PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043834

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043834

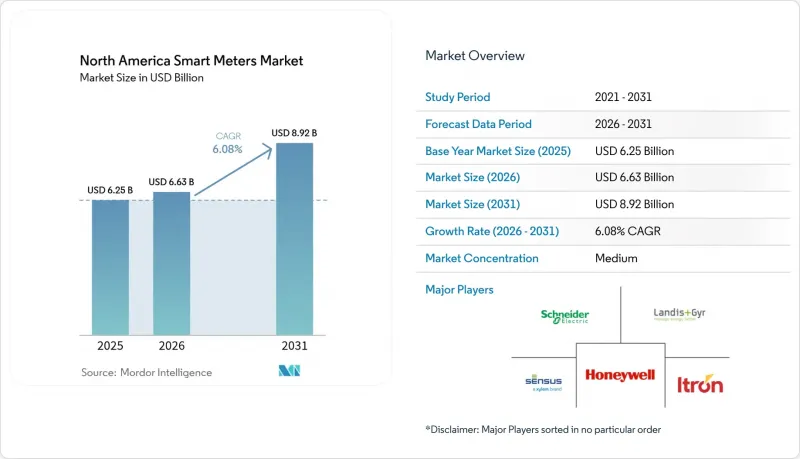

North America Smart Meters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The North America Smart Meters Market size is expected to grow from USD 6.25 billion in 2025 to USD 6.63 billion in 2026 and is forecast to reach USD 8.92 billion by 2031 at 6.08% CAGR over 2026-2031.

Continued modernization of transmission and distribution assets, direct federal appropriations for advanced metering infrastructure, and widening conservation mandates keep the upgrade wave intact across electric, water, and gas utilities. Smart meter penetration has already surpassed 80%, so the next growth leg pivots from first-wave roll-outs to AMI 2.0 replacements that embed edge computing, voltage optimization, and bidirectional measurement of distributed energy resources. Utility demand is further buoyed by real-time billing accuracy, shrinking truck rolls, and the need for granular consumption data that underpins dynamic pricing programs and customer engagement portals. Semiconductor supply-chain pressures have moderated since late 2024, yet component risk remains a gating factor that utilities manage through multi-year procurement contracts, strengthened vendor diversification, and higher safety inventories, sustaining purchasing momentum in the North America Smart Meters market.

North America Smart Meters Market Trends and Insights

Regulatory Mandates for Nationwide Smart-Electric Meter Roll-outs

Obligatory installation rules have transformed advanced metering from a discretionary technology into grid infrastructure. Ontario's early directive, which has driven 90% time-of-use rate adoption, showed regulators across North America how tariff reform and smart-meter penetration can move in lockstep. California's Assembly Bill 2572 applies parallel pressure in the water sector by requiring smart water meters at every home by 2025. New York's Senate Bill S1550 adds a health-impact reporting layer, signaling expanded oversight while still keeping deployment engines running. Predictable compliance timelines give suppliers confidence to scale production capacity, locking in multi-year contracts that sustain volume for the North America Smart Meters market.

Utility-led Grid-Modernization Programs

Utilities are bundling AMI with distribution automation, voltage control, and outage management investments. The U.S. Department of Energy's Smart Grid Investment Grant funded 99 projects valued at USD 8 billion, embedding advanced meters as the sensor backbone of modern grids. Public Service Company of New Mexico alone earmarked USD 188 million for meter upgrades inside a broader USD 344 million modernization road map. Most firms now specify AMI 2.0 endpoints with extra processing power and memory, enabling on-board analytics that detect voltage anomalies and DER back-feed in real time, thus improving grid visibility while creating incremental revenue opportunities for analytics software providers.

High Upfront Meter & Installation Costs

Smart meters cost five to seven times more than legacy analog devices once field labor, communications modules, and back-office integration are included. San Jose Water's USD 100 million outlay for 230,000 units equates to roughly USD 435 per endpoint. BC Hydro's province-wide program required CAD 2 billion (USD 1.5 billion) but promises CAD 520 million (USD 390 million) in net present value by 2033. Rate cases often allow recovery through tariff adders, yet smaller cooperatives with limited borrowing power sometimes stretch deployments over eight to ten years, dampening near-term installation volumes and injecting episodic demand variance into the North America Smart Meters market.

Other drivers and restraints analyzed in the detailed report include:

- Federal and State Funding for Infrastructure Upgrades

- Demand for Real-time Consumption Data & Accurate Billing

- Cyber-security and Data-privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electricity meters generated 79.60% of 2025 revenue, underscoring their anchor role in the North America Smart Meters market. Mandatory replacement schedules and 111 million deployed endpoints across the United States ensure a steady AMI 2.0 refresh cycle. Utilities value voltage analytics, outage detection, and service disconnection features that help recoup theft losses and reduce O&M spending.

Water meters, though only 13.10% of 2025 revenue, are outpacing every other device category at a 7.20% CAGR. Conservation mandates, leak-reduction targets, and state-funded drought resilience programs drive growth, with utilities like San Francisco rolling out 180,000 units under a USD 56 million budget. American Water has already surpassed 1 million installations, reporting 38% leak-duration reductions and a double-digit cut in non-revenue water.

Gas meters comprise the remaining share. Their modest unit growth is buoyed by safety regulations that mandate remote shut-off and methane-leak detection. Several utilities bundle electric, gas, and water installations to maximize truck-roll efficiency, a practice that further increases total addressable volume for the North America Smart Meters market.

The North America Smart Meters Market Report is Segmented by Type (Electricity Meters, Water Meters, and Gas Meters), Communication Technology (RF Mesh, Power-Line Communication, Cellular, and Other Short-Range), End-User (Residential, Commercial, and Industrial), and Geography (United States, Canada, and Mexico). The Market Size and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Landis+Gyr

- Itron

- Xylem (Sensus)

- Schneider Electric

- Honeywell International

- Siemens AG

- ABB Ltd

- Aclara (Hubbell)

- Kamstrup

- Badger Meter

- Neptune Technology Group

- EDMI

- Holley Technology

- Elster Group

- Silver Spring Networks (Itron)

- Trilliant

- Sagemcom

- Iskraemeco

- Hexing Electric

- EKM Metering

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory mandates for nationwide smart-electric meter roll-outs

- 4.2.2 Utility-led grid-modernization programs

- 4.2.3 Federal and state funding for infrastructure upgrades

- 4.2.4 Demand for real-time consumption data & accurate billing

- 4.2.5 Bi-directional metering to integrate distributed energy resources

- 4.2.6 Water-utility time-of-use tariffs amid drought management

- 4.3 Market Restraints

- 4.3.1 High upfront meter & installation costs

- 4.3.2 Cyber-security and data-privacy concerns

- 4.3.3 Semiconductor supply-chain volatility

- 4.3.4 Local pushback over RF-emission health fears

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Electricity Meters

- 5.1.2 Water Meters

- 5.1.3 Gas Meters

- 5.2 By Communication Technology

- 5.2.1 RF Mesh

- 5.2.2 Power-Line Communication (PLC)

- 5.2.3 Cellular

- 5.2.4 Other Short-Range (Wi-Fi, Zigbee, BLE)

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Landis+Gyr

- 6.4.2 Itron

- 6.4.3 Xylem (Sensus)

- 6.4.4 Schneider Electric

- 6.4.5 Honeywell International

- 6.4.6 Siemens AG

- 6.4.7 ABB Ltd

- 6.4.8 Aclara (Hubbell)

- 6.4.9 Kamstrup

- 6.4.10 Badger Meter

- 6.4.11 Neptune Technology Group

- 6.4.12 EDMI

- 6.4.13 Holley Technology

- 6.4.14 Elster Group

- 6.4.15 Silver Spring Networks (Itron)

- 6.4.16 Trilliant

- 6.4.17 Sagemcom

- 6.4.18 Iskraemeco

- 6.4.19 Hexing Electric

- 6.4.20 EKM Metering

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment