PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035149

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035149

Japan Credit Card - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

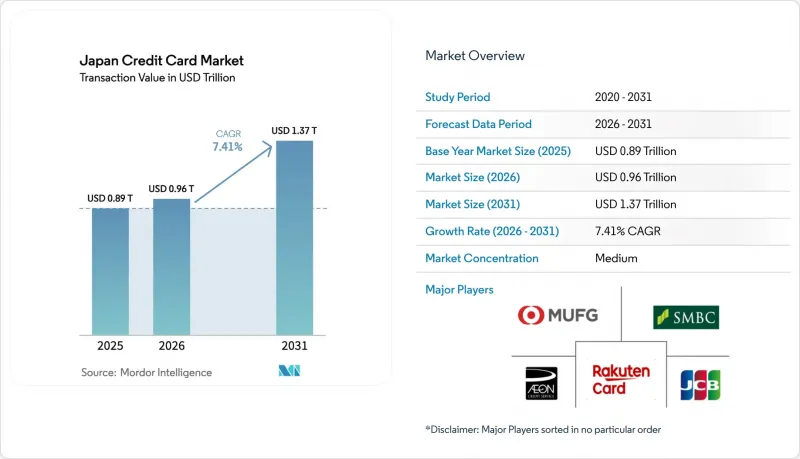

The Japan credit card market size was valued at USD 0.89 trillion in 2025 and estimated to grow from USD 0.96 trillion in 2026 to reach USD 1.37 trillion by 2031, at a CAGR of 7.41% during the forecast period (2026-2031).

In 2024, the increasing reliance on credit cards as a primary mode of cashless transactions highlights the country's ongoing transition toward a cashless economy. Despite this trend, the overall cashless payment ratio remains relatively low, indicating significant potential for growth in the adoption of digital payment methods. State-led digitalization programs, demographic shifts that favour contactless payments, and the integration of cards into super-app ecosystems continue to reinforce adoption momentum. Infrastructure modernization tied to the mandatory 3D Secure rule effective April 2025 is curbing fraud and raising merchant confidence, while inbound tourism recovery and embedded finance innovations are widening usage scenarios for both consumers and small businesses. Competitive dynamics remain intense, yet strategic alliances between banks, card networks, and fintech platforms are opening non-traditional distribution channels that extend the reach of the Japan credit card market.

Japan Credit Card Market Trends and Insights

Rising E-commerce Penetration Drives Transaction Volume Growth

Surging online retail activity funnels incremental spending onto cards, lifting transaction counts and average ticket sizes across the Japan credit card market. PayPay's 7.46 billion transactions in 2024, equivalent to one-fifth of all cashless activity, illustrate how super-apps amplify card-linked volumes both online and at point-of-sale. The Bank of Japan closely tracks JCB Consumption NOW data to gauge private consumption, underscoring the macroeconomic importance of card flows. Specialty products benefit disproportionally, as subscription-based gaming and streaming services underpin Media & Entertainment's double-digit expansion. Transport operators in Kansai have already enabled tap-to-ride credit card payments, blurred category lines, and driven habitual card usage for low-value mobility transactions that once favoured cash.

Government-Backed Cashless Push Accelerates Infrastructure Modernization

The Financial Services Agency and the Digital Agency are coordinating policy, subsidy, and regulatory levers that speed merchant acceptance and strengthen cybersecurity. Required 3D Secure authentication from April 2025 is absorbing fraud losses that climbed to JPY 541 billion (USD 3.60 billion) in 2023, addressing a key bottleneck for digital uptake. My Number digital IDs will be wallet-ready by late spring 2025, enabling biometric verification and further streamlining checkout flows. The Expo 2025 Osaka pilot of facial-recognition payments will showcase next-generation use cases across 1,000 terminals, illustrating how public events can seed nationwide rollouts. Together, these measures establish a secure, standards-based environment that sustains Japan's credit card market growth amid rising transaction complexity.

Ageing Population's Lower Credit Appetite Constrains Expansion

Japan's median age continues to climb, and older consumers generally avoid revolving balances, capping revenue potential for issuers. The senior demographic demonstrates a clear preference for card payments over cash transactions. Their card usage aligns more closely with debit card behaviour, underscoring a focus on transactional convenience rather than leveraging credit facilities. Rural depopulation compounds the issue, shrinking addressable volumes in regions where bank branch closures are already pronounced. Regulatory affordability guidelines further tighten underwriting, demanding more granular income validation for retirees. Issuers therefore pivot toward transaction-based economics, packaging generous points and cross-service bundles that resonate with frugal but digitally savvy seniors.

Other drivers and restraints analyzed in the detailed report include:

- Loyalty-Program Gamification Enhances Customer Lifetime Value

- Integration of Credit Cards into Super-Apps Expands Ecosystem Reach

- Intensifying Debit & QR-Code Competition Pressures Market Share

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

General-purpose cards represented 83.74% of Japan's credit card market size in 2025, reflecting their broad acceptance footprint and omnichannel utility. Specialty & Other cards are gaining ground at a forecast 12.59% CAGR as issuers court high-value niches with metal constructions, lifestyle privileges, and embedded finance options. JAL Luxury Card, launched August 2025, exemplifies ultra-premium positioning with annual fees up to JPY 599,500 (USD 3,990), targeting affluent travellers who demand exclusive lounge access. SME-focused products such as the forthcoming Orico-Aeon business card unlock working-capital lines for underserved corporate segments, illustrating how targeted propositions can widen participation without cannibalizing mainstream portfolios.

Fintech entrants' experiment with creator-economy tie-ups, adding social identity layers that resonate with Gen Z. These novel formats exploit lean digital distribution to bypass costly physical channels, undercut fees, and gin up community engagement metrics. The diversification trend spreads issuer risk and incubates differentiated revenue streams, although scale remains centred on the stalwart General Purpose category that continues to anchor the Japan credit card market.

The Japan Credit Cards Market Report Segments the Industry Into by Card Type (General Purpose Credit Cards, and Other), by Application (Food & Groceries, Health & Pharmacy, Restaurants & Bars, Consumer Electronics, Media & Entertainment, and Other Applications), and by Provider (Visa, Mastercard, Other Providers), and by Geography (Hokkaido, and Other). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mitsubishi UFJ NICOS Co. Ltd.

- Sumitomo Mitsui Card Co. Ltd.

- JCB Co. Ltd.

- Rakuten Card Co. Ltd.

- AEON Credit Service Co. Ltd.

- Orico (Orient Corp.)

- Saison Credit

- PayPay Card Corp.

- Seven Card Service Co. Ltd.

- Toyota Finance Corp.

- NTT Docomo d-Card

- Kyash Inc.

- SMBC Finance Service

- Resona Card Co. Ltd.

- UC Card Co. Ltd.

- Mitsubishi UFJ Trust & Banking Card

- Life Card Co. Ltd.

- Pocket Card Co. Ltd.

- JACCS Co. Ltd.

- APLUS Financial

- Discover Global Network (Japan issuing partners)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising e-commerce penetration

- 4.2.2 Government-backed cashless payments push

- 4.2.3 Loyalty-program gamification by issuers

- 4.2.4 Pandemic-induced digital payment habit stickiness

- 4.2.5 Integration of credit cards into super-apps (under-reported)

- 4.2.6 Growing buy-now-pay-later (BNPL)-card hybrids (under-reported)

- 4.3 Market Restraints

- 4.3.1 Ageing population's lower credit appetite

- 4.3.2 Intensifying debit & QR-code payment competition

- 4.3.3 Stricter FSA affordability controls (under-reported)

- 4.3.4 Cyber-fraud surge in regional ATMs (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Card Type

- 5.1.1 General Purpose Credit Cards

- 5.1.2 Specialty & Other Credit Cards

- 5.2 By Application

- 5.2.1 Food & Groceries

- 5.2.2 Health & Pharmacy

- 5.2.3 Restaurants & Bars

- 5.2.4 Consumer Electronics

- 5.2.5 Media & Entertainment

- 5.2.6 Travel & Tourism

- 5.2.7 Other Applications

- 5.3 By Provider

- 5.3.1 Visa

- 5.3.2 MasterCard

- 5.3.3 Other Providers

- 5.4 By Geography

- 5.4.1 Hokkaido

- 5.4.2 Tohoku

- 5.4.3 Kanto

- 5.4.4 Kyushu & Okinawa

- 5.4.5 Rest of Japan

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mitsubishi UFJ NICOS Co. Ltd.

- 6.4.2 Sumitomo Mitsui Card Co. Ltd.

- 6.4.3 JCB Co. Ltd.

- 6.4.4 Rakuten Card Co. Ltd.

- 6.4.5 AEON Credit Service Co. Ltd.

- 6.4.6 Orico (Orient Corp.)

- 6.4.7 Saison Credit

- 6.4.8 PayPay Card Corp.

- 6.4.9 Seven Card Service Co. Ltd.

- 6.4.10 Toyota Finance Corp.

- 6.4.11 NTT Docomo d-Card

- 6.4.12 Kyash Inc.

- 6.4.13 SMBC Finance Service

- 6.4.14 Resona Card Co. Ltd.

- 6.4.15 UC Card Co. Ltd.

- 6.4.16 Mitsubishi UFJ Trust & Banking Card

- 6.4.17 Life Card Co. Ltd.

- 6.4.18 Pocket Card Co. Ltd.

- 6.4.19 JACCS Co. Ltd.

- 6.4.20 APLUS Financial

- 6.4.21 Discover Global Network (Japan issuing partners)

7 Market Opportunities & Future Outlook

- 7.1 Embedded-finance card issuance for non-financial brands

- 7.2 Tokenized, biometric-authenticated "numberless" cards