PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035151

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035151

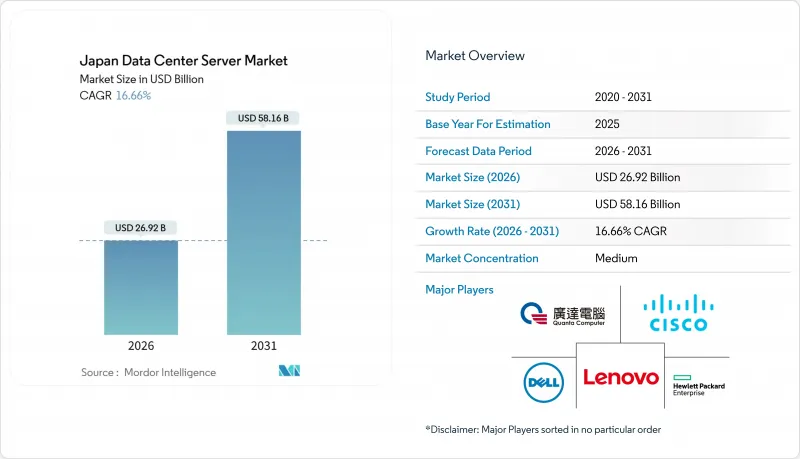

Japan Data Center Server - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan data center server market size stood at USD 26.92 billion in 2026 and is forecast to reach USD 58.16 billion by 2031, expanding at a 16.66% CAGR.

Robust capital outlays by hyperscale cloud providers are accelerating fresh server deployments, while sovereign semiconductor programs shorten component lead times and encourage proprietary silicon adoption. Rapid densification of racks above 100 kilowatts, stricter energy-efficiency mandates, and growing availability of renewable power outside Tokyo and Osaka are reshaping investment priorities. Competitive tension is intensifying as global OEMs introduce liquid-cooled GPU systems to counter domestic incumbents embedding Arm-based processors. Simultaneously, edge-computing use cases in smart-factory automation foster demand for compact micro-blade servers that can fit inside industrial enclosures.

Japan Data Center Server Market Trends and Insights

Expansion Of Hyperscale Facilities By US Cloud Giants

Amazon Web Services, Microsoft Azure, and Oracle pledged more than USD 26 billion of capital between 2024 and 2026, dwarfing the previous decade's cumulative investment and signaling a pivot toward in-country availability zones for regulated workloads. NTT DATA responded with a USD 10 billion build program targeting roughly 1 gigawatt by 2027, while EQUINIX deployed 3,700 cabinets at its TY15 site to satisfy rising interconnection demand. Mitsui Fudosan and Ares Management have likewise financed large campuses in Kanagawa and Tokyo. Faster project cycles favor modular racks that ship pre-integrated, enabling deployment in 90 days rather than 12 months, which benefits vendors with local assembly.

Accelerated Refresh Cycle To AI-Optimized GPU Servers

Japanese operators installed more than 10,000 NVIDIA H200 GPUs during 2025. Notable rollouts include GMO Internet's 1,000-GPU cluster in May, SAKURA Internet's 3,072-unit expansion in August, and AIST's 6,128-GPU ABCI 3.0 supercomputer in January. Generative AI inference pushes rack power well beyond 100 kilowatts, compelling operators to retrofit liquid-cooling. Fujitsu and Super Micro Computer formed an April 2025 pact to embed direct liquid cooling in PRIMERGY servers, aiming for 40% lower energy use. The refresh interval is compressing to 2.5 years as firms reap real-time analytics benefits.

High Land And Power Costs In Metro Regions

Data-center build costs climbed to USD 13.2 million per megawatt in Greater Tokyo during 2024, 35% above Singapore, fueled by scarce land and premium grid tariffs from TEPCO. Developers respond by densifying existing footprints with liquid-cooled racks and by expanding to Hokkaido and Kyushu, where land is 40% cheaper and renewable penetration exceeds 30%.

Other drivers and restraints analyzed in the detailed report include:

- Rising Edge-Computing Nodes For Smart-Factory Rollouts

- Strategic Semiconductor Self-Sufficiency Programs

- Escalating Grid-Power Curtailment Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tier 3 assets dominated the Japan data center server market share at 71.24% in 2025, a reflection of cost-sensitive colocation and enterprise deployments. Tier 4 facilities are projected to expand at a 17.21% CAGR as banks and government agencies demand 99.995% uptime, especially after the 2024 Noto Peninsula earthquake. NEXTDC's TK1 campus launched in 2024 illustrates tenant willingness to pay 25% premium lease rates for higher redundancy.

Vendor strategies now emphasize direct liquid-cooled PRIMERGY and DLC-2 racks that temper the 250-kilowatt densities needed for GPU clusters. The Japan data center server market size for Tier 4 is therefore on track to outpace overall growth. Meanwhile, Tier 1 and Tier 2 rooms continue to decline as enterprises consolidate into regional colocation hubs.

Hyperscale campuses controlled 44.54% of the Japan data center server market in 2025 and will grow at a 17.45% CAGR, buoyed by AWS and NTT DATA programs exceeding 1 gigawatt. Large 10-50 megawatt sites trail as grid delays impede metro builds. Medium facilities face margin pressure amid cloud migration, while small legacy rooms are being decommissioned.

The Japan data center server market size for hyperscale assets is further supported by long-term sale-leaseback deals such as Keppel DC REIT's USD 707 million Tokyo DC 3 purchase, ensuring stable cash flows that attract institutional capital. Edge-oriented operators use modular 10-megawatt designs to match tenant ramp-up and grid schedules.

The Japan Data Center Server Market Report is Segmented by Tier Type (Tier 1 and 2, and More), Data Center Size (Small, Medium, and More), Data Center Type (Colocation, Hyperscalers/CSPs, and More), Form Factor (Half-Height Blades, Full-Height Blades, and More), Application/Workload (Virtualization and Private Cloud, HPC, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Fujitsu Limited

- NEC Corporation

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- Super Micro Computer Inc.

- Quanta Computer Inc.

- Huawei Technologies Co. Ltd.

- IBM Corporation

- Gigabyte Technology

- Cisco Systems Inc.

- Hitachi Ltd.

- ASUSTeK Computer Inc.

- Wistron Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of hyperscale facilities by US cloud giants

- 4.2.2 Rising edge-computing nodes for smart-factory rollouts

- 4.2.3 Accelerated refresh cycle to AI-optimized GPU servers

- 4.2.4 Mandatory "green" procurement rules for government IT

- 4.2.5 Corporate tax incentives for datacenter energy efficiency

- 4.2.6 Strategic semiconductor self-sufficiency programs

- 4.3 Market Restraints

- 4.3.1 High land and power costs in metro regions

- 4.3.2 Escalating grid-power curtailment risks

- 4.3.3 Lengthy environmental approval timelines

- 4.3.4 Talent shortage in advanced server maintenance

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Tier Type

- 5.1.1 Tier 1 and 2

- 5.1.2 Tier 3

- 5.1.3 Tier 4

- 5.2 By Data Center Size

- 5.2.1 Small Data Center

- 5.2.2 Medium Data Center

- 5.2.3 Large Data Center

- 5.2.4 Hyperscale Data Center

- 5.3 By Data Center Type

- 5.3.1 Colocation Data Center

- 5.3.2 Hyperscalers Data Center/CSPs

- 5.3.3 Enterprise and Edge Data Center

- 5.4 By Form Factor

- 5.4.1 Half-height Blades

- 5.4.2 Full-height Blades

- 5.4.3 Quarter-height / Micro-blades

- 5.5 By Application / Workload

- 5.5.1 Virtualisation and Private Cloud

- 5.5.2 High-Performance Computing (HPC)

- 5.5.3 Artificial Intelligence/Machine Learning and Data Analytics

- 5.5.4 Storage-centric

- 5.5.5 Edge / IoT Gateways

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Fujitsu Limited

- 6.4.2 NEC Corporation

- 6.4.3 Dell Technologies Inc.

- 6.4.4 Hewlett Packard Enterprise Company

- 6.4.5 Lenovo Group Limited

- 6.4.6 Super Micro Computer Inc.

- 6.4.7 Quanta Computer Inc.

- 6.4.8 Huawei Technologies Co. Ltd.

- 6.4.9 IBM Corporation

- 6.4.10 Gigabyte Technology

- 6.4.11 Cisco Systems Inc.

- 6.4.12 Hitachi Ltd.

- 6.4.13 ASUSTeK Computer Inc.

- 6.4.14 Wistron Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment