona and Singapore. Specialized hazardous-waste firms displaying ISO 14001 credentials are therefore winning bids over generalist haulers that lack laboratory testing and manifest-tracking software. Rising capital expenditure pushes some smaller electroplating shops to form cooperatives that share on-site treatment units, echoing pooled effluent plants adopted by Indian textile clusters. The Waste Management market is responding with modular mobile separators that treat emulsified oils at the generator's dock, eliminating road transport and the liability it entails. As credit providers increasingly incorporate waste metrics into ESG loan covenants, industrial producers unwilling to disclose diversion progress are paying higher interest spreads, reinforcing the segment's push toward certified vendors.

The Waste Management Market Report is Segmented by Source (Residential, Commercial [Retail, Office, Etc. ], Industrial and More), by Service Type (Collection, Transportation, Sorting & Segregation and Disposal/Treatment), by Waste Type (Municipal Solid Waste, E-Waste and More), and by Geography (North America, Europe and More). The Report Offers Market Size and Forecasts in Value (USD) for all the Above Segments.

Geography Analysis

Asia-Pacific held 56% of 2025 global revenue, giving it the largest regional slice of the Waste Management market share and positioning it as the anchor for volume growth. China's revised Solid Waste Law imposes fines of USD 140,000 for illegal dumping, accelerating investment in optical sorters and waste-to-energy boilers that handle rising urban tonnage. India's Swachh Bharat Mission 2.0 disbursed USD 1.7 billion across 4,700 cities to scale source segregation and composting, while Japanese municipalities collectively target a 50% cut in final disposal by 2030, supported by mandatory take-back for textiles and smartphones. Private equity funds in Singapore are buying minority stakes in Malaysian recyclers, betting on regional logistics hubs that consolidate high-value plastics before shipment to local chemical depolymerization plants. Corporations exporting into Europe increasingly depend on compliant recovery certificates issued by licensed operators in Vietnam and Thailand, creating new revenue channels for firms that obtain both EU REACH and local permits.

The Middle East and Africa are the fastest-growing territories, expanding at a 9.1% CAGR to 2031 as sovereign wealth funds co-finance integrated waste campuses. Saudi Arabia's USD 1.8 billion joint venture with Averda exemplifies how public capital aligns with policy mandates targeting 70% diversion by 2030. The United Arab Emirates banned single-use plastics in 2024 and now grants fee holidays to operators installing advanced material-recovery facilities in Abu Dhabi's KEZAD zone. Egypt leverages World Bank loans to rehabilitate landfill cells and establish composting lines that process Cairo's food waste into agricultural amendments sold under guaranteed off-take agreements. South Africa's extended producer responsibility regulations, effective 2024, generated USD 90 million in compliance fees during their first full year, financing collection cooperatives in underserved townships.

North America and Europe remain technologically mature yet far from complacent. California and Washington State passed patchwork recycled-content statutes, prompting brand owners to lock in supply via 10-year contracts that favor U.S. recyclers offering blockchain-verified traceability. German and Dutch municipalities launched auction mechanisms where operators bid diversion percentages instead of gate-fee discounts, aligning incentives with circular-economy goals. Brazil, Chile, and Colombia trail in formal infrastructure but are closing gaps through sustainability-linked bond issuances, which subsidize fleet modernization and MRF upgrades. As legislation restricting waste exports widens, cross-border movements shrink, reinforcing regional self-sufficiency and pushing operators to optimize domestic treatment capacity.

- Veolia Environment SA

- Waste Management Inc.

- Suez SA

- Republic Services Inc.

- Waste Connections Inc.

- Clean Harbors Inc.

- Covanta Holding Corporation

- Biffa Group

- Remondis SE & Co. KG

- Stericycle Inc.

- GFL Environmental Inc.

- FCC Environment

- Cleanaway Waste Management Ltd

- Hitachi Zosen Inova AG

- Sims Limited

- Renewi PLC

- Averda

- Daiseki Co. Ltd

- Tatweer Environmental Services

- Waste Pro USA

- Recology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Mandatory Recycled-Content Laws for Plastic Packaging (EU, US)

- 4.1.2 EPR Expansion to Textiles & Electronics Across APAC

- 4.1.3 Corporate Science-Based-Targets Requiring Waste Scope-3 Reporting

- 4.1.4 Sustainability-Linked Bonds Financing Waste Infrastructure in Emerging Markets

- 4.1.5 Green-Hydrogen Projects Using MSW Feedstock

- 4.1.6 AI-Driven Robotics Achieving 99 % MRF Purity, Cutting Sorting Costs

- 4.2 Market Restraints

- 4.2.1 Labour Shortages Inflating Collection Wages in OECD Countries

- 4.2.2 High Interest Rates Weakening PPP Financing for Recycling Plants

- 4.2.3 Import Bans on Solid Waste (e.g., China) Shrinking Disposal Options

- 4.2.4 Absence of End-of-Waste Rules for Recycled Carbon Fibre Limiting Adoption

- 4.3 Value / Supply-Chain Analysis

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Startup Ecosystem Analysis

- 4.7 Key Emerging Trends

- 4.8 Impact of Geopolitical Shocks

- 4.9 Industry Attractiveness - Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Threat of Substitute Products

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Source

- 5.1.1 Residential

- 5.1.2 Commercial (retail, office, etc.)

- 5.1.3 Industrial

- 5.1.4 Medical (Health and Pharmaceutical)

- 5.1.5 Construction & Demolition

- 5.1.6 Others (institutional, agricultural, etc)

- 5.2 By Service Type

- 5.2.1 Collection, Transportation, Sorting & Segregation

- 5.2.2 Disposal / Treatment

- 5.2.2.1 Landfill

- 5.2.2.2 Recycling & Resource Recovery

- 5.2.2.3 Incineration & Waste-to-Energy

- 5.2.2.4 Others (Chemical Treatment, Composting, etc.)

- 5.2.3 Others (Consulting, Audit & Training, etc.)

- 5.3 By Waste Type

- 5.3.1 Municipal Solid Waste

- 5.3.2 Industrial Hazardous Waste

- 5.3.3 E-waste

- 5.3.4 Plastic Waste

- 5.3.5 Biomedical Waste

- 5.3.6 Construction & Demolition Waste

- 5.3.7 Agricultural Waste

- 5.3.8 Other Specialized Waste (radio active, etc)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.4.3.6 Australia

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 Europe

- 5.4.4.1 United Kingdom

- 5.4.4.2 Germany

- 5.4.4.3 France

- 5.4.4.4 Italy

- 5.4.4.5 Spain

- 5.4.4.6 Russia

- 5.4.4.7 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.4.8 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.4.9 Rest of Europe

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Turkey

- 5.4.5.5 South Africa

- 5.4.5.6 Egypt

- 5.4.5.7 Nigeria

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)}

- 6.3.1 Veolia Environment SA

- 6.3.2 Waste Management Inc.

- 6.3.3 Suez SA

- 6.3.4 Republic Services Inc.

- 6.3.5 Waste Connections Inc.

- 6.3.6 Clean Harbors Inc.

- 6.3.7 Covanta Holding Corporation

- 6.3.8 Biffa Group

- 6.3.9 Remondis SE & Co. KG

- 6.3.10 Stericycle Inc.

- 6.3.11 GFL Environmental Inc.

- 6.3.12 FCC Environment

- 6.3.13 Cleanaway Waste Management Ltd

- 6.3.14 Hitachi Zosen Inova AG

- 6.3.15 Sims Limited

- 6.3.16 Renewi PLC

- 6.3.17 Averda

- 6.3.18 Daiseki Co. Ltd

- 6.3.19 Tatweer Environmental Services

- 6.3.20 Waste Pro USA

- 6.3.21 Recology

7 Market Opportunities & Future Outlook