PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035116

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035116

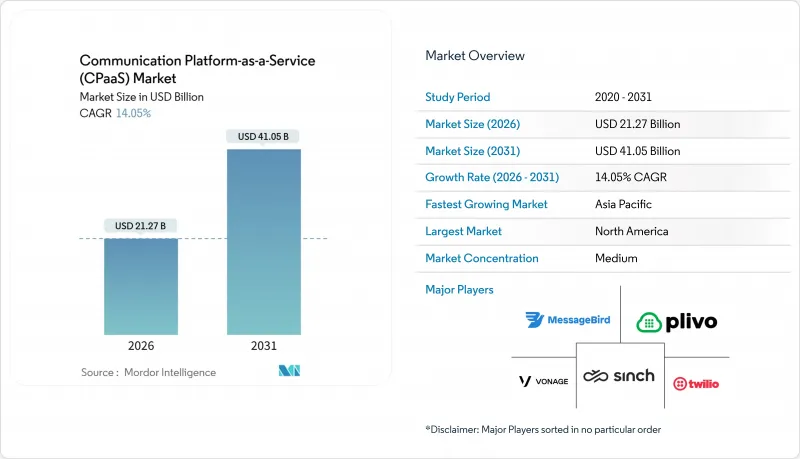

Communication Platform-as-a-Service (CPaaS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Communication Platform-as-a-Service market size is USD 21.27 billion in 2026, and it is projected to reach USD 41.05 billion by 2031, advancing at a 14.05% CAGR.

Heightened demand for embedded voice, messaging, and video is reshaping customer-experience architectures, encouraging firms to swap monolithic contact-center suites for API-first, composable layers that plug directly into digital workflows. Three catalysts drive this shift: stronger authentication rules such as PSD2 in Europe, which require programmable one-time-password flows; the migration of consumers to over-the-top chat channels that enterprises must now unify under a single vendor relationship; and the arrival of 5G network slicing that lets operators carve low-latency lanes for mission-critical workloads. Competitive intensity is rising, yet no vendor controls more than 15%, so the Communication Platform-as-a-Service market still offers white-space opportunities for specialists addressing vertical gaps or regional data-sovereignty requirements.

Global Communication Platform-as-a-Service (CPaaS) Market Trends and Insights

OTT Chat-Centric Engagement

WhatsApp Business API alone now handles more than 100 billion messages per month, a scale that forced Meta to adopt conversation-based pricing in July 2025. Enterprises flock to platforms that maintain turnkey integrations with WhatsApp, Telegram, LINE, WeChat, and Viber because each channel carries unique approval workflows and content rules. Retailers and e-commerce players use these integrations to automate order confirmations, shipping updates, and returns entirely within chat threads, trimming web-portal dependencies. CPaaS vendors incapable of sustaining multi-OTT support risk falling back to commoditized SMS delivery. Even so, data-localization rules in India and Brazil compel providers to keep regional hosting nodes, adding complexity and cost.

Low-Code / No-Code CPaaS Build-Outs

Visual flow builders such as Twilio Studio let non-technical staff design appointment-reminder calls or abandoned-cart campaigns in minutes, removing the need for dedicated developers. Rapid prototyping shortens sales cycles for SMEs and lets large enterprises pilot engagement ideas before allocating engineering budgets. Healthcare clerical workers, for instance, can set up post-consultation SMS follow-ups without IT involvement. The democratization of orchestration tools is broadening the Communication Platform-as-a-Service market by lowering entry barriers, particularly in emerging Asia Pacific where small businesses face acute developer shortages. Compliance with spam-consent rules such as the TCPA in the United States still requires guardrails, so leading vendors embed opt-in management inside their builders.

Country-Level A2P SMS Surcharges

Operators in India, the United States, and much of Europe have imposed fees of USD 0.005-0.02 per message on enterprise SMS, eroding margins by up to 25 percentage points for high-volume traffic. Registration systems such as India's blockchain-based DLT platform and the U.S. 10DLC framework require every template to be pre-approved, lengthening onboarding cycles for time-sensitive alerts. Vendors are nudging customers toward RCS or OTT channels where surcharges do not apply, but fragmented handset support outside developed markets slows migration.

Other drivers and restraints analyzed in the detailed report include:

- AI-Powered CPaaS Automation and Analytics

- Telco 5G-Anchored CPaaS Innovation

- Enterprise Data-Residency Mandates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pure-play specialists captured a 42.44% revenue slice of the Communication Platform-as-a-Service market in 2025. Their growth stems from rapid release cadences, unified APIs, and carrier-agnostic routing that speed global expansion. However, telco-driven offerings exhibit the segment's quickest advance at a 14.67% CAGR to 2031, riding bundled enterprise mobility contracts and direct network access that eliminates a hop in the signaling path.

In practice, multinational banks often dual-source, using a pure-play vendor for omnichannel innovation and a carrier subsidiary for latency-critical authentication inside domestic borders. Hyperscale clouds are now embedding native messaging and voice, narrowing switching costs further. Consequently, the Communication Platform-as-a-Service market is tilting toward hybrid consumption, where enterprises mix API-rich innovation from independents with regulated-workload delivery from mobile-network operators.

SMS and traditional A2P traffic retained 39.21% share in 2025, in part because every handset can receive a text even when data connectivity is unreliable. Yet Apple's iOS 18 added native RCS support in 2024, clearing a major adoption hurdle and driving a 14.98% CAGR for RCS through 2031.

Retailers now embed product carousels and quick-reply buttons inside RCS messages, achieving tap-through rates triple that of plain-text SMS. Enterprises that move early gain richer engagement metrics without forcing customers to install standalone apps. Still, security-sensitive organizations retain voice and interactive-voice-response flows where verbal consent remains mandatory, confirming that a channel portfolio rather than a single medium underpins the Communication Platform-as-a-Service market.

The Communication Platform-As-A-Service Report is Segmented by CPaaS Type (Pure-Play, Enterprise-Grade, and More), Communication Channel (SMS and A2P Messaging, and More), API Service (Messaging, and More), Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Enterprise Size (SMEs, and Large Enterprises), End-User Vertical (IT and Telecom, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 36.01% of 2025 revenue due to deep cloud penetration, a dense start-up ecosystem, and proximity to hyperscalers. Regional buyers prioritize AI-driven analytics and omnichannel orchestration, translating into premium ARPU that props up vendor profitability.

Asia Pacific is the growth engine, forecast to surge at a 15.90% CAGR to 2031 as smartphone-first economies in India, China, and Southeast Asia leapfrog desktop web to mobile engagement. India's Unified Payments Interface processed 11.4 billion monthly transactions by late 2025, each triggering real-time alerts that inflate baseline traffic on domestic CPaaS platforms.

Europe retains a solid base order flow anchored in PSD2 authentication, but growth moderates after the initial compliance wave. South America, the Middle East and Africa trail in absolute revenue, though Saudi Arabia and the United Arab Emirates are accelerating due to public-sector digitization. In Africa, coverage gaps mean SMS dominates for now, sustaining a revenue floor for legacy channels inside the Communication Platform-as-a-Service market.

- Twilio Inc.

- Vonage Holdings Corp.

- Sinch AB

- Infobip Ltd.

- MessageBird B.V.

- Bandwidth Inc.

- Plivo Inc.

- 8x8 Inc.

- Voximplant (Zingaya Inc.)

- Voxvalley Technologies

- IntelePeer Cloud Communications

- Wazo Communication Inc.

- Avaya Inc.

- AT&T Inc.

- Mitel Networks Corporation

- Telestax

- CM.com N.V.

- Kaleyra Inc.

- Route Mobile Ltd.

- Telnyx LLC

- RingCentral Inc.

- Cisco Systems Inc.

- Link Mobility Group ASA

- TeleSign Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 OTT Chat-Centric Engagement

- 4.2.2 Low-Code / No-Code CPaaS Build-Outs

- 4.2.3 PSD2-Driven Programmable Messaging

- 4.2.4 Telco 5G-Anchored CPaaS Innovation

- 4.2.5 AI-Powered CPaaS Automation and Analytics

- 4.2.6 IoT and Edge-Integrated CPaaS Workloads

- 4.3 Market Restraints

- 4.3.1 Country-Level A2P SMS Surcharges

- 4.3.2 Enterprise Data-Residency Mandates

- 4.3.3 Stricter Anti-Spam and Consent Regulations

- 4.3.4 Growing Messaging/API Security and Fraud Risk

- 4.4 Industry Value-Chain Analysis

- 4.5 Industry Ecosystem Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.7.1 Serverless Deployments

- 4.7.2 Machine-Learning and AI-Enabled Contextual Routing

- 4.7.3 Omnichannel Conversational Bots

- 4.7.4 Advanced Security and Privacy Paradigms (Zero-Trust, STIR/SHAKEN)

- 4.8 Impact of Macroeconomic Factors on the Market

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Bargaining Power of Suppliers

- 4.9.4 Threat of Substitutes

- 4.9.5 Competitive Rivalry

- 4.10 Pricing and Business-Model Analysis

- 4.11 Comparative Analysis of CPaaS vs UCaaS vs Traditional Deployments

- 4.12 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By CPaaS Type

- 5.1.1 Pure-Play CPaaS

- 5.1.2 Enterprise-Grade CPaaS

- 5.1.3 Telco-Driven CPaaS

- 5.1.4 Service-Provider-Based CPaaS

- 5.1.5 Hybrid CPaaS

- 5.2 By Communication Channel

- 5.2.1 SMS and A2P Messaging

- 5.2.2 Voice and IVR

- 5.2.3 Video and WebRTC

- 5.2.4 Email

- 5.2.5 Push and In-App Notifications

- 5.2.6 Rich Communication Services (RCS) Messaging

- 5.3 By API Service

- 5.3.1 Messaging APIs

- 5.3.2 Voice APIs

- 5.3.3 Video APIs

- 5.3.4 Authentication and Security APIs

- 5.3.5 Rich Communication Services (RCS) APIs

- 5.4 By Deployment Model

- 5.4.1 Public Cloud

- 5.4.2 Private Cloud

- 5.4.3 Hybrid Cloud

- 5.5 By Enterprise Size

- 5.5.1 Small and Medium Enterprises (SMEs)

- 5.5.2 Large Enterprises

- 5.6 By End-User Vertical

- 5.6.1 IT and Telecom

- 5.6.2 BFSI

- 5.6.3 Retail and E-commerce

- 5.6.4 Healthcare

- 5.6.5 Travel and Hospitality

- 5.6.6 Logistics and Transportation

- 5.6.7 Government and Public Sector

- 5.6.8 Education

- 5.6.9 Other End-User Verticals

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 India

- 5.7.4.5 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 United Arab Emirates

- 5.7.5.1.2 Saudi Arabia

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Funding, Partnerships)

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Twilio Inc.

- 6.4.2 Vonage Holdings Corp.

- 6.4.3 Sinch AB

- 6.4.4 Infobip Ltd.

- 6.4.5 MessageBird B.V.

- 6.4.6 Bandwidth Inc.

- 6.4.7 Plivo Inc.

- 6.4.8 8x8 Inc.

- 6.4.9 Voximplant (Zingaya Inc.)

- 6.4.10 Voxvalley Technologies

- 6.4.11 IntelePeer Cloud Communications

- 6.4.12 Wazo Communication Inc.

- 6.4.13 Avaya Inc.

- 6.4.14 AT&T Inc.

- 6.4.15 Mitel Networks Corporation

- 6.4.16 Telestax

- 6.4.17 CM.com N.V.

- 6.4.18 Kaleyra Inc.

- 6.4.19 Route Mobile Ltd.

- 6.4.20 Telnyx LLC

- 6.4.21 RingCentral Inc.

- 6.4.22 Cisco Systems Inc.

- 6.4.23 Link Mobility Group ASA

- 6.4.24 TeleSign Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment