PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043840

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043840

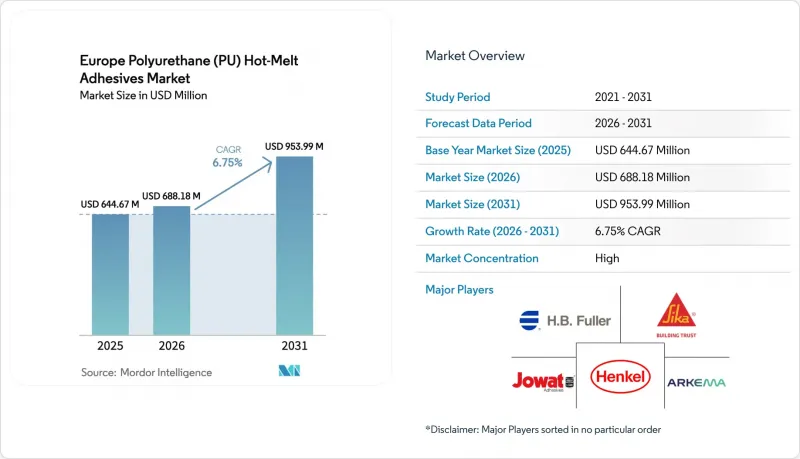

Europe Polyurethane (PU) Hot-Melt Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe Polyurethane Hot-Melt Adhesives Market size is projected to expand from USD 644.67 million in 2025 and USD 688.18 million in 2026 to USD 953.99 million by 2031, registering a CAGR of 6.75% between 2026 to 2031. Accelerated migration away from solvent-based chemistries, rising automation in edge-banding and vehicle assembly, and the quest for lighter, repair-friendly packaging are steering volume toward high-performance reactive formulations. Western European parcel networks handled 2.1 billion intra-EU shipments in 2025, broadening the customer base for fast-setting grades that tolerate recycled board and high-speed case sealers. Automotive OEMs are substituting mechanical fasteners with polyurethane bonding to cut body-in-white weight by up to 2 kg per roof panel, directly improving electric-vehicle range. At the same time, furniture lines in Germany, Poland, and Italy have adopted zero-joint edge-banding equipment that demands adhesives curing in less than 10 seconds at 25 m min line speeds. Supply risk for isocyanate feedstocks has elevated input-cost volatility, but leading formulators are hedging by backward-integrating polyol capacity and experimenting with bio-based intermediates to soften exposure.

Europe Polyurethane (PU) Hot-Melt Adhesives Market Trends and Insights

Surge in E-Commerce Packaging Volumes

Cross-border parcel traffic within the European Union rose 12% year-on-year to 2.1 billion units in 2025. Higher throughput has pushed fulfillment centers to replace slower water-based adhesives with reactive grades that set within five seconds on recycled corrugated substrates. Henkel's Technomelt Supra 100 series, launched in early 2025, withstands the impact loads of automated sorters while bonding to lower-grammage liners. Upcoming European Union (EU) Packaging and Packaging Waste Regulation targets 65% recycled content by 2030, further tilting specifications toward chemistries that perform on rougher fiber surfaces. Bostik recorded a 15% jump in European packaging-adhesive revenue in 2025, noting that polyurethane hot melts supplied more than half of the incremental growth.

European Union VOC Rules Accelerating Solvent-Free Adhesive Adoption

The Industrial Emissions Directive caps plant-level VOC emissions at 50 g kg adhesive applied, eliminating most solvent-based contact adhesives from new European installations. Germany's TA Luft revision in 2024 tightened the limit to 20 g/kg for furniture and automotive lines, cementing the transition to 100%-solids polyurethane hot melts. Covestro's Desmomelt portfolio, which emits zero VOCs (Volatile Organic Compounds) and cures via ambient moisture, registered a 22% sales rise in 2025 as OEMs (Original Equipment Manufacturers) prioritized compliance-ready alternatives. France's ICPE (Installations classified for environmental protection) framework now requires annual VOC audits for plants using more than one ton of adhesive, raising fixed administrative costs and favoring solvent-free systems. Consolidation is accelerating: Sika purchased two regional producers in Poland and Spain during 2025, citing the regulatory hurdle as a catalyst.

Isocyanate Feedstock Price Volatility

European MDI spot prices averaged EUR 2,450 t in 2025, an 18% leap over January 2024, driven by Chinese production cuts and Europe's elevated gas costs. BASF, Covestro, and Huntsman trimmed regional output by 12%, prioritizing higher-margin rigid foam customers and tightening adhesive supply. TDI prices fluctuated between EUR 2,100 and EUR 2,900 t during 2025, reflecting outages at BASF Ludwigshafen and Covestro Dormagen. Margin compression exceeded 300 basis points for spot-buying converters, pushing several Italian and Spanish shops to halt new-product development. Brussels opened an antitrust investigation into isocyanate producers in late 2025, injecting added uncertainty into expansion plans.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Lightweight Structures Needing Fast-Cycle Bonding

- Edge-Banding Automation in Modular Furniture Lines

- Mandatory Di-Isocyanate Worker-Training Regulation (EU 2023/C)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reactive grades accounted for 86.20% of the Europe Polyurethane (PU) Hot-Melt Adhesives market size in 2025 and are projected to grow at 6.92% during the forecast period (2026-2031), propelled by urethane-urea crosslinking that yields heat- and moisture-resistant joints above 10 MPa. Automobile body-in-white bonding, battery-pack encapsulation, and medical wearables rely on this chemistry to resist sterilization at 134°C or endure 1,000 charge-discharge vibration cycles. Converters also prize the adhesives for their ability to bond to low-surface-energy substrates such as polyolefin elastomers after plasma activation. Germany's stringent VOC limits provide a regulatory tailwind because reactive formulations are 100% solids and solvent-free.

Non-reactive polyurethane hot melts' utility persists in bookbinding, textile lamination, and temporary footwear lasting since they cool-set rapidly and can be heat-reactivated. Book manufacturers value the open time flexibility for multi-signature alignment, while flexible-packaging converters laud the sub-120°C application that cuts natural-gas usage. Footwear factories in Portugal have shifted to non-reactive grades for toe-lasting, where the bond must release cleanly post-thermoforming. Despite these strengths, the segment faces structural headwinds: EU circular-economy guidelines reward durable assemblies and recyclability, diminishing the appeal of easy-rework adhesives. Consequently, the Europe polyurethane (PU) hot-melt adhesives market will continue tilting toward reactive chemistries, but non-reactive systems will defend niches tied to short dwell times and low-heat substrates.

The Europe Polyurethane (PU) Hot-Melt Adhesives Market is Segmented by Type (Non-Reactive and Reactive), Application (Packaging, Healthcare, Automotive, Furniture, Footwear, Textile, Electronics, Bookbinding, and Others), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, and the Rest of Europe). The Market Sizing and Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- AdCo (UK) Ltd.

- Arkema

- Artimelt AG

- BASF SE

- Buhnen Gmbh & Co. KG

- Delo Industrial Adhesives

- DIC CORPORATION

- Dow

- Franklin International

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- Jowat SE

- Klebchemie M. G. Becker GmbH & Co. KG

- Mapei SpA

- Master Bond Inc.

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in e-commerce packaging volumes

- 4.2.2 Electronics assembly shift toward low-VOC bonding

- 4.2.3 European Union VOC rules accelerating solvent-free adhesive adoption

- 4.2.4 Automotive lightweight structures needing fast-cycle bonding

- 4.2.5 Edge-banding automation in modular furniture lines

- 4.3 Market Restraints

- 4.3.1 Isocyanate feedstock price volatility

- 4.3.2 Mandatory di-isocyanate worker-training regulation (EU 2023/ C)

- 4.3.3 High European energy prices raising melt-line OPEX

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Non-reactive

- 5.1.2 Reactive

- 5.2 By Application

- 5.2.1 Packaging

- 5.2.2 Healthcare

- 5.2.3 Automotive

- 5.2.4 Furniture

- 5.2.5 Footwear

- 5.2.6 Textile

- 5.2.7 Electronics

- 5.2.8 Bookbinding

- 5.2.9 Others

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Russia

- 5.3.7 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 AdCo (UK) Ltd.

- 6.4.3 Arkema

- 6.4.4 Artimelt AG

- 6.4.5 BASF SE

- 6.4.6 Buhnen Gmbh & Co. KG

- 6.4.7 Delo Industrial Adhesives

- 6.4.8 DIC CORPORATION

- 6.4.9 Dow

- 6.4.10 Franklin International

- 6.4.11 H.B. Fuller Company

- 6.4.12 Henkel AG & Co. KGaA

- 6.4.13 Huntsman International LLC

- 6.4.14 Jowat SE

- 6.4.15 Klebchemie M. G. Becker GmbH & Co. KG

- 6.4.16 Mapei SpA

- 6.4.17 Master Bond Inc.

- 6.4.18 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment