PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035115

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035115

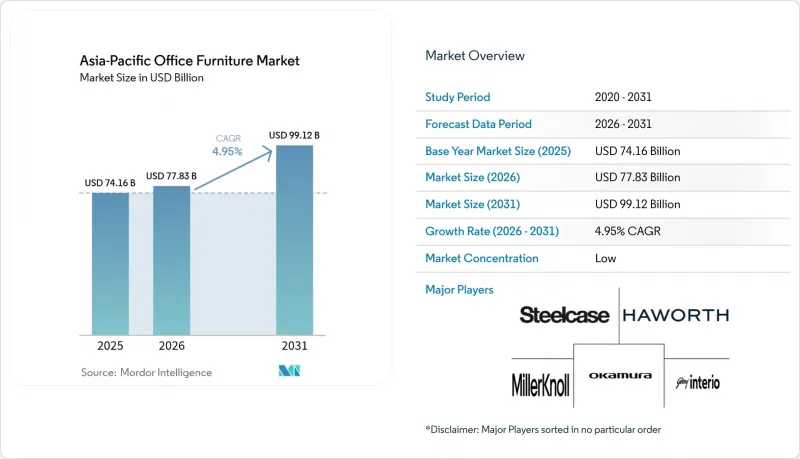

Asia-Pacific Office Furniture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Asia-Pacific Office Furniture market size in 2026 is estimated at USD 77.83 billion, growing from 2025 value of USD 74.16 billion with 2031 projections showing USD 99.12 billion, growing at 4.95% CAGR over 2026-2031.

This growth places the Asia-Pacific office furniture market size at the core of the region's return-to-office revival and hybrid workplace transformation. The rise in the in-person workforce share between 2023 and 2024 has prompted enterprises to reconfigure floor plans, invest in AI-driven smart desk solutions, and align with increasingly stringent indoor air quality regulations. Corporations are reallocating capital from remote-work stipends to wellness-centric chairs and touch-free workstation systems, while government infrastructure programs and foreign direct investment funnel new projects into Tier II and emerging satellite cities. Furniture producers manage volatility in wood and metal costs by diversifying supplier bases and signing long-term contracts, and they capture margin through circular-economy leasing that meets ESG scorecard requirements. Despite supply-chain complexity, the Asia-Pacific office furniture market benefits from resilient regional GDP, rising co-working penetration, and a creative push toward modular, data-rich products that satisfy both real-estate efficiency and employee experience goals.

Asia-Pacific Office Furniture Market Trends and Insights

Post-pandemic Expansion of Co-working Spaces

The Asia-Pacific region, which hosts the highest number of co-working hubs globally, is projected to witness operators expanding their presence from 5,889 venues to over 10,000 within the next decade. In India, the flexible workspace segment experienced a reduction in vacancy rates, while in Singapore, co-working spaces accounted for 4.2% of the total office stock, accompanied by an upward trend in average desk prices. Modular desks, lightweight chairs, and reconfigurable storage allow landlords to convert suites overnight for new tenants, keeping the Asia-Pacific office furniture market on a steady growth climb. Operators prefer furnishings that break down quickly for relocation, reinforcing demand for tool-free joints and quick-lock fittings. Cloud-connected smart desks help manage booking systems, so asset owners can monetize under-utilized zones and prove utilization to investors. Co-working's service-oriented mindset also accelerates furniture-leasing contracts that bundle maintenance and eventual take-back, cementing a subscription revenue layer for manufacturers.

Government-led Infrastructure Investments in Commercial Real Estate

India's Smart Cities Mission, Make in India incentives, and foreign developer commitments such as Sumitomo Realty's USD 3.34 billion Mumbai project expand the Asia-Pacific office furniture market by opening fresh corridors of commercial space. Tier II cities benefit from upgraded metro links and IT parks, widening the customer base beyond Bengaluru and Mumbai. Southeast Asia's 4.6% 2024 GDP growth, coupled with favourable demographics, underpins new office-tower pipelines that require full fit-outs. Builders often bundle furniture procurement with design-build contracts, accelerating volume orders even before occupancy. As regional governments court international tenants, premium ESG standards are embedded in tender documents, steering procurement to certified low-VOC and recyclable products. These long-cycle developments sustain baseline demand even if short-term real-estate cycles soften elsewhere.

Volatility in Raw-material Prices

Vietnam's USD 289 million office-furniture export surge in 2024 underscored its reliance on timber inputs that swing with global demand. Indonesia's SVLK Plus verification elevates transparency but adds audit fees, while fluctuations in steel futures complicate cost forecasts for metal bases. Manufacturers hedge with multi-year supply contracts and mixed-material designs, yet margin compression still trickles through to price-sensitive clients. Larger brands absorb shocks through scale and digital demand-planning systems that reroute orders to alternate plants. Persistent cost shifts may defer discretionary upgrades, especially among SMEs that lack lease-back options.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Ergonomic & Wellness-centric Workstations

- Adoption of Modular Furniture to Optimise High-rent Urban Micro-offices

- Slowdown in Commercial Real Estate Development in Tier-1 Chinese Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wood continued to hold a commanding 55.78% of the Asia-Pacific office furniture market share in 2025 because buyers associate solid timber with executive status, long service life, and a warmer aesthetic than laminate substitutes. Vietnamese exporters delivered USD 289 million of wood-office furniture last year, taking advantage of upgraded kiln-drying capacity and U.S. market demand. Yet plastics exhibit the fastest 10.05% CAGR as furniture engineers incorporate recycled polypropylene and bio-PET to cut freight weights and lower embodied carbon. Metal subframes remain critical for premium height-adjustable desks that support heavier monitors and cable runs, although aluminium and thin-wall steel tubing help shrink raw-material tonnage.

Emerging composites, such as bamboo fibre boards and recycled ocean-plastic panels, provide ESG-focused clients with storytelling value, allowing suppliers to differentiate amid commodity timber. The Asia-Pacific office furniture market size tied to sustainable lines rises each tender cycle as procurement audits include chain-of-custody certificates. BIFMA LEVEL and Forest Stewardship Council validations bolster bidder scores, and vendors add QR-code traceability on drawer bottoms. Wood costs, however, are vulnerable to shipping bottlenecks and phytosanitary restrictions; plastic pellet prices fluctuate with crude-oil movements, demanding agile costing models. Over the forecast horizon, wood's share is projected to erode modestly as corporate design guidelines shift toward lighter, easily disassembled components that fit closed-loop logistics.

Asia-Pacific Office Furniture Market is Segments Into Material (Wood, Metal, Plastic, Other Materials), by Product (Meeting Chairs, Lounge Chairs, and Other), by Distribution Channel (Multi-Branded Stores, Specialty Stores, and Other), by Geography (India, China, and Other). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Steelcase Inc.

- Okamura Corporation

- Haworth Inc.

- MillerKnoll (Herman Miller)

- KOKUYO Co., Ltd.

- Godrej Interio

- HNI Corporation

- Fursys Group

- Sunon Group

- UE Furniture

- Zuoyou Furniture

- Featherlite

- Zenith Interiors

- Itoki Corporation

- Quama Furniture

- Li & Fung Furniture

- UB Office Systems

- Kian Furniture

- Teknion Corp.

- IKEA (Inter IKEA Group)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Post-pandemic expansion of co-working spaces

- 4.2.2 Government-led infrastructure investments in commercial real estate

- 4.2.3 Rising demand for ergonomic & wellness-centric workstations

- 4.2.4 Adoption of modular furniture to optimise high-rent urban micro-offices

- 4.2.5 Corporate ESG mandates driving shift to circular-economy furniture leasing

- 4.2.6 Digital transformation of workplace planning via AI-driven layout tools

- 4.3 Market Restraints

- 4.3.1 Volatility in raw-material prices (wood & metal)

- 4.3.2 Slow-down in commercial real-estate development in tier-1 Chinese cities

- 4.3.3 Stringent indoor-air-quality certifications increasing compliance costs

- 4.3.4 Rising logistics and cross-border shipping costs post-RCEP implementation delays

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Competitive Rivalry

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Threat of New Entrants

5 Market Size & Growth Forecasts

- 5.1 By Material

- 5.1.1 Wood

- 5.1.2 Metal

- 5.1.3 Plastics

- 5.1.4 Other Materials

- 5.2 By Product

- 5.2.1 Meeting Chairs

- 5.2.2 Lounge Chairs

- 5.2.3 Swivel Chairs

- 5.2.4 Office Tables

- 5.2.5 Storage Cabinets

- 5.2.6 Desks

- 5.3 By Distribution Channel

- 5.3.1 Multi-branded Stores

- 5.3.2 Specialty Stores

- 5.3.3 Online Platforms

- 5.3.4 Other Distribution Channels

- 5.4 By Geography

- 5.4.1 India

- 5.4.2 China

- 5.4.3 Japan

- 5.4.4 Australia

- 5.4.5 South Korea

- 5.4.6 South-East Asia

- 5.4.6.1 Singapore

- 5.4.6.2 Malaysia

- 5.4.6.3 Thailand

- 5.4.6.4 Indonesia

- 5.4.6.5 Vietnam

- 5.4.6.6 Philippines

- 5.4.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Steelcase Inc.

- 6.4.2 Okamura Corporation

- 6.4.3 Haworth Inc.

- 6.4.4 MillerKnoll (Herman Miller)

- 6.4.5 KOKUYO Co., Ltd.

- 6.4.6 Godrej Interio

- 6.4.7 HNI Corporation

- 6.4.8 Fursys Group

- 6.4.9 Sunon Group

- 6.4.10 UE Furniture

- 6.4.11 Zuoyou Furniture

- 6.4.12 Featherlite

- 6.4.13 Zenith Interiors

- 6.4.14 Itoki Corporation

- 6.4.15 Quama Furniture

- 6.4.16 Li & Fung Furniture

- 6.4.17 UB Office Systems

- 6.4.18 Kian Furniture

- 6.4.19 Teknion Corp.

- 6.4.20 IKEA (Inter IKEA Group)

7 Market Opportunities & Future Outlook

- 7.1 Green-certified furniture aligned with Asia-Pacific carbon-neutrality roadmaps

- 7.2 AI-integrated smart desking systems for hybrid-work monitoring