PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035121

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035121

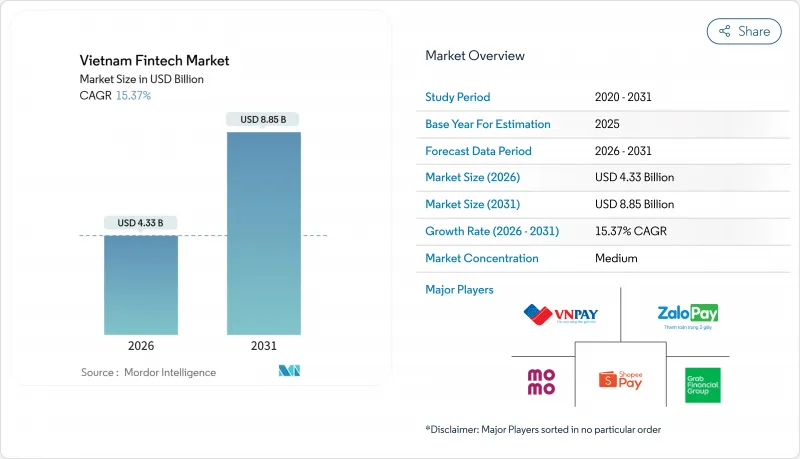

Vietnam Fintech - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Vietnam fintech market size is USD 4.33 billion in 2026 and is projected to reach USD 8.85 billion by 2031 at a 15.37% CAGR.

This growth is fueled by a robust domestic digital payment ecosystem, which saw significant year-on-year expansion. Vietnam introduced a fintech sandbox, allowing innovative financial products to scale in a controlled environment. The shift toward cashless payments is evident, with 5.5 billion cashless transactions recorded in Q1 2025, facilitated by NAPAS 247's real-time QR infrastructure that lowers merchant acceptance costs and expands digital use cases. Expanding financial inclusion has also contributed to market growth, as more individuals gain access to bank accounts. Digital platforms and banks have further accelerated adoption by providing accessible and user-friendly fintech solutions. The market is strengthened by growing consumer trust in digital payments, supported by secure and well-regulated systems. Overall, Vietnam's fintech landscape is poised for sustained growth, driven by technology adoption, regulatory support, and a broadening financial infrastructure.

Vietnam Fintech Market Trends and Insights

High Smartphone & Internet Penetration

Smartphone and internet penetration are a structural advantage for the Vietnam fintech market, with widespread connectivity enabling mobile-first service delivery across payments, lending, investments, and insurance. The Ministry of Information and Communications has driven household fiber and 4G coverage to high levels, which has reduced access friction for real-time transactions and account onboarding. National planning targets 5G availability at scale by 2030, which supports the next wave of low-latency fintech use cases like instant credit decisioning and dynamic QR payments. Platform growth shows the effect of this base, as leading wallets and bank apps scaled rapidly on the back of digital infrastructure and user readiness. As participation widens, hybrid models that blend digital channels with local agent support continue to expand reach in areas where digital literacy is still maturing, keeping the Vietnam fintech market inclusive while sustaining growth.

Government Cashless Roadmap & National Digital Transformation Program

The cashless roadmap and the National Digital Transformation Program have accelerated the Vietnam fintech market by pushing digital payments into the mainstream of commerce and public services. Fiscal and administrative measures, including requirements that link deductions and benefits to non-cash evidence, have created persistent incentives for businesses to digitize payment flows and record-keeping. National database integration prioritized by the government is improving the quality of identity, tax, and credit data that underpin digital onboarding, underwriting, and fraud control. Banks have reinforced these gains by rolling out biometric ID-based authentication at scale, which has improved security outcomes and reduced fraud exposure alongside compliance with new verification rules. As payroll, pensions, and subsidy distribution migrate to digital channels through local pilots, consumer switching costs rise, and platform lock-in strengthens, supporting durable adoption across the Vietnam fintech market.

Low Financial Literacy & Trust in Rural Areas

Over 70% of the population lives outside the largest cities, which means the Vietnam fintech market depends on outreach models that address gaps in confidence, awareness, and product understanding. Government programs focused on financial inclusion and digital transformation continue to push acceptance infrastructure and e-services deeper into rural districts. Payment providers, banks, and agents are testing hybrid delivery that combines mobile onboarding with local assistance to bridge literacy constraints and build trust. Greater coverage of identity services, including chip-based IDs and biometric verification, is also reducing fraud risk and improving confidence in digital channels. A sustained focus on education, grievance redressal, and agent quality is likely to determine how quickly advanced products like investments and insurance scale beyond major urban corridors in the Vietnam fintech market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Middle-Class Demand for Convenient Financial Services

- Expansion of NAPAS 247 Real-Time QR Rail

- Fragmented KYC Rules Across Ministries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital payments held a commanding 71.73% share in 2025, while insurtech is forecast to be the fastest-growing service line at a 31.28% CAGR through 2031, underscoring the depth and breadth of the Vietnam fintech market. In parallel, the regulatory sandbox enables controlled pilots in P2P lending, credit scoring, and open APIs, which will support lending and data-led models as they transition from proof of concept to scaled deployment. Neobanking is advancing through bank-backed digital brands and partnerships with technology players that shorten the path from customer acquisition to product activation. Digital investments are expanding through fractional equity and automated saving tools, as platforms adapt to rising retail wealth and the need for low-barrier entry. Insurtech's growth is leveraging embedded distribution and digital channels, which aligns with the policy environment that has supported greater foreign investment into the sector and modernization of distribution.

From a growth-composition perspective, the Vietnam fintech market is set to evolve as payments mature and other verticals accelerate from a smaller base. Digital payments are likely to sustain mid-teen rates as account ownership nears saturation, while new use cases in merchant acquiring and B2B payments keep activity healthy. Insurtech's acceleration reflects a catch-up dynamic, as carriers pivot toward embedded models and consumer-grade digital experiences. Lending and financing are positioned to benefit from open-banking integration, improved credit data, and better verification, which together reduce default risk and increase addressable demand. These dynamics indicate a broader shift from a payments-led to a multi-product Vietnam fintech industry, which is likely to broaden revenue pools and diversify monetization.

The Vietnam Fintech Market Report is Segmented by Service Proposition (Digital Payments, Digital Lending & Financing, Digital Investments, Insurtech, Neobanking), End-User (Retail, Businesses), User Interface (Mobile Applications, Web/Browser, POS/IoT Devices), and Geography (Northern Vietnam, Central Vietnam, Southern Vietnam). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- M_Service (MoMo)

- VNPay

- ZaloPay (VNG)

- ShopeePay (Sea Ltd.)

- Grab Financial Group (Vietnam)

- BePay (Be Group)

- Timo Digital Bank

- Cake by VPBank

- TPBank

- Techcombank Digital

- Vietcombank Digital

- VPBank

- Payoo

- FinHay

- Infina

- Trusting Social

- Lendbiz

- Mirae Asset Finance Vietnam

- F88

- MFast

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High smartphone & internet penetration

- 4.2.2 Government cash-less roadmap & National Digital Transformation Program

- 4.2.3 Rising middle-class demand for convenient financial services

- 4.2.4 Expansion of NAPAS 247 real-time QR rail

- 4.2.5 Regulatory sandbox for P2P lending & open banking

- 4.2.6 Cross-border e-commerce remittance inflows

- 4.3 Market Restraints

- 4.3.1 Low financial literacy & trust in rural areas

- 4.3.2 Fragmented KYC rules across ministries

- 4.3.3 Unsustainably high CAC from cashback wars

- 4.3.4 Limited cloud availability zones & latency issues

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Proposition

- 5.1.1 Digital Payments

- 5.1.2 Digital Lending & Financing

- 5.1.3 Digital Investments

- 5.1.4 Insurtech

- 5.1.5 Neobanking

- 5.2 By End-User

- 5.2.1 Retail

- 5.2.2 Businesses

- 5.3 By User Interface

- 5.3.1 Mobile Applications

- 5.3.2 Web / Browser

- 5.3.3 POS / IoT Devices

- 5.4 By Geography

- 5.4.1 Northern Vietnam

- 5.4.2 Central Vietnam

- 5.4.3 Southern Vietnam

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 M_Service (MoMo)

- 6.4.2 VNPay

- 6.4.3 ZaloPay (VNG)

- 6.4.4 ShopeePay (Sea Ltd.)

- 6.4.5 Grab Financial Group (Vietnam)

- 6.4.6 BePay (Be Group)

- 6.4.7 Timo Digital Bank

- 6.4.8 Cake by VPBank

- 6.4.9 TPBank

- 6.4.10 Techcombank Digital

- 6.4.11 Vietcombank Digital

- 6.4.12 VPBank

- 6.4.13 Payoo

- 6.4.14 FinHay

- 6.4.15 Infina

- 6.4.16 Trusting Social

- 6.4.17 Lendbiz

- 6.4.18 Mirae Asset Finance Vietnam

- 6.4.19 F88

- 6.4.20 MFast

7 Market Opportunities & Future Outlook

- 7.1 Green financing for rooftop solar boom

- 7.2 Embedded insurance in super-apps